Chenxi Wang is a postgraduate student at the School of Management, University of Science and Technology of China. Her research mainly focuses on risk and strategic management

Lei Zhou is an Associate Professor at the School of Public Affairs, University of Science and Technology of China (USTC). He received his Ph.D. degree from USTC in 2014. His research mainly focuses on risk and strategic management

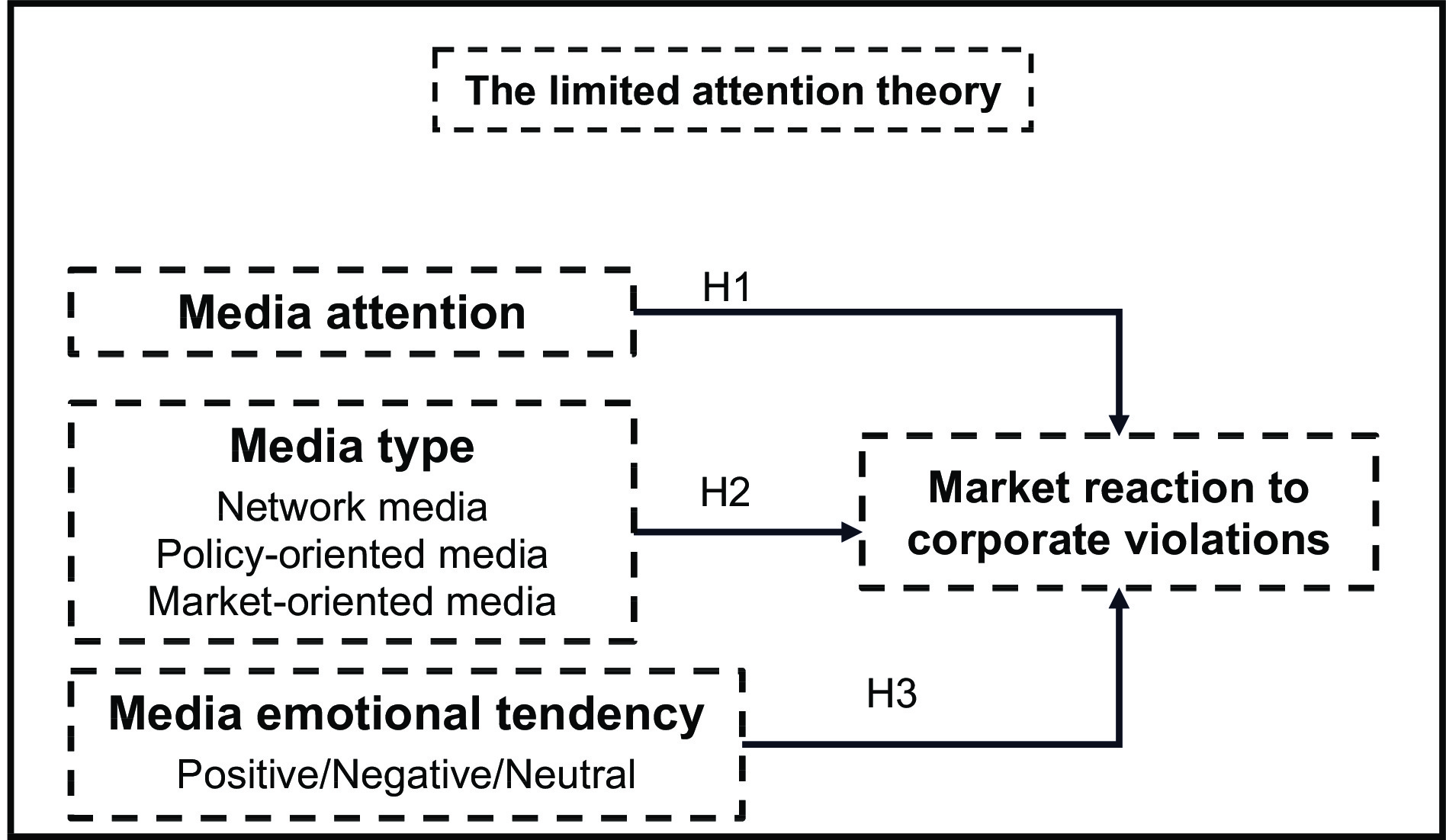

Reducing market volatility and achieving high-quality development are important tasks for the Chinese capital market at the present stage. Based on the asset pricing role of media, this study used the event study to empirically examine the impact, as well as the heterogeneity from type and emotional tendency, of media attention on the market reaction to corporate violations from the perspective of limited attention. The results showed that the media’s prior attention to the listed company has a significantly negative impact on the market reaction after the company’s violation. The attention of network media and policy-oriented media has a significantly negative correlation with the market reaction after the company’s violation, while market-oriented media has no significant impact. Compared with neutral media attention, negative and positive media attention trigger more severe negative market reaction after company violations. Furthermore, the negative impact of media attention on the market reaction after corporate violations is mainly manifested in non-state-owned enterprises. The results demonstrate the important role of media attention in asset pricing and have important practical significance for better playing the role of the media, protecting the rights and interests of investors and achieving high-quality development of the capital market.

Graphical Abstract

Media attention, media type, media emotional tendency, and market reaction to listed companies’ violations.

Abstract

Reducing market volatility and achieving high-quality development are important tasks for the Chinese capital market at the present stage. Based on the asset pricing role of media, this study used the event study to empirically examine the impact, as well as the heterogeneity from type and emotional tendency, of media attention on the market reaction to corporate violations from the perspective of limited attention. The results showed that the media’s prior attention to the listed company has a significantly negative impact on the market reaction after the company’s violation. The attention of network media and policy-oriented media has a significantly negative correlation with the market reaction after the company’s violation, while market-oriented media has no significant impact. Compared with neutral media attention, negative and positive media attention trigger more severe negative market reaction after company violations. Furthermore, the negative impact of media attention on the market reaction after corporate violations is mainly manifested in non-state-owned enterprises. The results demonstrate the important role of media attention in asset pricing and have important practical significance for better playing the role of the media, protecting the rights and interests of investors and achieving high-quality development of the capital market.

Public Summary

Based on the asset pricing role of media, this study used the event study to empirically examine the impact, as well as the heterogeneity from type and emotional tendency, of media attention on the market reaction to corporate violations from the perspective of limited attention.

The media’s prior attention to listed companies has a significant negative impact on the market reaction after corporate violations.

There is heterogeneity in media types and emotional effects of media coverage.

Recently, all-solid-state Li batteries (ASSLBs) have attracted great interest for their potential to offer higher energy density and better safety[1, 2]. However, the substitution of liquid-solid contact with solid-solid contacts brings significant challenges[3-5]. For example, the requirements for the cathodes in ASSLBs are no longer the same as those in commercial Li-ion batteries using liquid electrolytes.

The difference is at least twofold. On the one hand, insufficient contact between brittle, nondeformable solid particles would lead to high resistance for Li+ transport. Therefore, to maintain good interfacial contact, cathode particles should preferably show good deformability[6]. On the other hand, to improve ionic diffusion in cathodes, the addition of SSEs (solid-state electrolytes) is usually needed in the composite cathode, but these electrochemically inert materials inevitably decrease the mass loading of active materials and thus the energy densities[7]. However, if the cathode itself is highly Li-ion conductive, the composite cathode would no longer need much solid electrolyte to make its ionic transport sufficiently fast. According to Gao et al.[5], the composite cathode of ASSLBs should have a high ionic conductivity of more than 10−4 S∙cm−1. Therefore, to decrease or eliminate the need for solid electrolytes in the composite cathode, the ionic conductivity of the cathode active material itself should at least reach this level. Unfortunately, realizing the two characteristics mentioned above (especially the deformability) in the present mainstream cathodes is rather difficult because they are all brittle, poorly deformable oxides[8, 9].

Chlorides have good deformability and high oxidation potential; in addition, their open structures can support good ionic conduction, giving them great potential as cathode materials. Most chlorides are soluble in polar solvents, so there is not much research on such electrode materials in the past[8]. The deformable spinel-type chloride Li2MIICl4 (MII = Mn, Mg, Fe, Cd, V, Cr, etc.) may contain transition-metal cations and thus could potentially serve as the cathode. Among Li2MCl4-type chlorides, Li2MnCl4 has the highest Li+ conductivity (4×10−6 S∙cm−1, 25 °C)[10], and the nonstoichiometric Li2−2xMn1+xCl4 can reach 1.5×10−5 S∙cm−1[11], but still does not satisfy the requirements. To be a qualified cathode active material (CAM), it needs to be sufficiently conductive.

In this work, the aliovalent substitution Li2-xMn1-xZrxCl4 with high Li+ conductivity (up to 1.60×10−4 S∙cm−1) was synthesized by mechanical ball milling, and the ionic conductivity and activation energy of the powder were investigated. Moreover, the remarkable reversibility of the all-solid-state Li-In/Li6PS5Cl-Li3InCl6/LiMn0.5Zr0.5Cl4 cell over 200 cycles was demonstrated.

2.

Materials and methods

2.1

Preparation of materials

All preparations were conducted under an Ar atmosphere. For the preparation of as-milled Li2−2xMn1−xZrxCl4, stoichiometric amounts of precursors LiCl (99.99%, Alfa Aesar), MnCl2 (99.9%, Aladdin), and ZrCl4 (98%, Alfa Aesar) were hand-mixed in the mortar by pestle for homogenization. Subsequently, the as-mixed stoichiometric mixture was mechanically milled at 500 r/min for 25 h in an 80 mL ZrO2 vial with ZrO2 balls (ф = 5 mm) using a PULVERISETTE 7 premium line (Fritsch GmbH), and the ball-to-powder weight ratio was 15∶1.

To obtain annealed samples, as-milled powder samples were sealed in a quartz ampoule under vacuum and then heat-treated at 350 °C for 5 h with a heating rate of 5 °C∙min−1 and naturally cooled to room temperature. Li3InCl6 (LIC) was prepared by mechanical milling and subsequent heating treatment. A stoichiometric amount of LiCl (99.99%, Alfa Aesar) and InCl3 (99.99%, Alfa Aesar) was milled under the same conditions as for Li2−2xMn1+xCl4, which was followed by annealing at 350 °C for 5 h with Ar flow.

2.2

Material characterization

Powder X-ray diffraction (XRD) patterns were collected on a Rigaku Ultima IV diffractometer with Cu Kα1 radiation (λ = 1.54178 Å). Prior to the XRD measurements, the powder samples were sealed in Kapton film in an Ar-filled glovebox to avoid air exposure. The scanning speed was 10° per minute, and the scanning range was from 20° to 80°.

2.3

Conductivity measurements

Li+ conductivity was measured by electrochemical impedance spectroscopy (EIS) on a BioLogic MTZ-35 impedance analyzer. Prior to the AC impedance spectroscopy measurements, the powders were cold pressed into pellets at 370 MPa, and then Au electrodes were sputtered on the pellet surfaces as blocking electrodes. The thickness of the pellet was between 0.6–0.8 mm. The above procedures were performed inside an Ar-filled glovebox to avoid air exposure. The frequency range of the EIS measurement was from 1 Hz to 35 MHz with a 50 mV driving potential amplitude. The electronic conductivity was determined by direct current (DC) polarization measurements on a Chenhua CHI630e. The cold-pressed pellets were measured at 25 °C with an applied voltage of 1 V.

2.4

Electrochemical characterization

All ASSLB preparation processes were performed inside an Ar-filled glove box. The cathode composite powder was prepared by mixing as-milled LiMn0.5Zr0.5Cl4 (LMZC5) and an electron-conductive additive carbon nanotube (CNT) using a ball mill apparatus (Fritsch GmbH). The electrochemical stability window (ESW) was evaluated by linear sweep voltammetry (LSV) measurements on a Li/Li6PS5Cl-LMZC5/LMZC5+CNT (weight ratio: LMZC5/CNT = 70/30) semiblocking cell[12]. To assemble an all-solid-state battery, approximately 40 mg LIC was added into a polyetheretherketone (PEEK) die with a diameter of 10 mm and cold pressed at 1 ton as the SSE layer. To avoid reaction between LIC and the Li-In anode, 50 mg Li6PS5Cl (Hefei Kejing, 99%) was further added and pressed at 1.5 tons. Then, 10 mg of the cathode composite powder was dispersed on the LIC side of the double-layer solid electrolyte and pressed again at 2 tons. Finally, a piece of indium foil (0.1 mm thick, 10 mm diameter) was placed at the surface of the Li6PS5Cl layer, and a piece of lithium foil (0.03 mm thick, 10 mm diameter) was then placed on the indium foil. The ASSLB was cycled under a stack pressure of 2 tons at 25 °C using a LAND CT2001A cycler within the potential window of 1.5–3.6 V (vs Li+/LiIn).

3.

Results and discussion

The X-ray diffraction (XRD) patterns of the as-milled Li2-2xMn1-xZrxCl4 (x = 0, 0.1, 0.2, 0.3, 0.4, 0.5, 0.6, abbreviated as LMC, LMZC1, LMZC2, LMZC3, LMZC4, LMZC5 and LMZC6, respectively) powder samples are shown in Fig. 1. In the range of 0 ⩽x⩽ 0.4, the XRD patterns match well with Li2MnCl4 (ICSD No. 97-000-1984)[13]. The main characteristic peaks of the two components LMZC5 and LMZC6 are also consistent with Li2MnCl4, while a weak characteristic peak belonging to the Li2ZrCl6 impurity can be observed at approximately 32° in LMZC5. Further substitution of x = 0.6 resulted in more obvious peaks of Li2ZrCl6. The results indicate that the mutual solubility of Zr4+ in Li2MnCl4 should be between 0.4 and 0.5. In addition, it can be observed from Fig. 1b that with increasing doping ratio, the characteristic peak shifts to a high angle, which indicates that Zr4+ has been successfully doped into the structure of Li2MnCl4. Due to the smaller ionic radius of Zr4+ (compared to Mn2+) and the generation of Li+ vacancies, the lattice constant of the material decreases with increasing doping ratio.

Figure

1.

(a) XRD patterns of as-milled Li2−2xMn1−xZrxCl4. (b) Partial enlarged image of (a).

The crystallinity of samples obtained by mechanical ball milling is very low, while previous studies have shown that for chloride solid electrolytes, the highly crystalline phases generally tend to have higher ionic conductivity[14, 15]. Therefore, the as-milled samples were annealed at 350 °C for 5 h to improve the crystallinity. The XRD patterns of the annealed samples are shown in Fig. 2. The main characteristic peaks are the same as before, while the intensities are much higher, and peaks with lower intensity that cannot be observed in the as-milled samples can also be clearly displayed, indicating that the annealing process greatly improved the crystallinity. In addition, no impurity peak was found in the annealed samples for all different doping ratios, which means that the annealed samples are all single-phase materials with Li2MnCl4 structures. As mentioned above, weak characteristic peaks of α-Li2ZrCl6 can be observed in the as-milled samples for LMZC5 and LMZC6, but peaks of the corresponding high-temperature phase (β-Li2ZrCl6)[16] were not found in the annealed samples. This phenomenon may be explained by the fact that the as-milled samples are in a metastable state, and after annealing, the structure is more stable; thus, the solid solubility of Zr4+ is improved.

Figure

2.

XRD patterns of the 350 °C-annealed Li2−2xMn1−xZrxCl4 powder samples.

Fig. 3a, b displays the typical Nyquist plots of the as-milled and annealed samples, respectively. The impedance spectra were fitted with the equivalent circuit consisting of one parallel constant phase element (CPE)/resistor (R) in series with another CPE. The low electronic conductivities of the as-milled and annealed samples were measured, as shown in Fig. 3c, d. The Li+ conductivities and electronic conductivities of all samples are listed in Table 1, 2. With the aliovalent substitution of Zr4+, the Li+ conductivities of the as-milled samples can reach ~10−4 S∙cm−1. However, the Li+ conductivity decreased by two orders of magnitude after annealing at 350 °C for 5 h. Since the Li+ conductivities of the annealed samples are all on the order of 10−6 S∙cm−1, which cannot satisfy the requirements of assembling all-solid-state batteries, they will not be discussed in the following.

Figure

3.

Conductivity of LMZC5 under different processing conditions. (a, b) Nyquist plots of the as-milled (a) and 350 °C-annealed (b) LMZC5 at 25 °C. (c, d) Chronoamperometry results for the as-milled (c) and 350 °C-annealed (d) LMZC5 at 25 °C with a voltage step of 1 V.

The Arrhenius plots derived from the Nyquist plots at different temperatures (Fig. 4a) showed good linearity. The ionic conductivities at 25 °C and activation energies (Ea) determined according to the Arrhenius equation of Li2−2xMn1−xZrxCl4 are shown in Fig. 4b. The ionic conductivities of the samples increase gradually with increasing Zr4+ substitution, while the Ea values gradually decrease with increasing Zr4+ content. The highest ionic conductivity (1.6×10−4 S∙cm−1 at 25 °C) is achieved for x = 0.5, which also exhibits the lowest activation energy (0.381 eV). However, further substitution of x = 0.6 resulted in a decrease in the ionic conductivity. According to the previous XRD patterns, weak peaks of Li2ZrCl6 can be observed in LMZC5 and LMZC6. While the reported ionic conductivity of Li2ZrCl6 is higher (~4×10−4 S∙cm−1)[17], it seems that the presence of Li2ZrCl6 in LMZC6 does not further improve its ionic conductivity. It could be reasonably inferred that the ionic conductivity of the sample is still mainly affected by the structural change of Li2MnCl4, and the content of Li2ZrCl6 is too low to have a significant impact on its ionic conductivity. Last but not least, it should be noted that all the conductivity measurements above were conducted directly on cold-pressed powders without any heat treatment. Regardless, a rather high ionic conductivity above 10−4 S∙cm−1 can still be achieved for as-milled LMZC5, so this material should be highly deformable[18].

Figure

4.

Conductivity and activation energy evolution upon Zr4+ substitution. (a) Arrhenius plots of Li+ conductivity for as-milled Li2−2xMn1−xZrxCl4. (b) Ionic conductivities at 25 °C and activation energies of as-milled Li2-2xMn1-xZrxCl4.

The electrochemical stability window (ESW) of LMZC5 was calculated by using the established scheme[19-21] based on the Materials Project[22] database. The equilibrium voltage profile and corresponding phase equilibria as a function of applied potential referenced to Li/Li+ are shown in Fig. 5. The electrochemical reduction originates from Mn2+ becoming Mn metal, while the oxidation process originates from the Cl− anion chemistry with the product of Cl2. It shows a wide electrochemical window with an oxidation potential of 4.25 V (vs Li/Li+) and a reduction potential of 2.03 V (vs Li/Li+).

Figure

5.

Thermodynamic equilibrium voltage profiles and the phase equilibria for LMZC5 based on DFT calculations.

The ESW predicted above is verified by linear sweep voltammetry (LSV) measurements of all-solid-state Li/Li6PS5Cl/LMZC5/LMZC5+C/SS semiblocking cells. The LMZC5+C composite is a mixture of 70 wt% as-milled LMZC5 and 30 wt% carbon. The composite layer is used to improve the electron conduction, thereby making the redox peaks more easily detectable. The LSV results (Fig. 6) reveal multiple reduction peaks below 2 V (vs Li/Li+), along with one oxidation peak above 4 V (vs Li/Li+), which are consistent with the calculated values. The high Li+ conductivity, good deformability and high oxidation potential above 4 V make LMZC5 very suitable as a cathode material for ASSLBs.

Figure

6.

LSV curves of the Li/Li6PS5Cl-LMZC5/LMZC5+C cell at 0.1 mV∙s−1. The measurements were conducted at room temperature. (a) 0–3.1 V. (b) 3–5 V.

Finally, the as-milled LMZC5 was integrated as the CAM into an all-solid-state cell. Benefiting from its high ionic conductivity, no solid electrolyte is necessary for the cathode, and electronic conduction in the cathode is fulfilled by electronic conductive agents (CNTs, 30 wt%). The all-solid-state battery uses LIC obtained by 350 °C annealing as the electrolyte. Since its reduction potential is higher than that of the Li-In alloy (0.62 V vs Li/Li+), a layer of Li6PS5Cl is used to separate the negative electrode side to avoid the reaction. The cell was cycled at 0.1 C between 1.5 V and 3.6 V at 25 °C. Mn has various valence states, such as Mn2+, Mn3+ and Mn4+. Among LiMn0.5Zr0.5Cl4, if Mn2+ rises to Mn3+ during charging (LiMn0.5Zr0.5Cl4 ↔ 0.5Li + Li0.5Mn0.5Zr0.5Cl4), the theoretical capacity should be 60 mA∙h∙g−1. Meanwhile, referring to the calculated results (Fig. 5), the electrochemical mechanism may also be a conversion reaction (LiMn0.5Zr0.5Cl4 + Li ↔ 2LiCl + 0.5ZrCl4 + 0.5Mn), in which case the theoretical capacity should be approximately 121 mA∙h∙g−1.

The charge-discharge voltage profiles at the 1st, 2nd, 100th, and 200th cycles of the battery are shown in Fig. 7a. The initial charge capacity is extremely low, only 1.6 mA∙h∙g−1, while the discharge capacity is 52.4 mA∙h∙g−1. The electrochemical reaction occurred during the discharge process, so it is possible that the cycling takes place through the conversion reaction mentioned above: LiMn0.5Zr0.5Cl4 + Li ↔ 2LiCl + 0.5ZrCl4 + 0.5Mn. A voltage plateau appeared at approximately 2.5 V (vs Li/Li+) with some fluctuations, which may be caused by the decrease in the ionic conductivity affected by the conversion reaction during the discharge process. Given that the discharge capacity reaches only approximately half of the theoretical capacity, there is still an amount of LMZC5 that does not participate in the conversion reaction, which is helpful for ion diffusion in the cathode. The rate capability of the cell is shown in Fig. 7b. Due to the poor cycling stability associated with the conversion reaction, the capacity gradually decreases, especially in the first few cycles. However, upon each increase in the cycling rate, the capacity only dropped slightly; the average capacities at 0.33 C, 0.5 C and 1 C are 22.1 mA∙h∙g−1, 18.6 mA∙h∙g−1, and 14.4 mA∙h∙g−1, respectively. Fig. 7c displays the cycling performance of the cell at a rate of 0.1 C. The cell showed a quick capacity decay during the first few cycles and exhibited considerable cyclability with a reversible discharge capacity of 18 mA∙h∙g−1 after 15 cycles. It maintained a 99.1% Coulombic efficiency and a 14.3 mA∙h∙g−1 discharge capacity after 200 cycles, corresponding to a 79% capacity retention with respect to the fifth cycle. This is the first time that the chloride cathode material has achieved stable and long cycles in an all-solid-state lithium battery, indicating that the development of chloride cathode materials suitable for all-solid-state lithium batteries is a very worthwhile direction to explore.

Figure

7.

Electrochemical performance of the Li-In/Li6PS5Cl-LIC/LMZC5 cell at 25 °C. (a) Charge and discharge profiles at 0.1 C. (b) Rate performance. (c) Long-term cycling performance at 0.1 C.

To probe the reaction mechanism during cycling, ex situ XRD was conducted on LMZC5 at different depths of discharge, and the results are displayed in Fig. 8. As discharge proceeds, a diffraction peak that does not belong to LMZC5 emerges at approximately 25°, and its intensity keeps increasing with respect to that of LMZC5; at the end of discharge, a significant amount of LMZC5 was still observed, consistent with the low capacities observed in Fig. 7. The additional peak at approximately 25° cannot be indexed to any of the known compounds (including the products speculated by the calculation in Fig. 5), so the specific reaction mechanism cannot be determined. However, the fact that this peak cannot possibly arise from LMZC5 (Fig. 8a) indicates the emergence of new compounds during lithiation. That is, the reaction should follow a conversion mechanism instead of intercalation. It is known that the conversion-type cathode usually has difficulty achieving excellent cycling stability or capacities that are close to the theoretical value, no matter whether the cathode is deformable or not; a typical example is the S cathode in Li-S batteries. This seems to explain why LMZC5 is deformable but still shows poor cycling stability and low capacities.

Figure

8.

(a) Ex situ XRD patterns of LMZC5 at different depths of discharge (DoDs). The DoD of each XRD pattern is indicated in (b). (b) The initial discharge profile at 0.1 C, with the DoD for each XRD pattern in (a) indicated.

In summary, a series of spinel structure chlorides Li2−2xMn1−xZrxCl4 (0 ⩽x⩽ 0.6) were synthesized successfully by mechanical ball milling and 350 °C annealing. The Li+ conductivities and electrochemical stabilities of Li2−2xMn1−xZrxCl4 were also investigated. After aliovalent substitution with Zr4+, the Li+ conductivities of the as-milled samples can be improved to the highest of 0.16 mS∙cm−1 with the lowest activation energy of 0.381 eV. The ASSLB with LMZC5 cathode active material exhibited excellent cycling stability for 200 cycles at room temperature. Through our study, we have demonstrated the potential possibility of using chlorides with good deformability and high oxidation potential as cathode materials for all-solid-state batteries, which is important to the development of all-solid-state batteries.

Acknowledgements

This work was supported by the National Natural Science Foundation of China (72293573, 72104226), the Research Topic of Securities Futures Industry Standard (BZKT-2022-041), and Anhui Province 2022 Annual New Era Education Quality Project (Postgraduate Education) (2022zyxwjxalk003).

Conflict of interest

The authors declare that they have no conflict of interest.

Based on the asset pricing role of media, this study used the event study to empirically examine the impact, as well as the heterogeneity from type and emotional tendency, of media attention on the market reaction to corporate violations from the perspective of limited attention.

The media’s prior attention to listed companies has a significant negative impact on the market reaction after corporate violations.

There is heterogeneity in media types and emotional effects of media coverage.

Feroz E H, Park K J, Pastena V. The financial and market effects of the SEC’s accounting and auditing enforcement releases. Journal of Accounting Research,1991, 29: 107. DOI: 10.2307/2491006

[2]

Huang Z, Wu G P. The market reaction and the impact on investors’ interest of the punishment of illegal disclosure. Journal of Northeast Normal University (Philosophy and Social Sciences),2013 (3): 66–71. (in Chinese) DOI: 10.16164/j.cnki.22-1062/c.2013.03.046

[3]

Tang T Z, Ma X, Song X Z. Financial restatement and financial market stability: Based on the perspective of stock price crash risk. Accounting Research,2021 (11): 31–43. (in Chinese) DOI: 10.3969/j.issn.1003-2886.2021.11.003

[4]

Zhang D N, Liu C L. Research on the impact of corporate social responsibility on stock market reactions to violation events. Chinese Journal of Management,2022, 19 (9): 1288–1296. (in Chinese) DOI: 10.3969/j.issn.1672-884x.2022.09.004

[5]

Jiang X L, Zhao Y L. Management power structure, violation and corporate value: The evidence from A-share listed companies. Journal of Shanxi Finance and Economics University,2017, 39 (5): 68–81. (in Chinese) DOI: 10.13781/j.cnki.1007-9556.2017.05.006

[6]

Zhu G D, Shen W T. A study on effectiveness of penalties of listed companies’ violation of regulations. Commercial Research,2011 (8): 101–106. DOI: 10.13902/j.cnki.syyj.2011.08.007

[7]

Ma D F, Qian B Y. Social trust, corporate violations and market reactions. Journal of Zhongnan University of Economics and Law,2016 (6): 77–84. (in Chinese)

[8]

Liu L H, Xu Y P, Rao P G, et al. The contagion effects of irregularities within business groups. Journal of Financial Research,2019 (6): 113–131. (in Chinese)

[9]

Zhu J. Media sentiment, government supervision strategy, and stock price fluctuation risk. Discrete Dynamics in Nature and Society, 2021,2021: 5532663. DOI: 10.1155/2021/5532663

[10]

Liu C, Wang S L, Li D. Hidden in a group? Market reactions to multi-violator corporate social irresponsibility disclosures. Strategic Management Journal,2021, 43 (1): 160–179. DOI: 10.1002/smj.3330

[11]

Kipp P C, Zhang Y, Tadesse A F. Can social media interaction and message features influence non-professional investors’ perceptions of firms. Journal of Information Systems,2019, 33 (2): 77–98. DOI: 10.2308/isys-52067

[12]

Wu D. Does social media get your attention. Journal of Behavioral Finance,2019, 20 (2): 213–226. DOI: 10.1080/15427560.2018.1505729

[13]

Liang C, Tang L, Li Y, et al. Which sentiment index is more informative to forecast stock market volatility? Evidence from China. International Review of Financial Analysis,2020, 71: 101552. DOI: 10.1016/j.irfa.2020.101552

[14]

Shen X. Trading and non-trading period Internet information flow and intraday return volatility. Physica A: Statistical Mechanics and Its Applications,2016, 451: 519–524. DOI: 10.1016/j.physa.2016.01.086

[15]

Zhang Y, Song W, Shen D, et al. Market reaction to Internet news: Information diffusion and price pressure. Economic Modeling,2016, 56: 43–49. DOI: 10.1016/j.econmod.2016.03.020

[16]

Da Z, Engelberg J, Gao P. The sum of all FEARS investor sentiment and asset prices. The Review of Financial Studies,2015, 28: 1–32. DOI: 10.1093/rfs/hhu072

[17]

Quan X F, Hong T, Wu S N. Selective attention, the ostrich effect and market anomalies. Journal of Financial Research,2012 (3): 109–123. (in Chinese)

[18]

Zhang S Q. Notice of clarification, media coverage and the stock price of listed company. The Theory and Practice of Finance and Economics,2018, 39 (1): 50–55. (in Chinese) DOI: 10.3969/j.issn.1003-7217.2018.01.008

[19]

Zhong H B, Zeng Y M. Can financial coverage convince the market? Based on the empirical research of market rumors in China. Journal of Fujian Normal University (Philosophy and Social Sciences Edition),2019 (06): 87–98, 170. (in Chinese) DOI: 10.12046/j.issn.1000-5285.2019.06.010

[20]

Xu X D, Zeng S X, Zou H L, et al. The impact of corporate environmental violation on shareholders’ wealth: A media coverage perspective. Business Strategy and the Environment,2016, 25 (2): 73–91. DOI: 10.1002/bse.1858

[21]

Fang L, Peress J. Media coverage and the cross-section of stock returns. Journal of Finance,2009, 64 (5): 2023–2052. DOI: 10.1111/j.1540-6261.2009.01493.x

[22]

Dougal C, Engelberg J, Garcia D, et al. Journalists and the stock market. Review of Financial Studies,2012, 25 (3): 639–679. DOI: 10.1093/rfs/hhr133

[23]

Guan Y J, Zhang J, Liu Y. Media attention, investor sentiment and stock market volatility. Statistics & Decision,2022, 38 (24): 143–148. (in Chinese) DOI: 10.13546/j.cnki.tjyjc.2022.24.028

[24]

Mitchell M L, Mulherin J H. The impact of public information on the stock market. The Journal of Finance,1994, 49 (3): 923–950. DOI: 10.1111/j.1540-6261.1994.tb00083.x

[25]

Chan W S. Stock price reaction to news and no-news: Drift and reversal after headlines. Journal of Financial Economics,2003, 70 (2): 223–260. DOI: 10.1016/s0304-405x(03)00146-6

[26]

Tetlock P C. Giving content to investor sentiment: The role of media in the stock market. The Journal of Finance,2007, 62 (3): 1139–1168. DOI: 10.1111/j.1540-6261.2007.01232.x

[27]

Takeda F, Yamazaki H. Stock price reactions to public TV programs on listed Japanese companies. Economics Bulletin,2006, 13 (11): 1–7.

[28]

An Z, Chen C, Naiker V, et al. Does media coverage deter firms from withholding bad news? Evidence from stock price crash risk. Journal of Corporate Finance,2020, 64: 101664. DOI: 10.1016/j.jcorpfin.2020.101664

[29]

Kahneman D. Attention and Effort. Englewood Cliffs, USA: Prentice Hall, 1973.

[30]

Al-Nasseri A, Ali F M. What does investors’ online divergence of opinion tell us about stock returns and trading volume. Journal of Business Research,2018, 86: 166–178. DOI: 10.1016/j.jbusres.2018.01.006

[31]

Barber B M, Odean T. All that glitters: The effect of attention and news on the buying behavior of individual and institutional investors. Review of Financial Studies,2008, 21 (2): 785–818. DOI: 10.1093/rfs/hhm079

[32]

Jia X C, Zhao Y, Meng S, et al. Limited attention of investors and the liquidation of non-tradable shares. Journal of Financial Research,2010 (11): 108–122. (in Chinese)

[33]

Jacob B, Ronen F, Shimon K. Information, trading, and volatility: Evidence from firm-specific news. Review of Financial Studies,2019, 32 (3): 992–1033. DOI: 10.1093/rfs/hhy083

[34]

Liu J L, Huang C Y, Dan L, et al. Opinion leadership, limited attention and overreaction. Economic Research Journal,2018 (3): 126–141. (in Chinese)

[35]

Lu Q Y, Chen H. Media coverage, investor sentiment and stock price volatility. Research on Financial and Economic Issues,2021 (3): 60–67. (in Chinese) DOI: 10.19654/j.cnki.cjwtyj.2021.03.007

[36]

Lv H K, Liu Z H, Qian Y X, et al. Relationship between financial news and stock market fluctuations. Data Analysis and Knowledge Discovery,2021, 5 (1): 99–111. (in Chinese) DOI: 10.11925/infotech.2096-3467.2020.0063

[37]

Renault T. Intraday online investor sentiment and return patterns in the U.S. stock market. Journal of Banking & Finance,2017, 84: 25–40. DOI: 10.1016/j.jbankfin.2017.07.002

[38]

Tausch F, Zumbuehl M. Stability of risk attitudes and media coverage of economic news. Journal of Economic Behavior & Organization,2018, 150 (6): 295–310. DOI: 10.1016/j.jebo.2018.01.013

[39]

Zhong H B, Shen Y Q, Zhang Y M. The influence of news discourse and stock price based on the perspective of financial media types. Journal of Beijing Institute of Technology (Social Sciences Edition),2018, 20 (3): 98–104. (in Chinese) DOI: 10.15918/j.jbitss1009-3370.2018.2834

[40]

Li P G, Shen Y F. The role of media in corporate governance: Empirical evidence from China. Economic Research Journal,2010, 45 (4): 14–27. (in Chinese)

[41]

Rodriguez F, Garza S. Predicting emotional intensity in social networks. Journal of Intelligent & Fuzzy Systems: Applications in Engineering and Technology,2019, 36 (5): 4709–4719. DOI: 10.3233/jifs-179020

[42]

Zhang L. Public information disclosure, media report tone and stock price behavior: A news report perspective based on equity change information. Friends of Accounting,2017 (4): 96–99. (in Chinese) DOI: 10.3969/j.issn.1004-5937.2017.04.021

[43]

Zhang T J, Sun Q. Over-optimistic sentiment of Internet media and stock price crash risk. Modernization of Management,2022, 42 (1): 34–39. (in Chinese) DOI: 10.19634/j.cnki.11-1403/c.2022.01.006

[44]

Li H. The impact of investor expectations on stock prices. The Journal of World Economy,2001 (6): 19–22. (in Chinese)

[45]

Dai Y Y, Yue P, Liu S C. Media supervision, government intervention and corporate governance: Evidence from the perspective of financial restatement of Chinese listed companies. The Journal of World Economy,2011 (11): 121–144. (in Chinese)

[46]

Shiller R J. Measuring bubble expectations and investor confidence. The Journal of Psychology and Financial Markets,2000, 1 (1): 49–60. DOI: 10.1207/s15327760jpfm0101_05

[47]

Merton R C. A simple model of capital market equilibrium with incomplete information. The Journal of Finance,1987, 42 (3): 483–510. DOI: 10.1111/j.1540-6261.1987.tb04565.x

[48]

Quan X F, Yin H Y, Wu H J. Analysis of asymmetric effects of media coverage on IPO stock price evidence from Chinese growth enterprise market. Accounting Research,2015 (6): 56–63. (in Chinese) DOI: 10.3969/j.issn.1003-2886.2015.06.008

[49]

Wang J X, Rao Y L, Peng D F. What drives the stock market “media coverage effect” expected media attention or unexpected media attention. Systems Engineering — Theory & Practice,2015, 35 (1): 37–48. (in Chinese) DOI: 10.12011/1000-6788(2015)1-37

[50]

Liu F, Ye Q, Li Y J. Impacts of interactions between news attention and investor attention on stock returns: Empirical investigation on financial shares in China. Journal of Management Sciences in China,2014, 17 (1): 72–85. (in Chinese) DOI: 10.3969/j.issn.1007-9807.2014.01.007

[51]

Wu Y. Momentum trading, mean reversal and overreaction in Chinese stock market. Review of Quantitative Finance& Accounting,2011, 37 (3): 301–323. DOI: 10.1007/s11156-010-0206-z

[52]

Mullainathan S. A memory-based model of bounded rationality. Quarterly Journal of Economics,2002, 117 (3): 735–774. DOI: 10.1162/003355302760193887

[53]

Coombs W T. Protecting organization reputations during a crisis: The development and application of situational crisis communication theory. Corporate Reputation Review,2007, 10 (3): 163–176. DOI: 10.1057/palgrave.crr.1550049

[54]

Wang X N, Zhou L Y. The mechanism of new media influence on haze risk perception. Journal of Beijing Institute of Technology (Social Sciences Edition),2020, 22 (2): 41–49. DOI: 10.15918/j.jbitss1009-3370.2020.3290

[55]

Yang Y, Zhao Y L. Media type, media attention and listed companies’ violations: A study based on propensity score matching method. Modern Economic Research,2017 (12): 60–69. DOI: 10.13891/j.cnki.mer.2017.12.008

[56]

Lu D, Fu P, Yang D. Media type, media coverage and internal control quality of listed firms. Accounting Research,2015 (4): 78–85. (in Chinese) DOI: 10.3969/j.issn.1003-2886.2015.04.011

[57]

Shen Y F, Yang J, Li G P. The corporate governance role of Internet public opinion: Evidences from private placement. Nankai Business Review,2013, 16 (3): 80–88. (in Chinese) DOI: 10.3969/j.issn.1008-3448.2013.03.009

[58]

Lou J H, Cai D. Can media coverage increase the information content of stock prices? Review of Investment Studies,2013, 32 (5): 38–53. (in Chinese)

[59]

Yin H Y, Sun M. Financial restatement, media attention and stock idiosyncratic risk volatility of listed companies. Finance and Trade Research,2022, 33 (5): 96–110. (in Chinese) DOI: 10.19337/j.cnki.34-1093/f.2022.05.008

[60]

Muller A, Kräuss R. Doing good deeds in times of need: A strategic perspective on corporate disaster donations. Strategic Management Journal,2011, 32 (4): 911–929. DOI: 10.1002/smj.917

[61]

Wei J C, Ouyang Z, Chen H. Well known or well liked? The effects of corporate reputation on firm value at the onset of a corporate crisis. Strategic Management Journal,2017, 38 (10): 2103–2120. DOI: 10.1002/smj.2639

[62]

Kim J B, Yu Z, Hao Z. Can media exposure improve stock price efficiency in China and why? Chinese Accounting Journal,2016, 9 (2): 83–114. DOI: 10.1016/j.cjar.2015.08.001

[63]

Dyck A, Volchkova N, Zingales L. The corporate governance role of the media: Evidence from Russia. The Journal of Finance,2008, 63 (3): 1093–1135. DOI: 10.1111/j.1540-6261.2008.01353.x

[64]

Wu P, Lu S, Yang N. The corporate governance role of media: Evidence from financial fraud. Journal of Central University of Finance & Economics,2019 (3): 51–69. (in Chinese) DOI: 10.19681/j.cnki.jcufe.2019.03.005

[65]

Liang Y J, Han R F, Liang Z L. Green technology innovation, media attention and enterprise value. Friends of Accounting,2023 (6): 112–119. (in Chinese) DOI: 10.3969/j.issn.1004-5937.2023.06.014

Spencer, M.A., Yun, T.G., Flynn, M. et al. Crystallographic Dimensionality Determines the Electrochemical Reaction Mechanism in Alkali Transition-Metal Chlorides. Journal of the American Chemical Society, 2024, 146(46): 32059-32071.

DOI:10.1021/jacs.4c13005

Figure

2.

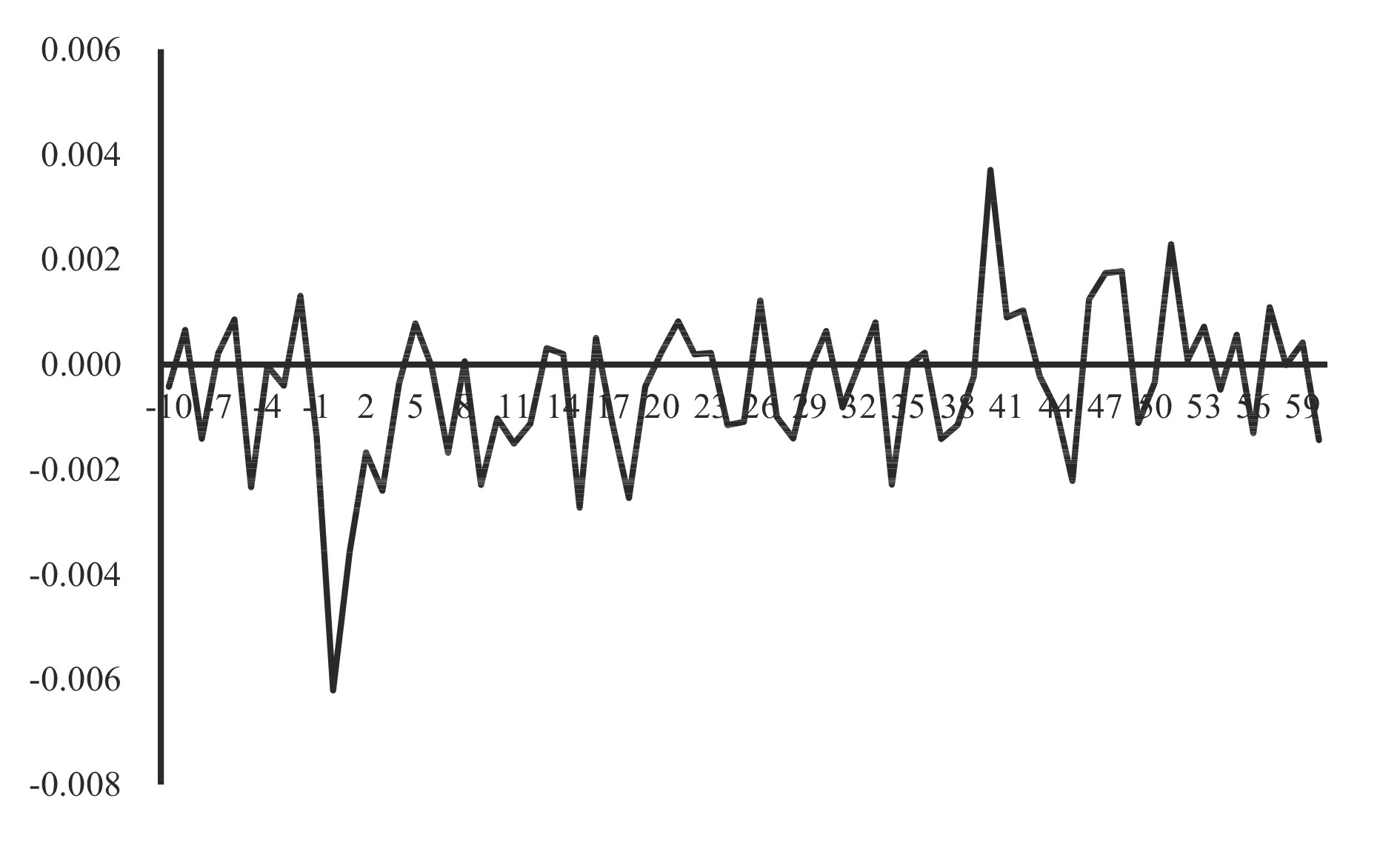

Abnormal return rate after corporate violation.

References

[1]

Feroz E H, Park K J, Pastena V. The financial and market effects of the SEC’s accounting and auditing enforcement releases. Journal of Accounting Research,1991, 29: 107. DOI: 10.2307/2491006

[2]

Huang Z, Wu G P. The market reaction and the impact on investors’ interest of the punishment of illegal disclosure. Journal of Northeast Normal University (Philosophy and Social Sciences),2013 (3): 66–71. (in Chinese) DOI: 10.16164/j.cnki.22-1062/c.2013.03.046

[3]

Tang T Z, Ma X, Song X Z. Financial restatement and financial market stability: Based on the perspective of stock price crash risk. Accounting Research,2021 (11): 31–43. (in Chinese) DOI: 10.3969/j.issn.1003-2886.2021.11.003

[4]

Zhang D N, Liu C L. Research on the impact of corporate social responsibility on stock market reactions to violation events. Chinese Journal of Management,2022, 19 (9): 1288–1296. (in Chinese) DOI: 10.3969/j.issn.1672-884x.2022.09.004

[5]

Jiang X L, Zhao Y L. Management power structure, violation and corporate value: The evidence from A-share listed companies. Journal of Shanxi Finance and Economics University,2017, 39 (5): 68–81. (in Chinese) DOI: 10.13781/j.cnki.1007-9556.2017.05.006

[6]

Zhu G D, Shen W T. A study on effectiveness of penalties of listed companies’ violation of regulations. Commercial Research,2011 (8): 101–106. DOI: 10.13902/j.cnki.syyj.2011.08.007

[7]

Ma D F, Qian B Y. Social trust, corporate violations and market reactions. Journal of Zhongnan University of Economics and Law,2016 (6): 77–84. (in Chinese)

[8]

Liu L H, Xu Y P, Rao P G, et al. The contagion effects of irregularities within business groups. Journal of Financial Research,2019 (6): 113–131. (in Chinese)

[9]

Zhu J. Media sentiment, government supervision strategy, and stock price fluctuation risk. Discrete Dynamics in Nature and Society, 2021,2021: 5532663. DOI: 10.1155/2021/5532663

[10]

Liu C, Wang S L, Li D. Hidden in a group? Market reactions to multi-violator corporate social irresponsibility disclosures. Strategic Management Journal,2021, 43 (1): 160–179. DOI: 10.1002/smj.3330

[11]

Kipp P C, Zhang Y, Tadesse A F. Can social media interaction and message features influence non-professional investors’ perceptions of firms. Journal of Information Systems,2019, 33 (2): 77–98. DOI: 10.2308/isys-52067

[12]

Wu D. Does social media get your attention. Journal of Behavioral Finance,2019, 20 (2): 213–226. DOI: 10.1080/15427560.2018.1505729

[13]

Liang C, Tang L, Li Y, et al. Which sentiment index is more informative to forecast stock market volatility? Evidence from China. International Review of Financial Analysis,2020, 71: 101552. DOI: 10.1016/j.irfa.2020.101552

[14]

Shen X. Trading and non-trading period Internet information flow and intraday return volatility. Physica A: Statistical Mechanics and Its Applications,2016, 451: 519–524. DOI: 10.1016/j.physa.2016.01.086

[15]

Zhang Y, Song W, Shen D, et al. Market reaction to Internet news: Information diffusion and price pressure. Economic Modeling,2016, 56: 43–49. DOI: 10.1016/j.econmod.2016.03.020

[16]

Da Z, Engelberg J, Gao P. The sum of all FEARS investor sentiment and asset prices. The Review of Financial Studies,2015, 28: 1–32. DOI: 10.1093/rfs/hhu072

[17]

Quan X F, Hong T, Wu S N. Selective attention, the ostrich effect and market anomalies. Journal of Financial Research,2012 (3): 109–123. (in Chinese)

[18]

Zhang S Q. Notice of clarification, media coverage and the stock price of listed company. The Theory and Practice of Finance and Economics,2018, 39 (1): 50–55. (in Chinese) DOI: 10.3969/j.issn.1003-7217.2018.01.008

[19]

Zhong H B, Zeng Y M. Can financial coverage convince the market? Based on the empirical research of market rumors in China. Journal of Fujian Normal University (Philosophy and Social Sciences Edition),2019 (06): 87–98, 170. (in Chinese) DOI: 10.12046/j.issn.1000-5285.2019.06.010

[20]

Xu X D, Zeng S X, Zou H L, et al. The impact of corporate environmental violation on shareholders’ wealth: A media coverage perspective. Business Strategy and the Environment,2016, 25 (2): 73–91. DOI: 10.1002/bse.1858

[21]

Fang L, Peress J. Media coverage and the cross-section of stock returns. Journal of Finance,2009, 64 (5): 2023–2052. DOI: 10.1111/j.1540-6261.2009.01493.x

[22]

Dougal C, Engelberg J, Garcia D, et al. Journalists and the stock market. Review of Financial Studies,2012, 25 (3): 639–679. DOI: 10.1093/rfs/hhr133

[23]

Guan Y J, Zhang J, Liu Y. Media attention, investor sentiment and stock market volatility. Statistics & Decision,2022, 38 (24): 143–148. (in Chinese) DOI: 10.13546/j.cnki.tjyjc.2022.24.028

[24]

Mitchell M L, Mulherin J H. The impact of public information on the stock market. The Journal of Finance,1994, 49 (3): 923–950. DOI: 10.1111/j.1540-6261.1994.tb00083.x

[25]

Chan W S. Stock price reaction to news and no-news: Drift and reversal after headlines. Journal of Financial Economics,2003, 70 (2): 223–260. DOI: 10.1016/s0304-405x(03)00146-6

[26]

Tetlock P C. Giving content to investor sentiment: The role of media in the stock market. The Journal of Finance,2007, 62 (3): 1139–1168. DOI: 10.1111/j.1540-6261.2007.01232.x

[27]

Takeda F, Yamazaki H. Stock price reactions to public TV programs on listed Japanese companies. Economics Bulletin,2006, 13 (11): 1–7.

[28]

An Z, Chen C, Naiker V, et al. Does media coverage deter firms from withholding bad news? Evidence from stock price crash risk. Journal of Corporate Finance,2020, 64: 101664. DOI: 10.1016/j.jcorpfin.2020.101664

[29]

Kahneman D. Attention and Effort. Englewood Cliffs, USA: Prentice Hall, 1973.

[30]

Al-Nasseri A, Ali F M. What does investors’ online divergence of opinion tell us about stock returns and trading volume. Journal of Business Research,2018, 86: 166–178. DOI: 10.1016/j.jbusres.2018.01.006

[31]

Barber B M, Odean T. All that glitters: The effect of attention and news on the buying behavior of individual and institutional investors. Review of Financial Studies,2008, 21 (2): 785–818. DOI: 10.1093/rfs/hhm079

[32]

Jia X C, Zhao Y, Meng S, et al. Limited attention of investors and the liquidation of non-tradable shares. Journal of Financial Research,2010 (11): 108–122. (in Chinese)

[33]

Jacob B, Ronen F, Shimon K. Information, trading, and volatility: Evidence from firm-specific news. Review of Financial Studies,2019, 32 (3): 992–1033. DOI: 10.1093/rfs/hhy083

[34]

Liu J L, Huang C Y, Dan L, et al. Opinion leadership, limited attention and overreaction. Economic Research Journal,2018 (3): 126–141. (in Chinese)

[35]

Lu Q Y, Chen H. Media coverage, investor sentiment and stock price volatility. Research on Financial and Economic Issues,2021 (3): 60–67. (in Chinese) DOI: 10.19654/j.cnki.cjwtyj.2021.03.007

[36]

Lv H K, Liu Z H, Qian Y X, et al. Relationship between financial news and stock market fluctuations. Data Analysis and Knowledge Discovery,2021, 5 (1): 99–111. (in Chinese) DOI: 10.11925/infotech.2096-3467.2020.0063

[37]

Renault T. Intraday online investor sentiment and return patterns in the U.S. stock market. Journal of Banking & Finance,2017, 84: 25–40. DOI: 10.1016/j.jbankfin.2017.07.002

[38]

Tausch F, Zumbuehl M. Stability of risk attitudes and media coverage of economic news. Journal of Economic Behavior & Organization,2018, 150 (6): 295–310. DOI: 10.1016/j.jebo.2018.01.013

[39]

Zhong H B, Shen Y Q, Zhang Y M. The influence of news discourse and stock price based on the perspective of financial media types. Journal of Beijing Institute of Technology (Social Sciences Edition),2018, 20 (3): 98–104. (in Chinese) DOI: 10.15918/j.jbitss1009-3370.2018.2834

[40]

Li P G, Shen Y F. The role of media in corporate governance: Empirical evidence from China. Economic Research Journal,2010, 45 (4): 14–27. (in Chinese)

[41]

Rodriguez F, Garza S. Predicting emotional intensity in social networks. Journal of Intelligent & Fuzzy Systems: Applications in Engineering and Technology,2019, 36 (5): 4709–4719. DOI: 10.3233/jifs-179020

[42]

Zhang L. Public information disclosure, media report tone and stock price behavior: A news report perspective based on equity change information. Friends of Accounting,2017 (4): 96–99. (in Chinese) DOI: 10.3969/j.issn.1004-5937.2017.04.021

[43]

Zhang T J, Sun Q. Over-optimistic sentiment of Internet media and stock price crash risk. Modernization of Management,2022, 42 (1): 34–39. (in Chinese) DOI: 10.19634/j.cnki.11-1403/c.2022.01.006

[44]

Li H. The impact of investor expectations on stock prices. The Journal of World Economy,2001 (6): 19–22. (in Chinese)

[45]

Dai Y Y, Yue P, Liu S C. Media supervision, government intervention and corporate governance: Evidence from the perspective of financial restatement of Chinese listed companies. The Journal of World Economy,2011 (11): 121–144. (in Chinese)

[46]

Shiller R J. Measuring bubble expectations and investor confidence. The Journal of Psychology and Financial Markets,2000, 1 (1): 49–60. DOI: 10.1207/s15327760jpfm0101_05

[47]

Merton R C. A simple model of capital market equilibrium with incomplete information. The Journal of Finance,1987, 42 (3): 483–510. DOI: 10.1111/j.1540-6261.1987.tb04565.x

[48]

Quan X F, Yin H Y, Wu H J. Analysis of asymmetric effects of media coverage on IPO stock price evidence from Chinese growth enterprise market. Accounting Research,2015 (6): 56–63. (in Chinese) DOI: 10.3969/j.issn.1003-2886.2015.06.008

[49]

Wang J X, Rao Y L, Peng D F. What drives the stock market “media coverage effect” expected media attention or unexpected media attention. Systems Engineering — Theory & Practice,2015, 35 (1): 37–48. (in Chinese) DOI: 10.12011/1000-6788(2015)1-37

[50]

Liu F, Ye Q, Li Y J. Impacts of interactions between news attention and investor attention on stock returns: Empirical investigation on financial shares in China. Journal of Management Sciences in China,2014, 17 (1): 72–85. (in Chinese) DOI: 10.3969/j.issn.1007-9807.2014.01.007

[51]

Wu Y. Momentum trading, mean reversal and overreaction in Chinese stock market. Review of Quantitative Finance& Accounting,2011, 37 (3): 301–323. DOI: 10.1007/s11156-010-0206-z

[52]

Mullainathan S. A memory-based model of bounded rationality. Quarterly Journal of Economics,2002, 117 (3): 735–774. DOI: 10.1162/003355302760193887

[53]

Coombs W T. Protecting organization reputations during a crisis: The development and application of situational crisis communication theory. Corporate Reputation Review,2007, 10 (3): 163–176. DOI: 10.1057/palgrave.crr.1550049

[54]

Wang X N, Zhou L Y. The mechanism of new media influence on haze risk perception. Journal of Beijing Institute of Technology (Social Sciences Edition),2020, 22 (2): 41–49. DOI: 10.15918/j.jbitss1009-3370.2020.3290

[55]

Yang Y, Zhao Y L. Media type, media attention and listed companies’ violations: A study based on propensity score matching method. Modern Economic Research,2017 (12): 60–69. DOI: 10.13891/j.cnki.mer.2017.12.008

[56]

Lu D, Fu P, Yang D. Media type, media coverage and internal control quality of listed firms. Accounting Research,2015 (4): 78–85. (in Chinese) DOI: 10.3969/j.issn.1003-2886.2015.04.011

[57]

Shen Y F, Yang J, Li G P. The corporate governance role of Internet public opinion: Evidences from private placement. Nankai Business Review,2013, 16 (3): 80–88. (in Chinese) DOI: 10.3969/j.issn.1008-3448.2013.03.009

[58]

Lou J H, Cai D. Can media coverage increase the information content of stock prices? Review of Investment Studies,2013, 32 (5): 38–53. (in Chinese)

[59]

Yin H Y, Sun M. Financial restatement, media attention and stock idiosyncratic risk volatility of listed companies. Finance and Trade Research,2022, 33 (5): 96–110. (in Chinese) DOI: 10.19337/j.cnki.34-1093/f.2022.05.008

[60]

Muller A, Kräuss R. Doing good deeds in times of need: A strategic perspective on corporate disaster donations. Strategic Management Journal,2011, 32 (4): 911–929. DOI: 10.1002/smj.917

[61]

Wei J C, Ouyang Z, Chen H. Well known or well liked? The effects of corporate reputation on firm value at the onset of a corporate crisis. Strategic Management Journal,2017, 38 (10): 2103–2120. DOI: 10.1002/smj.2639

[62]

Kim J B, Yu Z, Hao Z. Can media exposure improve stock price efficiency in China and why? Chinese Accounting Journal,2016, 9 (2): 83–114. DOI: 10.1016/j.cjar.2015.08.001

[63]

Dyck A, Volchkova N, Zingales L. The corporate governance role of the media: Evidence from Russia. The Journal of Finance,2008, 63 (3): 1093–1135. DOI: 10.1111/j.1540-6261.2008.01353.x

[64]

Wu P, Lu S, Yang N. The corporate governance role of media: Evidence from financial fraud. Journal of Central University of Finance & Economics,2019 (3): 51–69. (in Chinese) DOI: 10.19681/j.cnki.jcufe.2019.03.005

[65]

Liang Y J, Han R F, Liang Z L. Green technology innovation, media attention and enterprise value. Friends of Accounting,2023 (6): 112–119. (in Chinese) DOI: 10.3969/j.issn.1004-5937.2023.06.014

Spencer, M.A., Yun, T.G., Flynn, M. et al. Crystallographic Dimensionality Determines the Electrochemical Reaction Mechanism in Alkali Transition-Metal Chlorides. Journal of the American Chemical Society, 2024, 146(46): 32059-32071.

DOI:10.1021/jacs.4c13005

DownLoad:

DownLoad: