Jiuchang Wei is currently a Professor at the University of Science and Technology of China (USTC). He received his Ph.D. degree from USTC in 2006. His research mainly focuses on risk and crisis management and organizational reputation management

Ruixue Jiang is currently a Special Associate Researcher at the University of Science and Technology of China (USTC). She received her Ph.D. degree from USTC in 2019. Her research mainly focuses on efficiency evaluation, decision-making, and strategic management

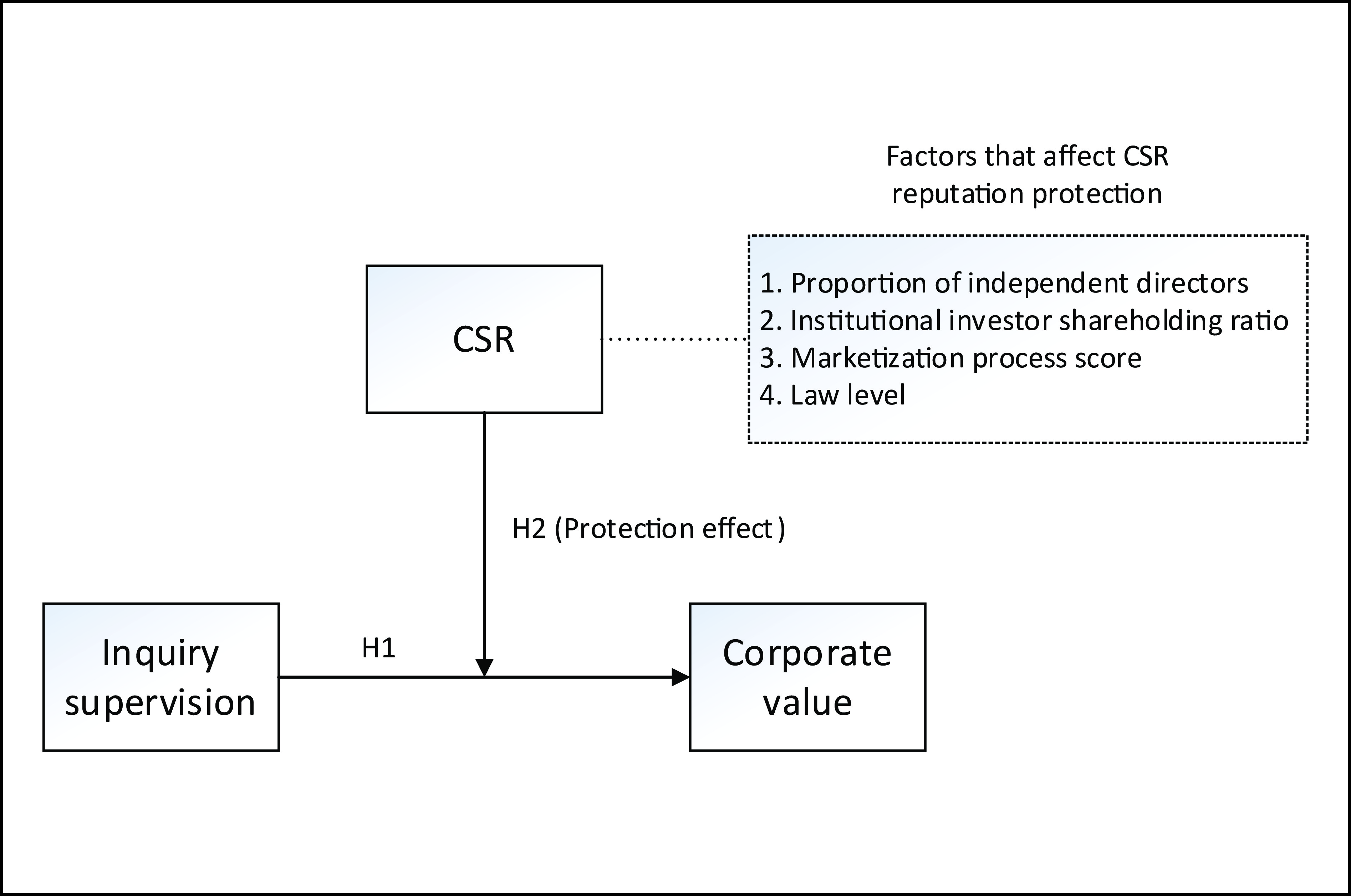

This study analyses all A-share listed companies from 2015 to 2020 to empirically examine the impact of inquiry supervision on corporate value and the moderating influence of corporate social responsibility (CSR) on this relationship. Research has shown that inquiry supervision significantly reduces corporate value, and the corporate social responsibility previously performed by companies can weaken this negative impact. Furthermore, the heterogeneity test based on internal and external controls shows that the reputation protection effect of CSR is more significant for companies with a higher proportion of independent directors, companies with a higher proportion of institutional investors investing in stocks, regions with a higher degree of marketization, and regions with a higher level of rule of law. The research in this article validates the effectiveness of reputation protection and verifies that reputation protection, as an informal mechanism, is easier to fulfil a role in areas where formal mechanisms are perfect. In other words, formal and informal mechanisms appear to complement each other. These findings provide empirical insights into the governance of CSR.

Graphical Abstract

CSR can alleviate the adverse impact of inquiry supervision on corporate value.

Abstract

This study analyses all A-share listed companies from 2015 to 2020 to empirically examine the impact of inquiry supervision on corporate value and the moderating influence of corporate social responsibility (CSR) on this relationship. Research has shown that inquiry supervision significantly reduces corporate value, and the corporate social responsibility previously performed by companies can weaken this negative impact. Furthermore, the heterogeneity test based on internal and external controls shows that the reputation protection effect of CSR is more significant for companies with a higher proportion of independent directors, companies with a higher proportion of institutional investors investing in stocks, regions with a higher degree of marketization, and regions with a higher level of rule of law. The research in this article validates the effectiveness of reputation protection and verifies that reputation protection, as an informal mechanism, is easier to fulfil a role in areas where formal mechanisms are perfect. In other words, formal and informal mechanisms appear to complement each other. These findings provide empirical insights into the governance of CSR.

Public Summary

Inquiry supervision has a negative impact on corporate value.

When companies actively fulfill their social responsibilities, they can effectively alleviate the adverse impact of inquiry supervision on corporate value.

The role of corporate social responsibility (CSR) in reputation protection was examined in companies with a high proportion of independent directors, companies with a high shareholding ratio of institutional investors, a high degree of marketization, and regions with a high level of rule of law. It was verified that reputation protection, as an informal mechanism, is easier to play in areas where the formal mechanism is perfect. That is, formal and informal mechanisms complement each other.

In recent years, China has vigorously promoted the reform of the capital market regulatory system. The government has continuously enhanced the modernization level of market supervision, promoting the diversification of regulatory models in the securities market. In addition to the punitive supervision issued by the China Securities Regulatory Commission (CSRC), nonpunitive supervision represented by inquiry supervision issued by securities exchanges is also an important part of China’s regulatory measures. Since the full implementation of information disclosure expression in 2013, the regulatory measure of inquiry supervision has been widely used[1]. Once securities exchanges discover abnormal issues in corporate governance, information disclosure, and other aspects, they often no longer audit and disclose them first[2] but rather directly send letters to inquire, which has attracted the attention of banks, investors, and suppliers[3].

However, the issues captured in the inquiry letters are not yet within the scope of illegal and irregular activities and have not reached the level of administrative penalties. For example, there are several issues related to corporate social responsibility (CSR), such as taxation, environmental responsibility, employee compensation, and charitable donations[4]. The inquiry letter issued by the securities exchanges, as one of the important regulatory measures in the capital market, urges listed companies to fulfill their information disclosure obligations in a timely and accurate manner, ensuring market fairness, impartiality, and transparency. If a listed company fails to provide answers to the inquiry letter and make relevant disclosures within the prescribed period, it is likely to face penalties and market risks from the securities exchange, which will objectively have a negative impact on the company’s reputation. This will inevitably affect the attitudes and behaviors of stakeholders and the public toward the company and have an impact on the company’s business performance.

In addition to CSRC, the US Securities and Exchange Commission (SEC) and the Australian Stock Exchange (ASX) also adopt an inquiry regulatory system, but there are certain differences in regulatory requirements among the three countries. First, in terms of response time for companies, the ASX requires companies to provide a response within one trading day. The SEC allows companies to respond within ten days after receiving the letter, while CSRC requires companies to respond within ten days after sending the letter. Second, in terms of timeliness of information disclosure, the ASX discloses only inquiry letters and response letters after receiving a response letter. The SEC generally discloses information 20 days after the inquiry is completed, while the Chinese Stock Exchange will issue inquiry letters in real time and disclose information in real time after receiving a response letter from the company. Third, as far as the issuing agency is concerned, the ASX is a listed company, and the SEC is similar to CSRC, which has a higher regulatory level. The main issuing agency for inquiry letters in China is the Shanghai and Shenzhen Stock Exchanges, which are affiliated with the CSRC.

Compared to punitive supervision, inquiry supervision is gentler and effectively promotes the self-improvement of companies. However, this does not mean that it has not damaged the value of the company. According to previous literature, it may have a certain negative impact on the reputation, investment efficiency, management performance, and stock price collapse risk of an enterprise. However, there has been insufficient attention in the previous literature on how companies can adjust their strategic decisions to cope with the deep economic consequences of inquiry supervision. In addition, according to Ref. [5], the social responsibility behaviors of companies can play a certain buffering role in the economic losses caused by crises.

This provides some inspiration for this article. Can corporate social responsibility (CSR) be seen as a protective strategy to alleviate the negative impact of inquiry supervision? Can this strategy enhance the reputation and investor confidence of companies, thereby protecting their value? Based on the above questions, this article proposes the following questions: Will inquiry supervision have a negative impact on corporate value? To maintain corporate value, will companies reduce their losses from nonpunitive supervision by taking on more social responsibilities? Will the reputation protection effect of CSR activities be influenced by internal control and the external environment, and what are the possible impact mechanisms?

Therefore, this article takes Chinese listed companies under inquiry supervision as the background and uses all A-share listed companies from 2015 to 2020 as research samples. Multiple regression analysis was used to empirically test the impact of inquiry supervision on corporate value and the reputation protection mechanism of CSR behavior. The research results indicate that inquiry supervision significantly reduces corporate value and that CSR activities performed by companies before the issuance of inquiry supervision can provide certain protection for corporate value after they are subjected to inquiry supervision.

Compared to the literature, the contribution of this article lies in these two points. First, this article introduces the important perspective of CSR, but unlike previous studies, it does not consider CSR as the dependent variable but rather as a moderating variable. This article delves into its moderating effect on the relationship between inquiry supervision and corporate value. Through empirical analysis, we found that when companies actively fulfill their social responsibilities, they can effectively alleviate the adverse impact of inquiry supervision on corporate value. This discovery not only enriches the research on the relationship between inquiry supervision and corporate value but also provides theoretical support for companies to respond to nonpunitive supervision by actively fulfilling social responsibility. Second, this article overcomes the limitations of previous studies that focused only on inquiry supervision and further considers the heterogeneity of CSR. We conducted an in-depth analysis of the protective effects of reputation in different social contexts. The role of CSR behavior in reputation protection was examined in companies with a high proportion of independent directors, companies with a high shareholding ratio of institutional investors, a high degree of marketization, and regions with a high level of rule of law. It was verified that reputation protection, as an informal mechanism, is easier to play in areas where the formal mechanism is perfect. That is, formal and informal mechanisms complement each other.

2.

Literature review

2.1

Inquiry supervision

2.1.1

Influence factor

The definition of inquiry supervision is that securities exchanges issue inquiry letters to listed companies that engage in violations during their business operations. As a warning, it aims to require listed companies to provide answers to the relevant questions in the inquiry letters and fulfill their information disclosure obligations. At present, research on securities supervision in China has focused mainly on punitive supervision, with only a few studies focusing on nonpunitive supervision. The most common regulatory method is to issue inquiry letters to regulatory objects. The main body of inquiry regulatory letters is the securities exchange, and the disclosure issues targeted by listed companies are relatively minor, mostly due to inaccurate or incomplete information disclosure. Therefore, they do not directly punish or regulate listed companies but rather urge them to supplement information and provide explanations. Lin et al.[4] believed that unlike punitive supervision directly targeting listed companies, the disclosure issues of listed companies targeted by regulatory inquiries are not yet serious and do not fall within the scope of illegal and irregular activities. Its regulatory strength is not as strong as that of punitive supervision, but its regulatory scope is wider, and the frequency of supervision is greater. Li et al.[6] found that inquiry supervision can exert regulatory effects, and the size of regulatory effects is influenced by the characteristics of inquiry letters (inquiry frequency, inquiry content, and inquiry tone) and the characteristics of the inquired companies (legal risk and external supervision mechanism).

Cassell et al.[7] found that the greater the fluctuation of stock prices, the greater the likelihood of a company being regulated. In addition, companies with lower level of corporate governance are more likely to be regulated. Heese et al.[8] found that the greater a company’s political affiliation is, the more likely it is to receive inquiry letters. Based on the annual report inquiry letter issued by the SEC, Johnston and Petacchi[9] explored the influencing factors of inquiry letters and concluded that larger companies with greater performance fluctuations are more likely to receive opinion letters .

2.1.2

Economic consequences

The academic community is concerned about the economic consequences of inquiry supervision. Zhao et al.[10] believed that inquiry letters play a role in stock price fluctuations, corporate information disclosure, and the quality of company earnings. Zhu et al.[2] believed that from the perspective of market pressure, inquiry supervision can lead to negative cognitive anchoring among stakeholders and damage corporate reputation. Chen et al.[11] believed that the announcement of the receipt of a financial report inquiry letter indicates that the company’s financial information disclosure is insufficient or does not comply with relevant rules and regulations, which will cause negative reputation damage to relevant companies, reduce investors’ trust in the company’s financial reports, and may even trigger negative reactions in the securities market. Shi et al.[12] believed that listed companies may face negative impacts such as reputation loss, public opinion pressure, stock price fluctuations, and increased company risk after receiving inquiry letters.

Johnston and Petacchi[9] noted that after receiving inquiry letters, listed companies will experience a significant decline in their excess return on stock prices and a decrease in stock trading volume. A study by Gietzmann and Pettinicchio[13] suggested that auditors will reassess the reputation and potential litigation risks of clients upon receiving an opinion letter and, accordingly, increase audit fees. Gietzmann and Isidro[14] delved into the specific impact of SEC inquiry letters on institutional investors, observing that once a company receives a letter, institutional investors will significantly reduce their holdings. A study by Brown et al. [15] revealed that when the SEC requests information disclosure, even listed companies that have not been directly regulated will significantly increase their information disclosure in the following year. Similarly, Bill et al.[16] also found that when listed companies receive inquiry letters related to goodwill, even for companies that have not received such inquiries, auditors will strengthen their review of their goodwill more strictly.

2.2

CSR and its protection effect

With the development of the information economy, the media is filled with reports on CSR-related issues. The government’s and the public’s call for companies to fulfill their social responsibilities is becoming stronger. At the same time, management and business communities have realized that actively fulfilling social responsibility is an important means to improve the visibility and reputation of companies, and irresponsible behavior may cause devastating blows to companies.

The research on CSR originated in the 1960s. Wood[17] believed that CSR mainly refers to a company actively engaging in socially responsible behavior, transcending economic and legal requirements. In the literature, the economic effects of CSR can be roughly divided into two categories: value-added effects and reputation protection effects. The value-added effect proposed in Ref. [18] suggests that CSR can directly or indirectly enhance corporate wealth. Meng and Hou[19] believed that from the perspective of the reputation protection mechanism, CSR describes the contribution that a company makes to stakeholders in addition to pursuing profit maximization, which can help the company accumulate reputation capital and moral capital. Godfrey[20] proposed the protection effect, which suggests that the CSR fulfilled by a company before a crisis event can provide a similar protection effect to the wealth of its shareholders after the crisis event. Although CSR does not always bring direct economic benefits to businesses, it helps to mitigate the impact of negative information and minimize the losses caused by negative events.

The focus of this article is on the protection effect of CSR. Chad and Lewis [21] argued that the degree to which CSR has protective value depends on whether the crisis event is in the same field as the company’s social reputation. If they are in the same field, CSR not only fails to provide effective protection but also has negative impacts. Gao et al. [22] believed that reputation capital can reduce the impact of unexpected negative events on a company. Fan’s study[23] defined the value-added effect of CSR on a company after a crisis event as the protective effect of CSR on the company’s market value. After a crisis event occurs, companies can actively fulfill and disclose short-term corporate social responsibility behaviors, respond to the expectations of stakeholders in a timely manner, not only disperse and guide public opinion and restore corporate reputation but also transmit signals of positive actions, repair the damaged brand image in the crisis, and ultimately recover the damaged wealth of the company. Klein et al.[24] proposed that CSR can serve as a protective strategy for responding to negative events, thereby bringing value to companies. Hoi et al.[25] found that corporate social responsibility activities have a reputation protection effect, reducing the risk of politics, regulatory, and social sanctions that companies face when facing negative events. Gong et al. [26] believed that reputation protection, as an informal institutional arrangement, is an important component of the orderly operation of the market. A good reputation can bring a competitive advantage to a company, while a bad reputation may lead to consumers losing trust, thereby damaging the value of the company.

The important role of reputation as a governance mechanism has been recognized by the academic community. Fu and Ji[27] found that the perspective of risk management is often overlooked in most empirical studies. From this perspective, they found that even though CSR cannot bring direct economic benefits to the company, it can play a role in reputation protection. Gu et al.[28] believed that CSR is a strategic resource that can be used to restore a company’s reputation and mitigate the adverse effects of negative events. At the same time, regulatory penalties can encourage companies to fulfill their social responsibilities. Che and Su[29] believed that the reputation recovery effect of CSR will be more effective in the context of inquiry events. There are certain boundary conditions for the value effect of CSR. When high responsibility attribution crisis events such as violation penalties occur, it is difficult for CSR to play a protective role. Compared with punitive supervision, the problems involved are not yet serious.

After reviewing the above literature, it can be found that inquiry supervision issued by securities exchanges is an effective means of market supervision, and CSR is a strategic resource. When security issues, potential boycotts, or other improper behaviors may cause reputational damage to companies, companies that are trusted by stakeholders and implement social responsibility strategies can reduce the associated risks. However, few studies have investigated the reputation protection effect of CSR behavior after inquiry supervision on corporate value, so we conduct research on this issue.

3.

Theoretical analysis and research hypotheses

3.1

The impact of inquiry supervision on corporate value

The inquiry letter received by listed companies has conveyed negative signals to the market that there may be unreliable financial reports in the future, increasing uncertainty in their future financial situation and operating environment, affecting the company’s reputation, reducing trust between the company and investors, and strengthening information asymmetry between the company and its stakeholders. Ultimately, this leads to a loss of corporate value. Specifically, a company’s receipt of regulatory inquiry letters may affect its corporate value in the following two ways.

First, based on the theory of information asymmetry. In market economy activities, there are differences in the level of understanding of relevant information among various types of personnel. Those who have sufficient knowledge of information are often in a more advantageous position, while those who have insufficient knowledge are in a more disadvantageous position. Asymmetric information may lead to adverse selection, resulting in investment risks. When a company receives an inquiry letter, due to information asymmetry, stakeholders often can only evaluate the company and crisis based on the information disclosed by the company and then determine their own behavior. When a listed company receives an inquiry letter, the quality of the company’s financial information is often poor, and the disclosure is insufficient. When investors receive relevant information, to reduce the risk cost caused by information asymmetry, they are more likely to avoid risk by selling the company’s stocks. This will increase the agency cost of the company, which will have a negative impact on its debt financing and business performance.

Second, it is based on the theory of reputation mechanisms. A company has many stakeholders, and their attitudes toward the company are largely influenced by the company’s reputation. If a company believes that its reputation is valuable, it will constrain its behavior to protect its reputation and make its reputation conform to social norms. After the information announcement that listed companies receive inquiry letters is disclosed, the negative event transmits bad news to the market, thereby causing a certain negative impact on the company’s reputation. A negative reputation can transmit negative signals to stakeholders and public media, reducing social confidence in the company. At the same time, the decrease in trust among stakeholders in the company can in turn damage the company’s reputation and have a negative impact on its economic benefits.

Fu and Zeng[30] believed that the annual report inquiry letter is a relatively strong regulatory signal that can cause stakeholders to form new cognitive anchors, which are usually negative, thereby interfering with stakeholders’ value expectations and rational judgments toward the company. Deng et al.[31] believed that inquiry supervision sends negative signals to the market, such as poor information disclosure quality and poor business management of companies that receive inquiry letters. This not only has a negative impact on the company’s reputation and reduces market trust in the company but also damages the reputation of executives. Zhan et al.[32] found that being punished for violations can have a negative impact on a company’s reputation, thereby transmitting negative news to the capital and product markets.

Ren and Han[33] found that crisis events not only disrupt the normal operation of companies and reduce their performance but also cause negative media coverage of companies, thereby undermining the trust of stakeholders in the company. Pi[34] found that after the issuance of inquiry letters, the stock price volatility risk of receiving companies significantly increases during short-term event window periods, and the short-term market response of receiving companies is significantly negative. In the long run, the exacerbating effect of inquiry letters on stock price volatility risk disappears. However, the full sample results show that the long-term market response to inquiry letters is still significantly negative, indicating that the long-term market performance of receiving companies is poor and that inquiry letters have a long-term risk warning effect.

Based on the above analysis, the first hypothesis of this article is proposed:

H1. Receiving an annual report inquiry letter will have a negative impact on a company’s value.

3.2

Moderating effect of CSR

According to Godfrey’s reputation protection theory[35], certain types of CSR activities can generate moral capital or goodwill, thereby mitigating punitive sanctions against stakeholders in negative events. At the same time, the moral capital generated may not be related to generating economic value but may play an important role in maintaining economic value. Corporate social responsibility activities demonstrate the existence of moral capital to investors and may mitigate potential sanctions. That is, after the information that a listed company receives inquiry letter is disclosed, the good reputation accumulated by the listed company can protect the stock price from significant fluctuations. However, companies without corporate social responsibility activities lack reputation protection and are likely to face greater risks.

Bae et al.[5] believed that actively assuming social responsibility before a company’s violations can effectively buffer the social public opinion and reputation crisis caused by the company’s violations in the short term and alleviate the impact of company violations on the company’s stock price and operating performance. Hemingway and Maclagan[36] argued that CSR can whitewash the improper practices of management in corporate governance. During the period between the occurrence of events and information disclosure, companies can whitewash their external attention to negative events by fulfilling their social responsibilities. After negative events are publicly disclosed, these corporate social responsibility activities reduce the attribution of stakeholders to negative events, thereby mitigating reputation losses and shareholder wealth losses. Zhang and Li[37] found that a higher level of social reputation trust leads to lower financial costs.

Based on the above analysis, the second hypothesis of this article is proposed:

H2. The fulfillment of CSR can provide reputation protection for companies that receive inquiry supervision and alleviate the impact of inquiry supervision on corporate value.

4.

Data and methodology

4.1

Data sources

Considering that the current publicly available annual report inquiry letter text began in 2015, this article uses data from all A-share listed companies from 2015 to 2020 as the initial sample. The data of listed companies come from the CSMAR, and the data related to CSR come from the Hexun website. All samples were processed as follows: ① Exclude listed companies with ST and *ST. Abnormal financial conditions may affect the research results. ② Exclude companies that have been listed for less than one year to exclude the impact of IPOs. Companies that have been listed for less than a year have experienced significant stock price fluctuations, which is not conducive to effective stock selection. ③ Exclude listed companies with negative net assets. The occurrence of operational losses or financial risks in such companies may affect the research results. ④ Exclude samples with missing data. After the above processing, 14175 samples were ultimately obtained.

4.2

Variables

4.2.1

The dependent variable

TobinQ, calculated as market value/total assets, market value= (total share capital – domestic listed foreign shares B shares) × current closing price of A shares + domestic listed foreign shares B shares × current closing price of B shares × current exchange rate of the day. This article uses this as a measure of corporate value. TobinQ has two different metering methods, namely TobinQA and TobinQC.

4.2.2

Explanatory variable

CL: If the company received a regulatory inquiry letter from the securities exchange in the current year, it is set to 1; otherwise, it is set to 0.

4.2.3

Moderating variable

CSR: the effectiveness of fulfilling corporate social responsibility. Divide CSR scores into high and low groups based on the annual industry average, with 2 for the high group and 1 for the low group.

4.2.4

Control variables

① ROA: the total return on assets of a listed company. ② Lev: the proportion of total liabilities to total assets of a listed company. ③ Size: company size. ④ Dual: If the two positions of Chairman and General Manager of the company are combined at the end of the previous year, 1 is taken; otherwise, 0 is taken. ⑤ Board: board size. ⑥ Indep: number of independent directors/size of directors. ⑦ PPE: Fixed asset ratio is calculated as fixed asset net value/total assets. ⑧ Cfo: net cash flow generated from operating activities. ⑨ HHI: Herfindahl index. ⑩ FirmFE and YearFE: Simultaneously control the sample company and year category.

The description of some variables is shown in Table 1.

Table

1.

Description of variables.

Variable

Description

TobinQA

The calculation method is market value A/total assets

TobinQC

The calculation method is market value B/total assets

CL

If the company received a regulatory inquiry letter from the securities exchange in the current year, it is set to 1; otherwise, it is set to 0

CSR

The social responsibility that companies undertake in their business activities

Size

Using the natural logarithm of the total assets of listed companies

PPE

Calculated as fixed asset net value/total assets

Cfo

Net cash flow generated from operating activities

Lev

Asset liability ratio, the proportion of total liabilities to total assets of a listed company

Indep

Number of independent directors/size of directors

Board

Board size, the logarithm of the number of directors plus 1

HHI

The sum of squares of the percentage of total revenue or total assets of each market competitor in an industry, used to measure changes in market share

Dual

If the two positions of Chairperson and General Manager of the company are combined at the end of the previous year, 1 is taken; otherwise, 0 is taken

ROA

Return on assets, the total return on assets of a listed company

To study the impact of inquiry supervision shocks on corporate value, this article establishes a model, as shown in Eq. (1):

TobinQ=β0+β1CL+βiControls+FirmFE+YearFE+ε.

(1)

To test whether CSR will have a protective effect on corporate value, this article uses the following variables for empirical testing, as shown in Eq. (2):

Table 2 presents the descriptive statistical results for each variable. The average value of CSR behavior is 1.483, indicating that the overall quality of CSR of the sample companies is not high.

After controlling for the fixed effects and year effects of the company, the regression test results for hypothesis H1 are shown in Table 3. Table 3 shows that the regression coefficient for the presence or absence of inquiry letters is significantly negative, indicating that the corporate value of companies receiving inquiry letters is more likely to decrease. Hypothesis H1 is validated.

Table

3.

Inquiry supervision and corporate value.

(1)

(2)

TobinQAt+1

TobinQAt+1

CL

−0.035**

−0.040**

(−1.89)

(−2.11)

Size

−0.003

(−0.06)

ROA

−0.379*

(−1.73)

PPE

0.513***

(2.68)

Cfo

0.626***

(3.69)

Lev

−0.049

(−0.25)

Indep

0.001

(0.01)

Board

0.005

(0.10)

HHI

0.446

(0.91)

Dual

−0.037

(−1.01)

Constant term

2.504***

2.338**

(125.67)

(2.13)

FirmFE

YES

YES

YearFE

YES

YES

N

14175

14175

R2

0.149

0.153

***, **, and * represent significant values at the 1%, 5%, and 10% levels, respectively. The statistical values of t are shown in parentheses. The same as in the following tables.

After controlling for the fixed effects and year effects of the company, the regression test results for hypothesis H2 are shown in Table 4. Table 4 shows that the regression coefficient of the interaction variable between CSR and whether an individual receives inquiry letters is significantly positive, indicating that CSR behavior can have a certain protective effect on the corporate value of companies receiving inquiry letters. Hypothesis H2 is verified.

Table

4.

Inquiry supervision, corporate social responsibility fulfillment, and corporate value.

Independent directors can effectively curb the selfish behavior of major shareholders and reflect the relative fairness of the board of directors. China has been striving to improve the relevant system of independent directors to ensure that independent directors can effectively supervise corporate governance. By studying the impact of board structure on corporate performance, Huang and Zhang[38] found that independent directors can have a positive impact on corporate performance. To test this inference, this article divides the proportion of independent directors into two groups based on the median proportion of independent directors and conducts regression tests. Table 5 shows that the protective effect of CSR behavior on corporate value is significant only for groups with a greater proportion of independent directors.

Table

5.

Heterogeneity analysis of the proportion of independent directors.

Mei and Li[39] believed that due to internal and external factors such as investment scale, professionals, and competitive pressure, institutional investors are more capable and motivated to participate in corporate governance than are individual investors. To leverage their supervisory advantages, institutional investors have the ability and motivation to promote their holding companies to improve the quality of information disclosure and reduce the degree of information asymmetry. Ye et al. [40] found that institutional investor shareholding helps improve the quality of company information disclosure. Li et al.[41] confirmed that the more concentrated and stable the holdings of securities investment funds are, the more helpful it is to improve the quality of information disclosure of their holding companies. At the same time, good corporate social responsibility behavior can attract institutional investors who focus on asset safety and stable operating funds, promote an increase in institutional investors, and convey positive signals to the outside world through the influence of institutional investors as market indicators, increase the reputation of the company, enhance the confidence of the capital market in the company, and thus have a positive impact on the value of the company. Therefore, institutional investors are motivated to include a company’s CSR performance in the context of information disclosure investment decisions. Therefore, this article proposes the hypothesis that there is a significant positive correlation between the shareholding ratio of institutional investors and corporate value. To test this inference, this article divides the shareholding ratio of institutional investors into two groups based on the median shareholding ratio of institutional investors and conducts a regression test. Table 6 shows that the protective effect of CSR behavior on corporate value is significant only for the group with a higher institutional investor shareholding ratio.

Table

6.

Heterogeneity analysis of the institutional investor shareholding ratio.

Lower shareholding ratio of institutional investors

Higher shareholding ratio of institutional investors

Regions with higher marketization indices have a more complete legal regulatory environment, better industry competition systems, more scientific government supervision mechanisms, and more rigorous intermediary market organizational structures. These external environmental factors have a positive impact on corporate governance. Cao and Li [42] found that in regions with higher levels of marketization, the more a company fulfills its social responsibility, the more it can enhance its value. Luo [43] found that with the acceleration of marketization, the level of corporate governance is gradually improving. Zhang [44] believed that economic resources in regions with a high degree of marketization are mainly allocated by the market, which not only allows effective resources to flow fully and reasonably to companies and departments with greater economic benefits but also reduces government intervention in companies and reduces their tax burden. The development of the product market promotes the gradual determination of product prices by the market, and market prices automatically play a regulatory role in the contradiction between product supply and demand. Once again, the development of the factor market also promotes the prosperity of the labor market, financial market, and technology market, which will inevitably bring good economic benefits. To test this inference, this article divides the total score of the marketization process into two groups based on the median of the total score and conducts regression tests. Table 7 shows that the protective effect of CSR behavior on corporate value is significant only for the group with a higher marketization process score.

Table

7.

Heterogeneity analysis of the marketization process score.

Alleviating regulatory pressure is an important motivation for companies to improve their social responsibility performance, and the regulatory effectiveness of annual report inquiry letters is influenced by the external legal environment. In areas with a higher level of rule of law, letter-receiving companies will face stricter penalties from regulatory agencies, and stakeholders will pay more attention to the company’s illegal and irregular behavior. As a result, inquiry supervision will cause more serious damage to the legitimacy of organizational regulations and norms and have a greater deterrent effect on letter-receiving companies. At this time, the receiving company will face higher levels of violation costs and litigation risks. It will not only reduce opportunistic behavior but also actively adopt compliant behavior to alleviate regulatory pressure. That is, a high level of rule of law will enhance the receiving company’s motivation to rectify the alienation of CSR behavior, thereby strengthening the optimization effect of inquiry supervision on CSR performance.

To test this inference, this article refers to the research of Mei et al.[45] and measures the level of regional rule of law by scoring the “development of intermediary organizations and legal system environment” in the marketization index. The sample is divided into two groups based on the median: higher rule of law level areas and lower rule of law level areas. Table 8 shows that the protective effect of CSR behavior on corporate value is significant only in areas with a higher level of rule of law.

Table

8.

Heterogeneity analysis of the rule of law level.

5.4.1

Changing the measurement method for whether inquiry letters were received in Model (1)

The method of changing variables is often used in robustness test. Using CLsum (the number of inquiry letters received by the company) instead of CL (whether the company has received inquiry letters) to regress the sample, the results show that the number of inquiry letters received has a negative impact on the value of the company.

5.4.2

Measurement method for replacing the dependent variable

This article replaces the original dependent variable TobinQA with TobinQC, which is another measurement of TobinQ, and replaces it with Model (1). The regression results in Table 10 show that the coefficient of whether the inquiry letter was received is still significantly negative, indicating that the conclusion has not changed substantially.

5.4.3

Changing the measurement method of CSR in Model (2)

Using Score, which represents the value of CSR, instead of CSR, to regress the sample, Table 11 shows that the regression coefficient of the interaction variable between the value of CSR and whether or not an individual receives inquiry letters is significantly positive, indicating that CSR can play a certain protective role in the corporate value of companies receiving inquiry letters, and the conclusion does not change substantially.

5.5

Endogeneity test

5.5.1

Heckman two-stage test

The issuance of inquiry letters by securities exchanges is often not random, and companies with insufficient information disclosure are more likely to receive inquiry letters. To address endogeneity issues caused by sample selection bias, this article uses the Heckman two-stage regression method. Imr is the inverse Mills ratio, commonly used to deal with sample selection bias issues. This article refers to Refs. [1, 10] and addresses whether the Big Four accounting firms (Big4) were audited and whether they received a standard audit opinion (Audit) as control variables. The results are shown in columns (1) and (2) of Table 12. The conclusions of this study are robust.

5.5.2

Inspection based on the extension of the receiving range of inquiry letters

Drawing on Ref. [7], the time of receiving inquiry letters is extended to the current year and the previous year, and CL is remeasured to further examine the impact of receiving letters in different time ranges on firm value. The regression results are shown in columns (3) and (4) of Table 12, which are consistent with the main test results, and the research conclusions remain robust.

5.5.3

Instrumental variable method

The endogeneity problem caused by bidirectional causality is the key issue that needs to be addressed in this article; that is, being regulated reduces the value of a company, but conversely, companies with lower values are more likely to be regulated. Therefore, the instrumental variable method is used to alleviate potential endogeneity problems. This article selects whether the auditor belongs to one of the Big Four accounting firms, the year of listing, and whether the company has received inquiry letters with a one-period lag as instrumental variables. This article conducts two-stage least squares regression (2SLS) on the hypotheses. The specific results are shown in columns (5) and (6) of Table 12. The results indicate that receiving inquiry letters has a negative impact on corporate value and that CSR can protect the corporate value of companies that receive inquiry letters. That is, the conclusion still holds after considering endogeneity issues.

6.

Conclusions

This article takes Chinese listed companies under inquiry supervision as the background and uses all A-share listed companies from 2015 to 2020 as research samples. Multiple regression analysis was used to empirically test the impact of inquiry supervision on corporate value and the reputation protection mechanism of CSR behavior. The research results indicate that inquiry supervision significantly reduces corporate value and that corporate social responsibility activities performed by companies before the issuance of inquiry supervision can provide certain protection for corporate value after they are subjected to inquiry supervision. Furthermore, the heterogeneity test results based on internal and external controls show that the reputation protection effect of CSR is significant only for companies with a high proportion of independent directors, companies with a high proportion of institutional investors investing in stocks, regions with a high degree of marketization, and regions with a high level of rule of law. This indicates that in an environment with mature market-oriented mechanisms, companies’ use of impression management is more effective in restoring their image; In contrast, in environments that rely more on relationships or rights to allocate resources, the importance of reputation is relatively weak. Compared to market competition, specific relationships often appear more reliable.

The theoretical significance of this article can be divided into the following two points. In the context of the gradual transformation of regulatory methods, inquiry supervision is gradually becoming the main regulatory tool for securities exchanges. First, this article provides an in-depth analysis of the channels through which inquiry supervision affects corporate value and explores the protective effect of CSR on corporate value, providing practical methods for better strategic management in daily business operations to respond to crisis events. Second, this article explores the magnitude of reputation protection in different environments and verifies that the reputation protection effect, as an informal mechanism, is easier to achieve in areas where formal mechanisms are well established; that is, formal and informal mechanisms complement each other, providing empirical insights for CSR governance.

In response to the above conclusions, this article proposes the following suggestions. First, listed companies should attach importance to the inquiry supervision of securities exchanges and cooperate with securities exchanges to actively fulfill their information disclosure obligations. Second, listed companies should proactively take appropriate measures, such as assuming corporate social responsibility and establishing a good public image, to cope with the pressure brought about by annual report inquiry letters and alleviate the negative impact of inquiry supervision. Third, after being inquired, companies located in areas with a higher level of marketization and rule of law are more likely to protect their corporate value through their previous behavior of assuming CSR. Therefore, when selecting a location for a listed company, priority should be given to areas with a higher level of marketization and rule of law. Fourth, after being questioned and regulated, companies with a greater proportion of independent directors and a greater proportion of institutional investors shareholding are more likely to achieve the protection of corporate value through their previous behavior of assuming CSR. Therefore, listed companies should actively increase the proportion of independent directors in the company and attract institutional investors to invest.

Due to limited data acquisition capabilities, there are still some shortcomings in this article, and future research can further analyze these aspects:First, this article has certain limitations in terms of data collection. Due to the relatively novel concepts of inquiry regulation and CSR reputation insurance, the relevant statistical data and empirical research are limited, resulting in relatively insufficient data support for our empirical analysis. Therefore, in future research, data support can be further enriched and the credibility and persuasiveness of the study can be improved through methods such as field research and case analysis.Second, there are many types of inquiry letters issued by stock exchanges, but this article only studies the impact of inquiry regulation on corporate value. In the future, further analysis can be conducted on the impact of different types of inquiry letters on corporate value.Third, companies in different industries may have different challenges and needs when facing regulatory and social responsibility issues, but this article does not conduct a detailed analysis of listed companies. Future research can explore in depth the application and effectiveness differences of inquiry regulation and CSR reputation insurance in different industries.Fourth, attention can be paid to the role of CSR reputation insurance in responding to emergencies and crisis management. The impact of emergencies and crises on companies cannot be ignored. How to prevent and resolve crises through fulfilling CSR is significant to the long-term development of companies and deserves further research and exploration.

Acknowledgements

This work was supported by the National Natural Science Foundation of China (72293573), the New Era Education Quality Project of Anhui Province (2022zyxwjxalk003), and the Fundamental Research Funds for the Central Universities (YD2160004004, WK2040000090).

Conflict of interest

The authors declare that they have no conflict of interest.

Inquiry supervision has a negative impact on corporate value.

When companies actively fulfill their social responsibilities, they can effectively alleviate the adverse impact of inquiry supervision on corporate value.

The role of corporate social responsibility (CSR) in reputation protection was examined in companies with a high proportion of independent directors, companies with a high shareholding ratio of institutional investors, a high degree of marketization, and regions with a high level of rule of law. It was verified that reputation protection, as an informal mechanism, is easier to play in areas where the formal mechanism is perfect. That is, formal and informal mechanisms complement each other.

Chen Y S, Deng Y L, Li Z. Effectiveness of the front-line regulation of the Chinese stock exchanges: Evidence from comment letters. Management World, 2019, 35 (3): 169–185. (in Chinese) DOI: 10.3969/j.issn.1002-5502.2019.03.012

[2]

Zhu J Y, Huang J C, Li X L, et al. The impact of nonadministrative punitive supervision on corporate social responsibility performance: Empirical evidence from annual report inquiry letters. Finance and Accounting Monthly, 2023, 44 (5): 52–59. (in Chinese) DOI: 10.19641/j.cnki.42-1290/f.2023.05.008

[3]

Li S N, Lou Y L, Wang Y T. How do the exchange comment letters affect audit fees: Risk disclosure and risk conduction effects. Audit and Economy Research, 2022, 37 (3): 52–61. (in Chinese) DOI: 10.3969/j.issn.1004-4833.2022.03.006

[4]

Lin H T, He Y R, Liu J Y. Financial report comment letters and firm’s financialization. Accounting Research, 2021, (9): 65–76. (in Chinese) DOI: 10.3969/j.issn.1003-2886.2021.09.005

[5]

Bae J, Choi W, Lim J. Corporate social responsibility: an umbrella or a puddle on a rainy day: Evidence surrounding corporate financial misconduct. European Financial Management, 2019, 26 (1): 77– 117. DOI: 10.1111/eufm.12235

[6]

Li X X, Rao P G, Yue H. Stock exchange comment letters and management earnings forecast. Management World, 2019, 35 (8): 173–188. (in Chinese) DOI: 10.3969/j.issn.1002-5502.2019.08.013

[7]

Cassell C A, Dreher L M, Myers L A. Reviewing the SEC’s review process: 10-K comment letters and the cost of remediation. Accounting Review, 2013, 88 (6): 1875–1908. DOI: 10.2308/accr-50538

[8]

Heese J, Khan M, Ramanna K. Is the SEC captured? Evidence from comment letter reviews. Journal of Accounting and Economics, 2017, 64 (1): 98–122. DOI: 10.1016/j.jacceco.2017.06.002

[9]

Johnston R, Petacchi R. Regulatory oversight of financial reporting: Securities and Exchange Commission comment letters. Contemporary Accounting Research, 2017, 34 (2): 1128–1155. DOI: 10.1111/1911-3846.12297

[10]

Zhao Z, Wang Y, Chen J. Non-administrative penalty supervision and enterprise investment efficiency: Evidence from the stock exchange comment letters. Nankai Economic Studies, 2022, (5): 181–200. (in Chinese) DOI: 10.14116/j.nkes.2022.05.010

[11]

Chen Y, Deng Y, Li Z. Does the nonpenalty regulation have information content: Evidence from inquiry letters. Journal of Financial Research, 2018, (4): 155–171. (in Chinese)

[12]

Shi X, Chen W, Liu F. Stock exchange comment letters and accounting conservatism. Economic Management Journal, 2021, 43 (12): 170–186. (in Chinese)

[13]

Gietzmann M B, Pettinicchio A K. External auditor reassessment of client business risk following the issuance of a comment letter by the SEC. European Accounting Review, 2013, 23 (1): 57–85. DOI: 10.1080/09638180.2013.774703

[14]

Gietzmann M B, Isidro H. Institutional investors’ reaction to SEC concerns about IFRS and US GAAP reporting. Journal of Business Finance & Accounting, 2013, 40: 796–841. DOI: 10.1111/jbfa.12027

[15]

Brown S V, Tian X L, Tucker J W. The spillover effect of SEC comment letters on qualitative corporate disclosure: Evidence from the risk factor disclosure. Contemporary Accounting Research, 2018, 35 (2): 622–656. DOI: 10.1111/1911-3846.12414

[16]

Bills K L, Cating R, Lin C, et al. The spillover effect of SEC comment letters through audit firms. Review of Accounting Studies, 2024: DOI: 10.1007/s11142-023-09819-z.

[17]

Wood D J. Measuring corporate social performance: A review. International Journal of Management Reviews, 2010, 12 (1): 50–84. DOI: 10.1111/j.1468-2370.2009.00274.x

[18]

Zhong H. The synthetic analysis on the functions of corporate philanthropy. China Industrial Economics, 2007, (2): 75–83. (in Chinese) DOI: 10.19581/j.cnki.ciejournal.2007.02.010

[19]

Meng Q, Hou C. Social responsibility performance and corporate financialization—Information supervision or reputation insurance. Economic Perspectives, 2020, (2): 45–58. (in Chinese)

[20]

Godfrey P C. The relationship between corporate philanthropy and shareholder wealth: A risk management perspective. The Academy of Management Review, 2005, 30 (4): 777–798. DOI: 10.5465/amr.2005.18378878

[21]

Chad C W, Lewis B W. Strategic silence: Withholding certification status as a hypocrisy avoidance tactic. Administrative Science Quarterly, 2017, 63 (1): 130–169. DOI: 10.1177/0001839217695089

[22]

Gao Y Q, Chen Y J, Zhang Y J. “Red scarf” or “green scarf”: A study on the motivation of charitable donations in private enterprises. Management World, 2012, (8): 106–114. (in Chinese) DOI: 10.19744/j.cnki.11-1235/f.2012.08.010

[23]

Fan J, Zhao Q, Tian Z. A study on insurance effects and restoration effects of corporate social responsibility in the context of a negative event. Chinese Journal of Management, 2020, 17 (5): 746–754. (in Chinese) DOI: 10.3969/j.issn.1672-884x.2020.05.013

[24]

Klein J, Dawar N. Corporate social responsibility and consumers’ attributions and brand evaluations in a product-harm crisis. International Journal of Research in Marketing, 2004, 21 (3): 203–217. DOI: 10.1016/j.ijresmar.2003.12.003

[25]

Hoi C K, Wu Q, Zhang H. Is corporate social responsibility (CSR) associated with tax avoidance? Evidence from irresponsible CSR activities. The Accounting Review, 2013, 88 (6): 2025–2059. DOI: 10.2308/accr-50544

[26]

Gong G, Huang X, Wu S, et al. Punishment by securities regulators, corporate social responsibility and the cost of debt. Journal of Business Ethics, 2021, 171 (2): 337–356. DOI: 10.1007/s10551-020-04438-z

[27]

Fu C, Ji L. Litigation risk and corporate charitable giving: An explanation from the perspective of reputation insurance. Nankai Business Review, 2017, 20 (2): 108–121. (in Chinese) DOI: 10.3969/j.issn.1008-3448.2017.02.010

[28]

Gu X, Wu Y, Huang Y, et al. Will fraud regulation promote corporate social responsibility. Review of Investment Studies, 2021, 40 (5): 33–65. (in Chinese)

[29]

Che X, Su Y. Research of corporate social responsibility report, violations and firm value. Economic Management Journal, 2018, 40 (10): 58–74. (in Chinese) DOI: 10.19616/j.cnki.bmj.2018.10.004

[30]

Fu W, Zeng H. Can non-punitive supervision restrain the management’s tone manipulation: Empirical evidence based on annual report text. Contemporary Finance and Economics, 2022, (3): 89–101. (in Chinese) DOI: 10.13676/j.cnki.cn36-1030/f.2022.03.004

[31]

Deng Y, Li Z, Chen Y. Front-line regulation of stock exchanges and top management turnover: Evidence based on inquiry letters. Management Review, 2020, 32 (4): 194–205. (in Chinese) DOI: 10.14120/j.cnki.cn11-5057/f.2020.04.016

[32]

Zhan X, Wang R. Financial pressure, expenditure structure and public service quality: Empirical analysis from the panel data of 229 cities in China. Reform, 2022, (2): 111–126. (in Chinese)

[33]

Ren J, Han Q. A comparative analysis of consumption decision-making under enterprise and industry crisis situations — Taking dairy products safety crisis as example. Collected Essays on Finance and Economics, 2017, (9): 94–104. (in Chinese) DOI: 10.3969/j.issn.1004-4892.2017.09.011

[34]

Pi M. The impact of nonpunitive regulation effect on stock price behavior: Based on the evidence in inquiry letter. Journal of Wuhan University of Technology (Information & Management Engineering), 2020, 42 (2): 160–167. (in Chinese) DOI: 10.3963/j.issn.2095-3852.2020.02.012

[35]

Godfrey P C, Merrill C B, Hansen J M. The relationship between corporate social responsibility and shareholder value: An empirical test of the risk management hypothesis. Strategic Management Journal, 2009, 30 (4): 425–445. DOI: 10.1002/smj.750

[36]

Hemingway C A, Maclagan P W. Managers’ personal values as drivers of corporate social responsibility. Journal of Business Ethics, 2004, 50 (1): 33–44. DOI: 10.1023/B:BUSI.0000020964.80208.c9

[37]

Zhang D L, Li S H. Social trust, political relationship and the private enterprises’ bank loans. Accounting Research, 2012, (8): 17–24. (in Chinese) DOI: 10.3969/j.issn.1003-2886.2012.08.003

[38]

Huang Y, Zhang X. A study on the impact of board structure on corporate performance. Journal of Shandong University of Technology (Social Sciences Edition), 2020, 36 (1): 25–30. (in Chinese) DOI: 10.3969/j.issn.1672-0040.2020.01.004

[39]

Mei J, Li Z. Research on the governance effect and heterogeneity of institutional investor shareholding: A corporate social responsibility perspective. Modern Management Science, 2022, (2): 117–124. (in Chinese) DOI: 10.3969/j.issn.1007-368X.2022.02.014

[40]

Ye J, Li D, Ding Q. Study on institutional investors’ share-holding and corporate transparency in a real environment—An analysis on endogenous test of omitted variables and simultaneous causality. Journal of Finance and Economics, 2009, 35 (1): 49–60. (in Chinese)

[41]

Li Z, Li D. The correlation between the volatility of fund holdings and the quality of company information disclosure: Empirical evidence from Shenzhen listed companies from 2005 to 2013. Securities Market Herald, 2015, (3): 58–63. (in Chinese)

[42]

Cao J, Li Z. Research on the correlation between social responsibility fulfillment of listed companies and corporate value. Communication of Finance and Accounting, 2013, 21: 104–107. (in Chinese) DOI: 10.16144/j.cnki.issn1002-8072.2013.21.020

[43]

Luo Y. Research on the relationship between marketization index, governance structure and corporate performance. Statistics and Decision, 2014, (24): 192–194. (in Chinese)

[44]

Zhang Y. The degree of marketization and the efficiency of provincial governments. Research on Development, 2011, (4): 46–48. (in Chinese) DOI: 10.3969/j.issn.1003-4161.2011.04.013

[45]

Mei B L, Guo X H, Ye J F. Legal environment and the spillover effect of comment letter: Based on earnings management perspective. Accounting Research, 2021, (6): 30–41. (in Chinese) DOI: 10.3969/j.issn.1003-2886.2021.06.003

Chen Y S, Deng Y L, Li Z. Effectiveness of the front-line regulation of the Chinese stock exchanges: Evidence from comment letters. Management World, 2019, 35 (3): 169–185. (in Chinese) DOI: 10.3969/j.issn.1002-5502.2019.03.012

[2]

Zhu J Y, Huang J C, Li X L, et al. The impact of nonadministrative punitive supervision on corporate social responsibility performance: Empirical evidence from annual report inquiry letters. Finance and Accounting Monthly, 2023, 44 (5): 52–59. (in Chinese) DOI: 10.19641/j.cnki.42-1290/f.2023.05.008

[3]

Li S N, Lou Y L, Wang Y T. How do the exchange comment letters affect audit fees: Risk disclosure and risk conduction effects. Audit and Economy Research, 2022, 37 (3): 52–61. (in Chinese) DOI: 10.3969/j.issn.1004-4833.2022.03.006

[4]

Lin H T, He Y R, Liu J Y. Financial report comment letters and firm’s financialization. Accounting Research, 2021, (9): 65–76. (in Chinese) DOI: 10.3969/j.issn.1003-2886.2021.09.005

[5]

Bae J, Choi W, Lim J. Corporate social responsibility: an umbrella or a puddle on a rainy day: Evidence surrounding corporate financial misconduct. European Financial Management, 2019, 26 (1): 77– 117. DOI: 10.1111/eufm.12235

[6]

Li X X, Rao P G, Yue H. Stock exchange comment letters and management earnings forecast. Management World, 2019, 35 (8): 173–188. (in Chinese) DOI: 10.3969/j.issn.1002-5502.2019.08.013

[7]

Cassell C A, Dreher L M, Myers L A. Reviewing the SEC’s review process: 10-K comment letters and the cost of remediation. Accounting Review, 2013, 88 (6): 1875–1908. DOI: 10.2308/accr-50538

[8]

Heese J, Khan M, Ramanna K. Is the SEC captured? Evidence from comment letter reviews. Journal of Accounting and Economics, 2017, 64 (1): 98–122. DOI: 10.1016/j.jacceco.2017.06.002

[9]

Johnston R, Petacchi R. Regulatory oversight of financial reporting: Securities and Exchange Commission comment letters. Contemporary Accounting Research, 2017, 34 (2): 1128–1155. DOI: 10.1111/1911-3846.12297

[10]

Zhao Z, Wang Y, Chen J. Non-administrative penalty supervision and enterprise investment efficiency: Evidence from the stock exchange comment letters. Nankai Economic Studies, 2022, (5): 181–200. (in Chinese) DOI: 10.14116/j.nkes.2022.05.010

[11]

Chen Y, Deng Y, Li Z. Does the nonpenalty regulation have information content: Evidence from inquiry letters. Journal of Financial Research, 2018, (4): 155–171. (in Chinese)

[12]

Shi X, Chen W, Liu F. Stock exchange comment letters and accounting conservatism. Economic Management Journal, 2021, 43 (12): 170–186. (in Chinese)

[13]

Gietzmann M B, Pettinicchio A K. External auditor reassessment of client business risk following the issuance of a comment letter by the SEC. European Accounting Review, 2013, 23 (1): 57–85. DOI: 10.1080/09638180.2013.774703

[14]

Gietzmann M B, Isidro H. Institutional investors’ reaction to SEC concerns about IFRS and US GAAP reporting. Journal of Business Finance & Accounting, 2013, 40: 796–841. DOI: 10.1111/jbfa.12027

[15]

Brown S V, Tian X L, Tucker J W. The spillover effect of SEC comment letters on qualitative corporate disclosure: Evidence from the risk factor disclosure. Contemporary Accounting Research, 2018, 35 (2): 622–656. DOI: 10.1111/1911-3846.12414

[16]

Bills K L, Cating R, Lin C, et al. The spillover effect of SEC comment letters through audit firms. Review of Accounting Studies, 2024: DOI: 10.1007/s11142-023-09819-z.

[17]

Wood D J. Measuring corporate social performance: A review. International Journal of Management Reviews, 2010, 12 (1): 50–84. DOI: 10.1111/j.1468-2370.2009.00274.x

[18]

Zhong H. The synthetic analysis on the functions of corporate philanthropy. China Industrial Economics, 2007, (2): 75–83. (in Chinese) DOI: 10.19581/j.cnki.ciejournal.2007.02.010

[19]

Meng Q, Hou C. Social responsibility performance and corporate financialization—Information supervision or reputation insurance. Economic Perspectives, 2020, (2): 45–58. (in Chinese)

[20]

Godfrey P C. The relationship between corporate philanthropy and shareholder wealth: A risk management perspective. The Academy of Management Review, 2005, 30 (4): 777–798. DOI: 10.5465/amr.2005.18378878

[21]

Chad C W, Lewis B W. Strategic silence: Withholding certification status as a hypocrisy avoidance tactic. Administrative Science Quarterly, 2017, 63 (1): 130–169. DOI: 10.1177/0001839217695089

[22]

Gao Y Q, Chen Y J, Zhang Y J. “Red scarf” or “green scarf”: A study on the motivation of charitable donations in private enterprises. Management World, 2012, (8): 106–114. (in Chinese) DOI: 10.19744/j.cnki.11-1235/f.2012.08.010

[23]

Fan J, Zhao Q, Tian Z. A study on insurance effects and restoration effects of corporate social responsibility in the context of a negative event. Chinese Journal of Management, 2020, 17 (5): 746–754. (in Chinese) DOI: 10.3969/j.issn.1672-884x.2020.05.013

[24]

Klein J, Dawar N. Corporate social responsibility and consumers’ attributions and brand evaluations in a product-harm crisis. International Journal of Research in Marketing, 2004, 21 (3): 203–217. DOI: 10.1016/j.ijresmar.2003.12.003

[25]

Hoi C K, Wu Q, Zhang H. Is corporate social responsibility (CSR) associated with tax avoidance? Evidence from irresponsible CSR activities. The Accounting Review, 2013, 88 (6): 2025–2059. DOI: 10.2308/accr-50544

[26]

Gong G, Huang X, Wu S, et al. Punishment by securities regulators, corporate social responsibility and the cost of debt. Journal of Business Ethics, 2021, 171 (2): 337–356. DOI: 10.1007/s10551-020-04438-z

[27]

Fu C, Ji L. Litigation risk and corporate charitable giving: An explanation from the perspective of reputation insurance. Nankai Business Review, 2017, 20 (2): 108–121. (in Chinese) DOI: 10.3969/j.issn.1008-3448.2017.02.010

[28]

Gu X, Wu Y, Huang Y, et al. Will fraud regulation promote corporate social responsibility. Review of Investment Studies, 2021, 40 (5): 33–65. (in Chinese)

[29]

Che X, Su Y. Research of corporate social responsibility report, violations and firm value. Economic Management Journal, 2018, 40 (10): 58–74. (in Chinese) DOI: 10.19616/j.cnki.bmj.2018.10.004

[30]

Fu W, Zeng H. Can non-punitive supervision restrain the management’s tone manipulation: Empirical evidence based on annual report text. Contemporary Finance and Economics, 2022, (3): 89–101. (in Chinese) DOI: 10.13676/j.cnki.cn36-1030/f.2022.03.004

[31]

Deng Y, Li Z, Chen Y. Front-line regulation of stock exchanges and top management turnover: Evidence based on inquiry letters. Management Review, 2020, 32 (4): 194–205. (in Chinese) DOI: 10.14120/j.cnki.cn11-5057/f.2020.04.016

[32]

Zhan X, Wang R. Financial pressure, expenditure structure and public service quality: Empirical analysis from the panel data of 229 cities in China. Reform, 2022, (2): 111–126. (in Chinese)

[33]

Ren J, Han Q. A comparative analysis of consumption decision-making under enterprise and industry crisis situations — Taking dairy products safety crisis as example. Collected Essays on Finance and Economics, 2017, (9): 94–104. (in Chinese) DOI: 10.3969/j.issn.1004-4892.2017.09.011

[34]

Pi M. The impact of nonpunitive regulation effect on stock price behavior: Based on the evidence in inquiry letter. Journal of Wuhan University of Technology (Information & Management Engineering), 2020, 42 (2): 160–167. (in Chinese) DOI: 10.3963/j.issn.2095-3852.2020.02.012

[35]

Godfrey P C, Merrill C B, Hansen J M. The relationship between corporate social responsibility and shareholder value: An empirical test of the risk management hypothesis. Strategic Management Journal, 2009, 30 (4): 425–445. DOI: 10.1002/smj.750

[36]

Hemingway C A, Maclagan P W. Managers’ personal values as drivers of corporate social responsibility. Journal of Business Ethics, 2004, 50 (1): 33–44. DOI: 10.1023/B:BUSI.0000020964.80208.c9

[37]

Zhang D L, Li S H. Social trust, political relationship and the private enterprises’ bank loans. Accounting Research, 2012, (8): 17–24. (in Chinese) DOI: 10.3969/j.issn.1003-2886.2012.08.003

[38]

Huang Y, Zhang X. A study on the impact of board structure on corporate performance. Journal of Shandong University of Technology (Social Sciences Edition), 2020, 36 (1): 25–30. (in Chinese) DOI: 10.3969/j.issn.1672-0040.2020.01.004

[39]

Mei J, Li Z. Research on the governance effect and heterogeneity of institutional investor shareholding: A corporate social responsibility perspective. Modern Management Science, 2022, (2): 117–124. (in Chinese) DOI: 10.3969/j.issn.1007-368X.2022.02.014

[40]

Ye J, Li D, Ding Q. Study on institutional investors’ share-holding and corporate transparency in a real environment—An analysis on endogenous test of omitted variables and simultaneous causality. Journal of Finance and Economics, 2009, 35 (1): 49–60. (in Chinese)

[41]

Li Z, Li D. The correlation between the volatility of fund holdings and the quality of company information disclosure: Empirical evidence from Shenzhen listed companies from 2005 to 2013. Securities Market Herald, 2015, (3): 58–63. (in Chinese)

[42]

Cao J, Li Z. Research on the correlation between social responsibility fulfillment of listed companies and corporate value. Communication of Finance and Accounting, 2013, 21: 104–107. (in Chinese) DOI: 10.16144/j.cnki.issn1002-8072.2013.21.020

[43]

Luo Y. Research on the relationship between marketization index, governance structure and corporate performance. Statistics and Decision, 2014, (24): 192–194. (in Chinese)

[44]

Zhang Y. The degree of marketization and the efficiency of provincial governments. Research on Development, 2011, (4): 46–48. (in Chinese) DOI: 10.3969/j.issn.1003-4161.2011.04.013

[45]

Mei B L, Guo X H, Ye J F. Legal environment and the spillover effect of comment letter: Based on earnings management perspective. Accounting Research, 2021, (6): 30–41. (in Chinese) DOI: 10.3969/j.issn.1003-2886.2021.06.003

The calculation method is market value A/total assets

TobinQC

The calculation method is market value B/total assets

CL

If the company received a regulatory inquiry letter from the securities exchange in the current year, it is set to 1; otherwise, it is set to 0

CSR

The social responsibility that companies undertake in their business activities

Size

Using the natural logarithm of the total assets of listed companies

PPE

Calculated as fixed asset net value/total assets

Cfo

Net cash flow generated from operating activities

Lev

Asset liability ratio, the proportion of total liabilities to total assets of a listed company

Indep

Number of independent directors/size of directors

Board

Board size, the logarithm of the number of directors plus 1

HHI

The sum of squares of the percentage of total revenue or total assets of each market competitor in an industry, used to measure changes in market share

Dual

If the two positions of Chairperson and General Manager of the company are combined at the end of the previous year, 1 is taken; otherwise, 0 is taken

ROA

Return on assets, the total return on assets of a listed company

***, **, and * represent significant values at the 1%, 5%, and 10% levels, respectively. The statistical values of t are shown in parentheses. The same as in the following tables.

DownLoad:

DownLoad: