Tiantian Mao is an Associate Professor with the University of Science and Technology of China (USTC). In 2012, she received her Ph.D. degree in Science from USTC. In May of the same year, she joined the Department of Statistics and Finance, School of Management, USTC, for postdoctoral work. Her research fields include risk measurement, risk management, random dominance and extreme value theory

Qinyu Wu is currently a Ph.D. candidate at the School of Management, University of Science and Technology of China. His research interests focus on risk management and mathematical finance

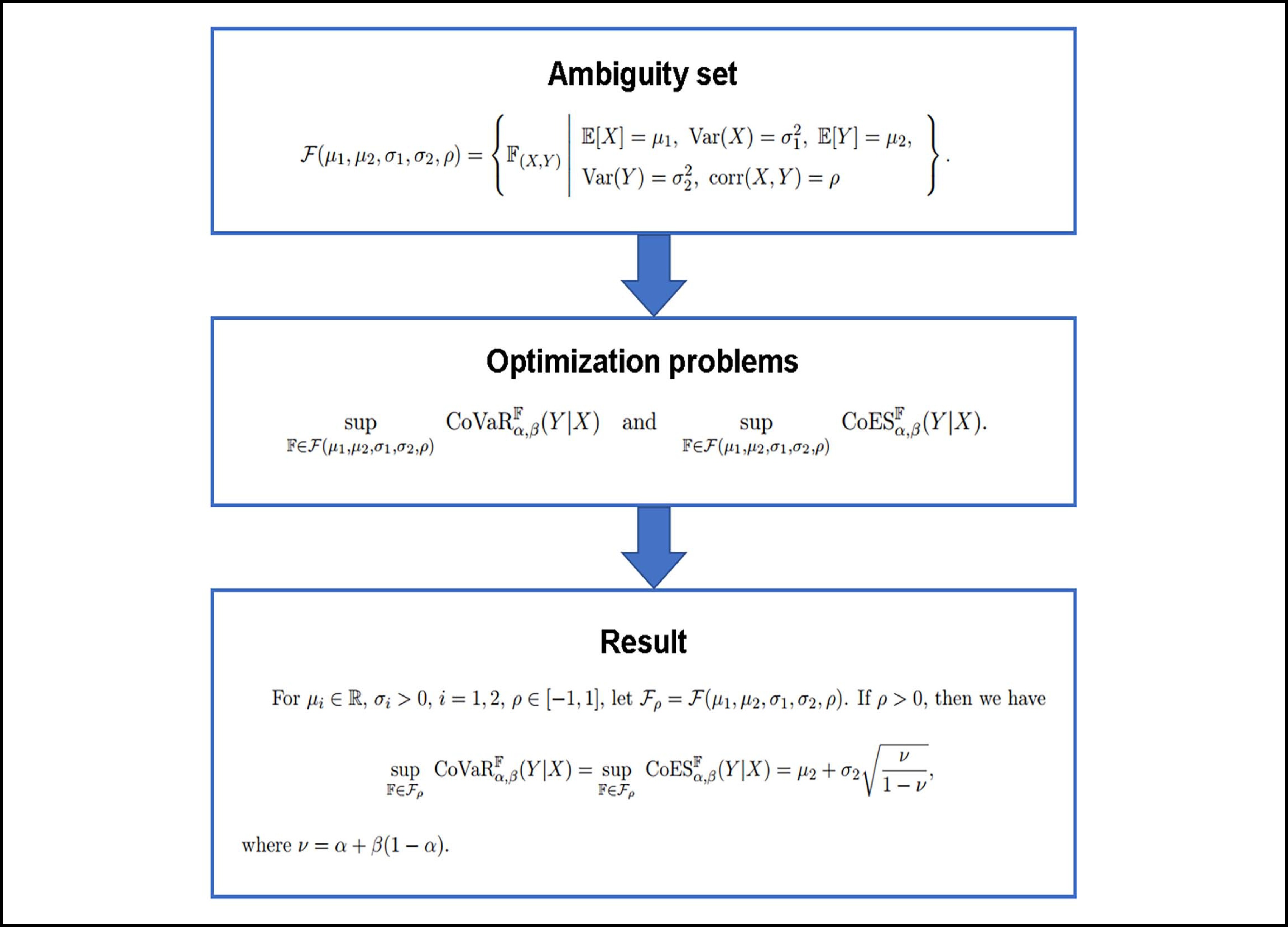

In this paper, we study the worst-case conditional value-at-risk (CoVaR) and conditional expected shortfall (CoES) in a situation where only partial information on the underlying probability distribution is available. In the case of the first two marginal moments are known, the closed-form solution and the value of the worst-case CoVaR and CoES are derived. The worst-case CoVaR and CoES under mean and covariance information are also investigated.

Graphical Abstract

We construct the above new ambiguity set, then propose the optimization problem of CoVaRand CoES based on this ambiguity set, and give the theoretical results.

Abstract

In this paper, we study the worst-case conditional value-at-risk (CoVaR) and conditional expected shortfall (CoES) in a situation where only partial information on the underlying probability distribution is available. In the case of the first two marginal moments are known, the closed-form solution and the value of the worst-case CoVaR and CoES are derived. The worst-case CoVaR and CoES under mean and covariance information are also investigated.

Public Summary

The relationship between CoVaR, CoES and dependence structure are investigated.

In case where the first two marginal moments are known, the closed-form solution and the valueof the worst-case CoVaR and CoES are derived.

The worst-case CoVaR and CoES under mean and covariance information are investigated.

Modern risk management often requires the evaluation of risks under multiple scenarios. For instance, in the fundamental review of the trading book of Basel Ⅳ[1], banks need to evaluate the risk of their portfolios under stressed scenarios including the model generated from data during the 2007 financial crisis. In the aftermath of the financial crisis, there has been growing interest in measuring systemic risk, which refers to the risk that an event at the company level could trigger severe instability or collapse an entire industry or economy. Capital requirements are closely linked to an institution’s contribution to the overall risk of the financial system and not merely to its individual risk.

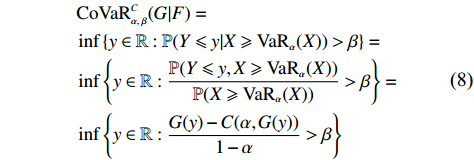

Measuring the contribution of each institution to the overall systemic risk can help regulators inhibit the tendency to generate systemic risk by identifying institutions that make significant contributions to systemic risk. Starting with the seminal paper of Adrian and Brunnermeier[2] (first published online in 2008), many methods have been proposed for measuring systemic risk[3, 4]. While the conditional value-at-risk (CoVaR) proposed by Ref. [2] described the VaR of the financial system conditional on an institution being in financial distress, Girardi and Ergün[5] modified the computation of CoVaR in Ref. [2] by changing the definition of financial distress from the loss of an institution being exactly its VaR to being no less than its VaR. Specifically, for a set of financial institutions (or portfolio) X=(X1,⋯,Xn), we denote by S=X1+⋯+Xn as the total systemic risk. The value-at-risk (VaR) of an institution Xi at level α is defined as the α-quantile function of Xi, that is, VaRα(Xi)=inf{x∈R:P(Xi⩽. The notation {\rm{ CoVaR}}_{\alpha, \beta}(S\vert X_i) is defined as the VaR of the systemic risk S at level \beta , conditional on one of the institutions X_i beyond its VaR at level \alpha , that is,

We use the right-continuous version of {\rm{ CoVaR}} in this study, that is, > \beta instead of \geqslant \beta in Eq. (1). In the case of the right-continuous version, the worst-case value is reachable. Both definitions have the same worst-case value, which has no effect on our study. Huang and Uryasev[6] linked the systemic risk contribution of an institution to the increase in the CoVaR of the entire financial system while the institution is under distress. Acharya et al.[4] proposed the marginal expected shortfall (ES) to measure the contributions of financial institutions to systemic risk, whose mathematical expression has been generalized to the following conditional expected shortfall (CoES)[2], at level \beta , conditional on one of the institutions X_i beyond its VaR at level \alpha ,

Notably, CoVaR and CoES, defined by Eqs. (1) and (2), and their transformers have played an essential role in measuring the system risk. Detailed discussions and their applications in economics, finance, and other fields can be found in Refs. [2, 5, 7, 8], as well as the references therein.

Measuring systemic risk requires the knowledge of its probability distribution. In most practices, the exact form of the distribution is often lacking, and only sample data are available for estimating the distribution, which is inevitably prone to sampling error. This situation, wherein the probability distribution of uncertain outcomes cannot be uniquely identified, is referred to as distributional uncertainty. The question of how to account for distributional uncertainty in decision-making has been of central interest in several fields, including economics, finance, control system, and operations research/ management science. One modeling paradigm that has been successfully adopted in all these fields to address this issue is distributionally robust optimization (DRO). In the standard form of DRO, we characterize one’s (partial) information by specifying an uncertainty set {\cal{ F}} , which is also known as an ambiguity set, instead of an underlying probability distribution that is known exactly. Various types of uncertainty sets {\cal{ F}} have been proposed in the literature. One common way of defining the set {\cal{ F}} is by specifying the moments of the distribution. The earlier works of Popescu[9], Bertsimas et al.[10], Delage and Ye[11], and Natarajan et al.[12] have considered the case where the uncertainty set is specified in terms of the first two moments. More recently, Wiesemann et al.[13] considered a case in which the uncertainty set was described through supports and higher-order moments. In this study, we consider the worst-case CoVaR and CoES under moment uncertainty. Specifically, we consider the following optimization problems:

where \mathcal F is an uncertainty set specifying the mean vector and the covariance of X , and {\rm{ CoVaR}}^\mathbb F and {\rm{ CoES}}^\mathbb F represent the calculation for {\rm{ CoVaR}}(S|X_i) and {\rm{ CoES}}(S|X_i) under the joint distribution \mathbb F , respectively. While the current stduy focuses on moment-based uncertainty sets, we should point out here that the uncertainty set can also be defined according to a certain distance over distributions, such as KL divergence and Wasserstein metric.

2

Preliminaries

Let (\mathit \Omega,\mathcal B, \mathbb{P}) be an atomless probability space, and (\mathit \Omega,\mathcal B, \mathbb{P})^n as its n-dimensional product space, where \mathit \Omega is a set of possible states of nature and \mathcal B is a σ-algebra on \mathit \Omega. The random variable is a measurable real-valued functional on (\mathit \Omega,\mathcal B, \mathbb{P}). For a random vector (random variable) {X} = (X_1, \dots,X_n), its distribution function is defined by \mathbb F(x_1, \dots,x_n) = \mathbb{P}(X_1 \leqslant x_1, \dots, X_n \leqslant x_n) for (x_1, \dots,x_n)\in \mathbb{R}^n , and we denote the distribution function of the random vector (random variable) X by \mathbb F_{X}. The notation \delta_x represents the point mass at x\in \mathbb{R}^n . The left and right quantile function of a univariate distribution F are denoted by F^{-1} and F^{-1+} , respectively. For a mapping f:(\mathit \Omega,\mathcal B, \mathbb{P})^n\to \mathbb{R}, the notation f^\mathbb F(X) indicates that it has the same value as f(X), where X is a random vector (random variable) in (\varOmega,\mathcal B, \mathbb{P})^n and \mathbb F is its distribution. In this study, both notation, f^\mathbb F(X) and f(X), are used. For a random variable X , we denote the mean and the variance of X by \mathbb{E}[X] and {\rm{ Var}}(X) , respectively, and for a random vector X, we denote the mean vector and the covariance matrix by \mathbb{E}[{X}] and {\rm{ Cov}}({X}), respectively.

Notably, VaR and ES are two popular and important risk measures in financial practice. The left and right VaRs of a random variable X at level \alpha\in(0,1) are defined by \mathrm{VaR}_\alpha(X) = F_X^{-1}(\alpha) and \mathrm{VaR}_\alpha^+(X) = F_X^{-1+}(\alpha), respectively. The ES of a random variable X at level \alpha\in[0,1) is defined by \mathrm{ES}_{\alpha}(X) = {1}/({1-\alpha})\int_\alpha^1 {\rm{ VaR}}_{s}(X)\,\mathrm{d} s . Furthermore, CoVaR and CoES are defined by Eqs. (1) and (2) in the Introduction, respectively.

2.1

Worst-case systemic risk measures

In this study, we examine the worst-case CoVaR and CoES with an uncertainty set based on moment constraints. Specifically, for a portfolio {X} = (X_1,\cdots,X_n), let S = X_1+ \dots+X_n , and we consider the following optimization problems:

where \mu\in \mathbb{R}^n, \mathit \Sigma\in \mathbb{R}^{n\times n} is a given semi-positive matrix. Our aim is to investigate the optimization problems in (4).

The objective function of (4) only depends on X_i and S . The uncertainty constraint can be replaced by the following set:

where \mathbb F_{(X_i,\;S)} is the joint distribution function of (X_i,\;S). Applying the general projection property in Ref. [9] (see also Ref. [14, Lemma 2.4]), \mathcal F_{i,\;\mu,\; \mathit \Sigma} equals to the following uncertainty set:

where {\bf{1}} = (1, \dots,1)\in \mathbb{R}^n , and e_i = (0,\cdots,1,\cdots,0)\in \mathbb{R}^n is the vector whose ith element equals to 1 and the other elements are all zero. These arguments inspire us to consider the following general optimization problems:

where \mu\in \mathbb{R}^2, and \mathit \Sigma\in \mathbb{R}^{2\times 2} is a semi-positive matrix. It is easy to verify that the original optimization problems in (4) are a special case of optimization problems in (6) with \boldsymbol\mu = (\mu_i,{\sum\limits}_{i = 1}^n\mu_i) and \mathit \Sigma = (e_i,{\bf{1}})^\top \mathit \Sigma_n(e_i,{\bf{1}}), where \mathit\Sigma_n is the covariance of the random vector (X_1, \dots,X_n) .

In the remainder of this paper, we aim to solve the optimization problems in (6). We always assume that all considered random variables X in (6) satisfy that F_X is continuous at \mathrm{VaR}_\alpha(X) so that \mathbb{P}(X \leqslant \mathrm{VaR}_\alpha(X)) = 1- \mathbb{P}(X \geqslant \mathrm{VaR}_\alpha(X)) = \alpha . Some preliminaries on the copula theory are needed, and these will be introduced in the next subsection.

2.2

Copula

In this section, we recall the definition of two-dimensional copula that is a tool for separating dependence and marginal distributions. A two-dimensional copula is a function C:[0,1]^{2}\to[0,1] that satisfies

(i) for any u, v\in [0,1], C(u, 0) = 0 = C(0, v), C(u, 1) = u \text { and } C(1, v) = v;

(ii) for any u_{1}, u_{2}, v_{1}, v_{2}\in [0,1] such that u_{1} \leqslant u_{2} and v_{1} \leqslant v_{2} ,

For a two-dimensional random vector (X,Y) with joint distribution \mathbb F_{(X,Y)} , its copula is denoted by C . By Sklar’s theorem[15], the joint distribution can be expressed as

The above-stated formula illustrates that the value of {\rm{ CoVaR}}_{\alpha,\; \beta}^C(G\vert F) does not depend on the marginal distribution F . The following proposition, which collects the results of Ref. [16, Theorem 3.4] shows that C_1 \leqslant C_2 pointwisely implies {\rm{ CoVaR}}_{\alpha,\;\beta}^{C_1} \leqslant {\rm{ CoVaR}}_{\alpha,\;\beta}^{C_2} and \operatorname{CoES}_{\alpha,\;\beta}^{C_1} \leqslant\operatorname{CoES}_{\alpha,\;\beta}^{C_2} for all \alpha,\;\beta\in(0,1), and it is useful throughout the paper.

Proposition 2.1. Let \alpha,\;\beta\in(0,1), and let F_1 , F_2 and G be three univariate distributions. For any copula C , we have

Proof. By Eq. (8), we can immediately obtain {\rm{ CoVaR}}^{C}_{\alpha, \; \beta} (G\vert F_1) = {\rm{ CoVaR}}^{C}_{\alpha, \; \beta}(G\vert F_2). Because CoES is formulated as the integral of CoVaR, we have {\rm{ CoES}}^{C}_{\alpha,\; \beta}(G\vert F_1) = {\rm{ CoES}}^{C}_{\alpha,\; \beta}(G\vert F_2). To see the "Moreover" part, if C_1 \leqslant C_2 pointwisely, then we have C_1(\alpha,G(y)) \leqslant C_2(\alpha,G(y)) for all y\in \mathbb{R} . It follows from Eq. (8) that {\rm{ CoVaR}}^{C_1}_{\alpha, \; \beta}(G\vert F_1) \leqslant {\rm{ CoVaR}}^{C_2}_{\alpha, \; \beta}(G\vert F_2). Noting that CoES is formulated as the integral of CoVaR, we obtain {\rm{ CoES}}_{\alpha, \; \beta}^{C_1}(G \vert F) \leqslant {\rm{ CoES}}^{C_2}_{\alpha,\; \beta}(G \vert F). Hence, we complete the proof.

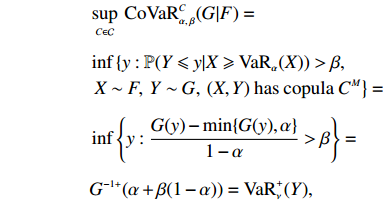

Since for any copula C , we have C(u,v) \leqslant C^M . The next proposition is a direct result followed by Proposition 2.1.

Proposition 2.2. Let C_0 be a copula function, and \mathcal C = \{C\vert C_0 \in \mathcal C, C \leqslant C_0 \}. Consider two optimization problems

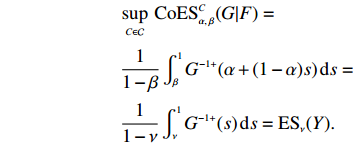

Both maximization problems can both be attained at C_0 . Specifically, if C^M\in\mathcal C , then the optimization problems (i) and (ii) can be attained at C^M , and the values of (i) and (ii) are \mathrm{VaR}_{\nu}^+(Y) and \mathrm{ES}_{\nu}(Y) , respectively, where \nu = \alpha+\beta(1-\alpha) and Y has distribution G .

Proof. The maximizer can be attained at C_0 , immediately following Proposition 2.1. If C^M\in\mathcal C , and C^M \geqslant C for all copulas C , the maximizer can be attained at C^M . Moreover, in this case, we obtain

Proposition 2.2 provides a natural idea to solve the optimization problem \sup_{\mathbb F\in \mathcal F}R^\mathbb F(Y\vert X) , where R = {\rm{ CoVaR}}_{\alpha,\;\beta} or {\rm{ CoES}}_{\alpha,\;\beta}, in two steps. First, fix the marginal distributions as F and G , and calculate R_{F,G} = \sup_{C\in\mathcal C_{F,\;G}} R^C(G|F) where \mathcal C_{F,G} = \{C: C (F,G)\in\mathcal F\}. Second, we calculate \sup_{F,\;G}R_{F,\;G}. If for all F,G , the set \mathcal C_{F,G} = \{C: C(F,G)\in\mathcal F\} contains a copula C_{F,G} such that C_{F,G} \geqslant C pointwisely for all C\in\mathcal C_{F,G} , then it follows from Proposition 2.2 that \sup_{\mathbb F\in \mathcal F}R^\mathbb F(Y\vert X) = \sup_{F,\;G}R^{C_{F,\;G}}(G\vert F).

3

Worst-case CoVaR and CoES under moment constraints

3.1

Marginal information

In this subsection, we consider the worst-case CoVaR and CoES in the case that the uncertainty set contains the information of the first two marginal moments, that is,

The following lemma, which plays an important role in the proof of the main theorems presented in this paper, is a direct result of Refs. [17, Theorem 1] and [14, Theorem 2.9].

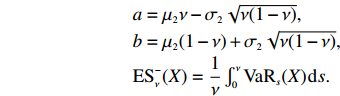

Lemma 3.1. For \mu\in \mathbb{R} , \sigma>0 and \alpha\in[0,1) , it holds that

where \nu = \alpha + \beta(1 -\alpha) , and the supremum can be attained at the joint distribution (x,y)\mapsto\min\{F(x),G(y)\}, where the mean and variance of F is \mu_1 and \sigma_1^2 , respectively, and G is a two-point distribution, defined as

G = \nu\delta_{\mu_2-\sigma_2\sqrt{\frac{1-\nu}{\nu}}} +(1-\nu)\delta_{\mu_2+\sigma_2\sqrt{\frac{\nu}{1-\nu}}}.

Proof. For any (X,Y) , it follows from Proposition 2.2 that

where the equalities in the two formulas given above follow from Lemma 3.1. On the other hand, one can verify that the worst-case value of CoVaR and CoES can be attained at the distribution given in the theorem. Thus, we have

Theorem 3.1 illustrates that the closed-form solution of (9) does not depend on the form of the distribution of X but requires a comonotonicity copula structure of (X,Y) . In other words, we can derive different forms of the closed-form solution by constructing different forms of the distribution of X . The following is a special case of the closed-form solution defined in Theorem 3.1.

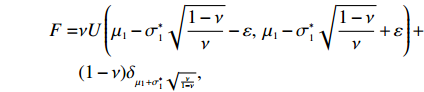

G = \nu\delta_{\mu_2-\sigma_2\sqrt{\frac{1-\nu}{\nu}}} +(1-\nu)\delta_{\mu_2+\sigma_2\sqrt{\frac{\nu}{1-\nu}}},

where \nu = \alpha+\beta(1-\alpha) , \varepsilon,\; \sigma_1^* \geqslant 0 satisfy {(\nu{ \varepsilon}^2)}/{3}+{\sigma^{*}_1}^2 = \sigma_1^2 , and U(a,b) represents a uniform distribution on [a,b] . It is easy to verify that the mean and variance of F are \mu_1 and \sigma_1^2 ; hence, \min\{F,G\} is a closed-form solution of (9). Moreover, suppose that \varepsilon^2 \leqslant {3\sigma_1^2}/({\nu(4-3\nu)}) . Then, we have

In particular, if \varepsilon = 0 , then F reduces to a two-point distribution. In this case, the correlation coefficient equals to 1.

3.2

Mean-covariance information

In this subsection, we consider the optimization problems in (6) when the uncertainty set \mathcal F contains the information of the mean vector and covariance with a fixed correlation coefficient, that is,

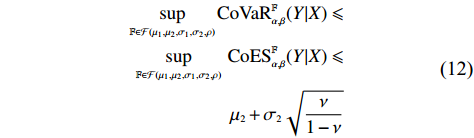

where \mu_i\in \mathbb{R} , \sigma_i>0 for i = 1,2 , \rho\in[-1,1] and {\rm{ corr}}(X,Y) represents the correlation coefficient of (X,Y) . It is noteworthy that \mathcal F(\mu_1,\mu_2,\sigma_1,\sigma_2,\rho)\subseteq \mathcal F(\mu_1,\mu_2,\sigma_1,\sigma_2) for all \rho\in[-1,1] , where \mathcal F(\mu_1,\mu_2,\sigma_1,\sigma_2) is defined by Eq. (10). By Theorem 3.1, we have

where \nu = \alpha+\beta(1-\alpha) . Recall Example 3.1, we know that the equalities of (12) hold if \rho \geqslant {3(1-\nu)}/({1+3(1-\nu)}) . A natural question is that what is the range of \rho that will make (12) become equalities? To answer this question, we first present the following lemma, which shows that the values of the worst-case CoVaR and CoES with the uncertainty set \mathcal F(\mu_1, \mu_2, \sigma_1,\sigma_2,\rho) increase in \rho .

Lemma 3.2. For \mu_i\in \mathbb{R} , \sigma_i>0 , i = 1,2 , \rho\in[-1,1] , let \mathcal F_\rho: = \mathcal F(\mu_1,\mu_2,\sigma_1,\sigma_2,\rho) defined by Eq. (11). Both \sup_{ \mathbb F\in \mathcal F_\rho} {\rm{ CoVaR}}_{\alpha, \beta}^\mathbb F(Y\vert X) and \sup_{\mathbb F\in \mathcal F_\rho} {\rm{ CoES}}_{\alpha, \beta}^\mathbb F(Y\vert X) increase in \rho.

Proof. We only give the proof of the case of CoVaR, as the case of CoES can be proved similarly. Let -1 \leqslant\rho_1<\rho_2 \leqslant 1 , and denote by \theta = \sup_{\mathbb F\in \mathcal F_{\rho_1}} {\rm{ CoVaR}}_{\alpha, \beta}^\mathbb F(Y\vert X). We demonstrate that \sup_{\mathbb F\in \mathcal F_{\rho_2}} {\rm{ CoVaR}}_{\alpha, \beta}^\mathbb F(Y\vert X) \geqslant \theta. To see it, for any \varepsilon>0 , there exists (X_1,Y_1) such that \mathbb F_{(X_1,Y_1)}\in\mathcal F_{\rho_1} and {\rm{ CoVaR}}_{\alpha, \beta}(Y_1\vert X_1) \geqslant \theta- \varepsilon. We denote the copula of (X_1,Y_1) by C1. Let (X_1^c,Y_1^c) be a random vector, with the same marginal distributions as (X_1,Y_1) with the comonotonicity copula C^M and denote the correlation coefficient of (X_1^c,Y_1^c) by ρ0. We consider the following two cases.

Case 1: If \rho_1<\rho_2 \leqslant \rho_{0} , then denote by \lambda = ({\rho_0-\rho_2})/({\rho_0-\rho_1}) , and define (X_2,Y_2) that has the same marginal distributions as (X_1,Y_1) with the copula C_2 = \lambda C_1+(1-\lambda)C^M . It can be observed that {\rm{ corr}}(X_2,Y_2) = \lambda \rho_1+(1-\lambda)\rho_0 = \rho_2 ; hence, \mathbb F_{(X_2,Y_2)}\in\mathcal F_{\rho_2} . As C_1 \leqslant C_2 pointwisely, it follows from Proposition 2.1 that

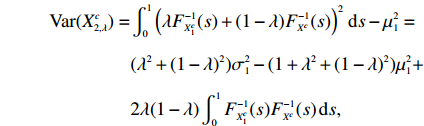

Case 2: If \rho_0<\rho_2 , then denote by X^c = {\sigma_1}(Y_1^c-\mu_2)/{\sigma_2}+\mu_1 . We know that \mathbb{E}[X^c] = \mu_1 , {\rm{ Var}}(X^c) = \sigma_1^2 and {\rm{ corr}}(X^c,Y_1^c) = 1 . For \lambda\in[0,1] , let X_{2,\lambda}^c with quantile function F_{X_{2,\lambda}^c}^{-1} = \lambda F_{X_1^c}^{-1}+(1-\lambda) F_{X^c}^{-1}, and (X_{2,\lambda}^c,Y_1^c) has the comonotonicity copula C^M . One can calculate that \mathbb{E}[X_{2,\lambda}^c] = \mu_1 ,

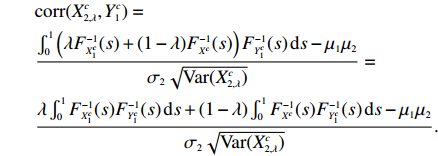

We find that the function \lambda\mapsto {\rm{ Var}}(X_{2,\lambda}^c) is continuous, and hence, the function \lambda\mapsto f(\lambda): = {\rm{ corr}}(X_{2,\lambda}^c,Y_1^c) is continuous. Also note that f(0) = {\rm{ corr}}(X^c,Y_1^c) = 1 and f(1) = {\rm{ corr}} (X_1^c,Y_1^c) = \rho_0 , and \rho_2\in(\rho_0,1] . There exists \lambda^*\in[0,1] such that f(\lambda^*) = {\rm{ corr}}(X_{2,\lambda^*}^c,Y_1^c) = \rho_2 . Now, let a>0 , b\in \mathbb{R} and X_2 = a X_{2,\lambda^*}^c+ b such that \mathbb{E}[X_2] = \mu_1 and {\rm{ Var}}(X_2) = \sigma_1^2 . It can be seen that {\rm{ corr}}(X_2,Y_1^c) = {\rm{ corr}}(X_{2,\lambda^*}^c,Y_1^c) = \rho_2 , and (X_2,Y_1^c) has the comonotonicity copula C^M ; hence, \mathbb F_{(X_2,Y_1^c)}\in\mathcal F_{\rho_2} . From Proposition 2.1, we have

where the second inequality holds because (X_1,Y_1) and (X_1^c,Y_1^c) have the same marginal distributions, and (X_1^c,Y_1^c) has the comonotonicity copula C^M .

Combing Cases 1 and 2, and noting that \varepsilon>0 is arbitrary, we have \sup_{\mathbb F\in \mathcal F_{\rho_2}} {\rm{ CoVaR}}_{\alpha, \beta}^\mathbb F(Y\vert X) \geqslant \theta. This completes the proof.

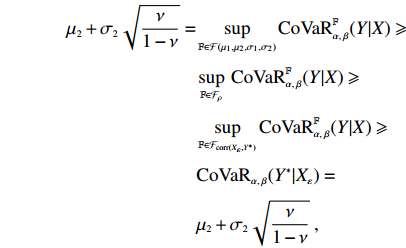

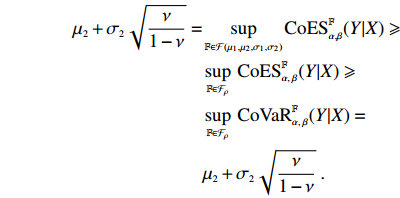

Based on Lemma 3.2, if \rho_0\in[0,1] makes (12) become equalities, then so does for all \rho \geqslant\rho_0 . The following theorem shows that zero is a lower bound of \rho that (12) holds as equalities.

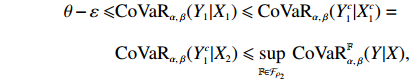

Theorem 3.2. For \mu_i\in \mathbb{R} , \sigma_i>0 , i = 1,2 , \rho\in[-1,1] , let \mathcal F_\rho = \mathcal F(\mu_1,\mu_2,\sigma_1,\sigma_2,\rho) defined by Eq. (11). If \rho >0 , then we have

Proof. Let Y^* be a random variable with distribution

G = \nu\delta_{\mu_2-\sigma_2\sqrt{\dfrac{1-\nu}{\nu}}} +(1-\nu)\delta_{\mu_2+\sigma_2\sqrt{\dfrac{\nu}{1-\nu}}}\;,

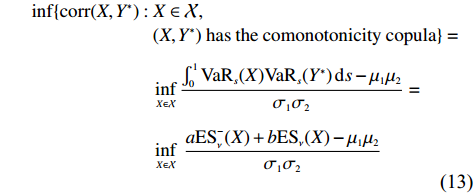

and we define \mathcal X = \{X: \mathbb{E}[X] = \mu_1,{\rm{ Var}}(X) = \sigma_1^2\} . From Theorem 3.1, for any X\in\mathcal X such that (X,Y^*) has the comonotonicity copula, we have {\rm{ CoVaR}}_{\alpha,\; \beta}(Y^*\vert X) = \mu_2 +\sigma_2\sqrt{{\nu}/({1-\nu})}. We consider the following optimization problem:

where the first equality holds because b-{(1-\nu)a}/{\nu} = \sigma_2\sqrt{({1-\nu})/{\nu}} \geqslant0 , and the second equality follows from Ref. [18, Corollary 5]. Hence, for any \rho\in(0,1] , there exists X_ \varepsilon\in\mathcal X such that (X_ \varepsilon,Y^*) has the comonotonicity copula with {\rm{ corr}}(X_ \varepsilon,Y^*)\in(0,\; \rho), and {\rm{ CoVaR}}_{\alpha, \beta}(Y^*\vert X_ \varepsilon) = \mu_2 + \sigma_2\sqrt{{\nu}/({1-\nu})} . Therefore,

where \mathcal F(\mu_1,\mu_2,\sigma_1,\sigma_2) is defined by Eq. (10), and the second inequality follows from Lemma 3.2. Hence, we verify that \sup_{\mathbb F\in \mathcal F_\rho} {\rm{ CoVaR}}^\mathbb F_{\alpha, \beta}(Y\vert X) = \mu_2 +\sigma_2\sqrt{{\nu}/({1-\nu})} for all \rho\in(0,1] . Because {\rm{ CoES}} \geqslant{\rm{ CoVaR}} , we have for any \rho\in(0,1] ,

Hence, we have \sup_{\mathbb F\in \mathcal F_\rho}\; {\rm{ CoES}}^\mathbb F_{\alpha,\; \beta}(Y\vert X) = \mu_2 +\sigma_2\sqrt{{\nu}/({1-\nu})} for all \rho\in(0,1] . This completes the proof.

Remark 3.1. Theorem 3.2 shows that it holds equalities for (12) if the underlying random vector (X,Y) is positively correlated.

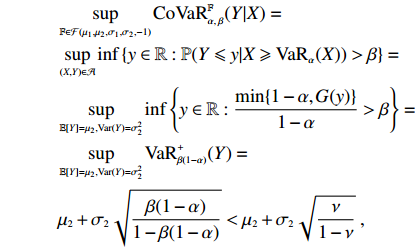

Nevertheless, this result cannot hold for all \rho\in[-1,1] . For instance, if {\rm{ corr}}(X,Y) = -1 , then for any \mathbb F_{(X,Y)}\in \mathcal F(\mu_1,\mu_2,\sigma_1, \sigma_2,-1), it holds that X = {\sigma_1}(\mu_2-Y)/ {\sigma_2}+\mu_1. Let \mathcal A = \{(X,Y): { \mathbb{E}[Y] = \mu_2,{\rm{ Var}}(Y) = \sigma_2^2,X = {\sigma_1}(\mu_2-Y)/{\sigma_2}+\mu_1}\} , and we have

where the fourth equality follows from Lemma 3.1. It is beyond current technology to calculate the value of the worst-case CoVaR and CoES under the uncertainty set \mathcal F(\mu_1, \mu_2,\sigma_1,\sigma_2,\rho) when \rho \leqslant 0 . However, this could be an open question.

4

Simulation

In this section, we investigate the (worst-case) CoVaR and CoES in two cases: ① the true underlying distribution is a bivariate Gaussian or bivariate t-distribution with different correlation coefficients; ② the true underlying marginal distribution is a Pareto distribution with different copulas. In both cases, we include the worst-case CoVaR and CoES, where the partial information is induced by the given true underlying distribution.

4.1

CoVaR and CoES with Gaussian or t-distribution

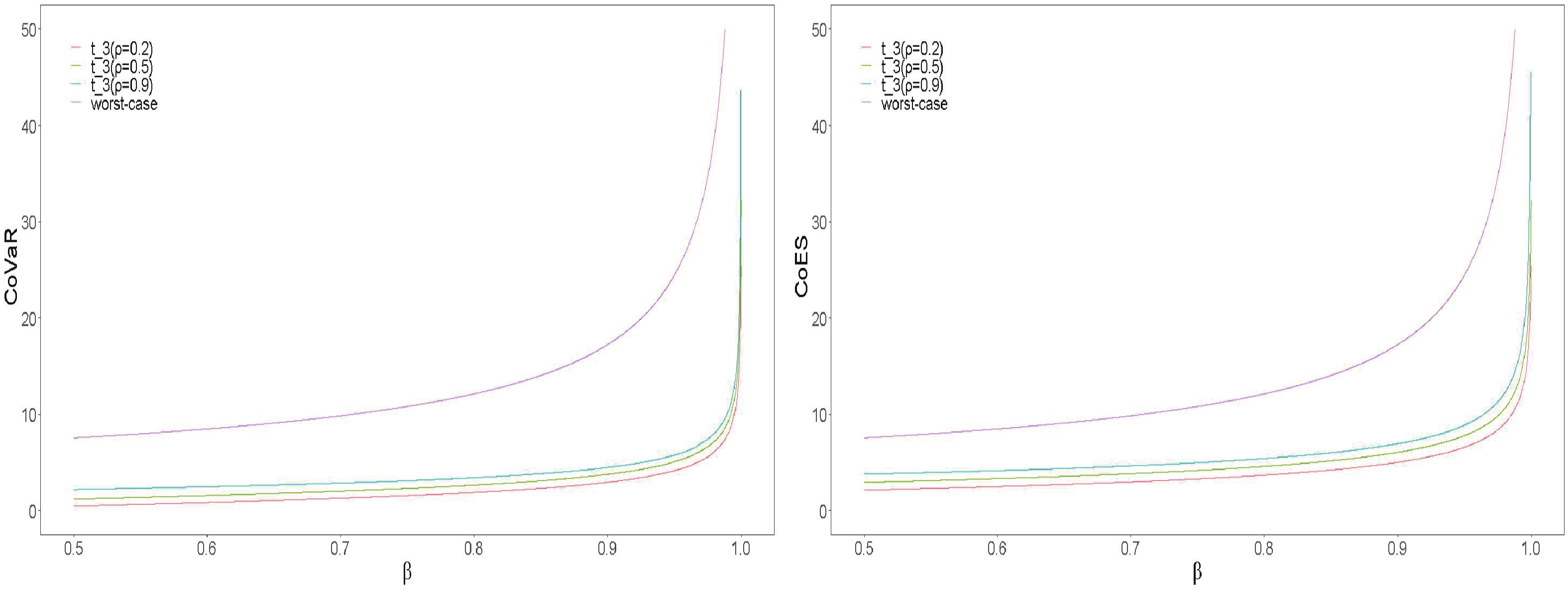

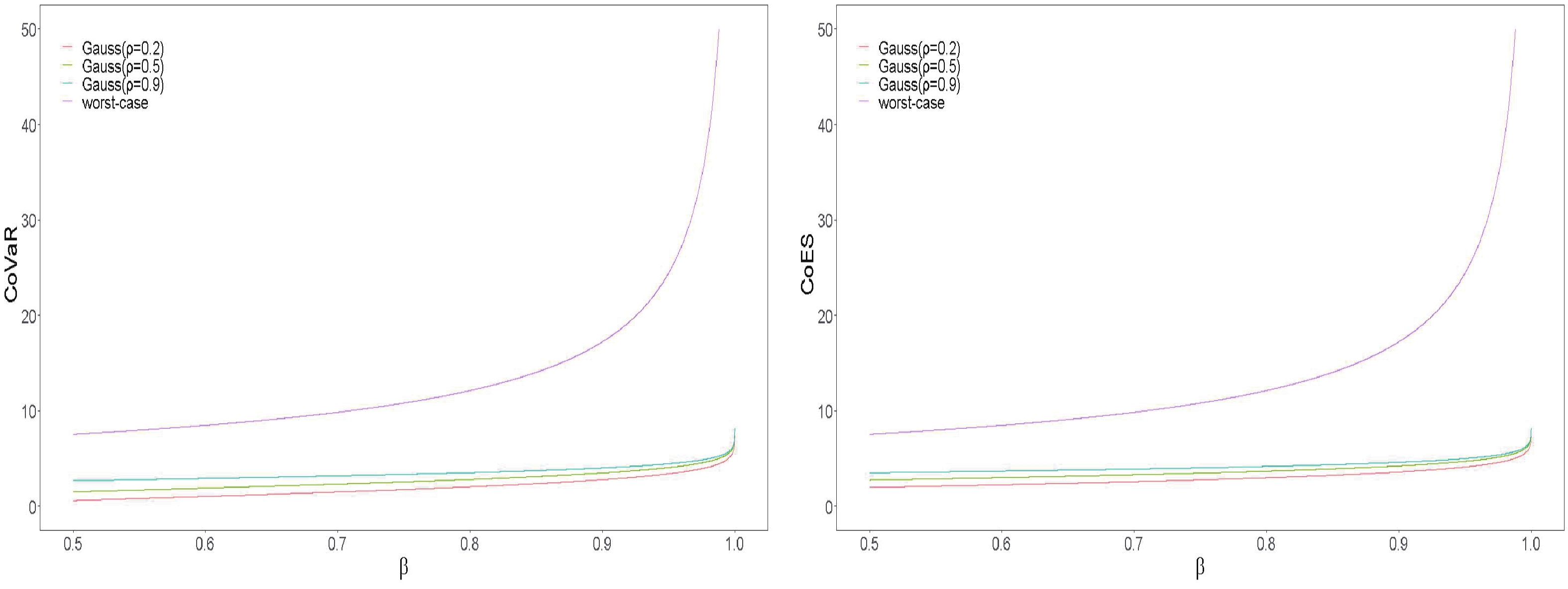

In this subsection, we investigate the value of {\rm{ CoVaR}}_{\alpha,\;\beta} and {\rm{ CoES}}_{\alpha,\;\beta} when the true underlying distribution is a bivariate Gaussian or bivariate t-distribution. The marginal mean and variance of the Gaussian and t-distribution are chosen as \mu_1 = \mu_2 = 0,\; \sigma_1^2 = \sigma_2^2 = 3 . In both cases, we consider three correlation coefficients, that is \rho = 0.2,\; 0.5 and 0.9 , and fix the parameter \alpha = 0.9 , and \beta ranges from 0.5 to 1. The worst-case {\rm{ CoVaR}}_{\alpha,\;\beta} and {\rm{ CoES}}_{\alpha,\;\beta} are derived by the moment information of the underlying distribution, the value of which is

The corresponding values of {\rm{ CoVaR}}_{\alpha,\;\beta} and {\rm{ CoES}}_{\alpha,\;\beta} are showed in Figs. 1 and 2. Note that all given correlation coefficients are positive. From Theorem 3.2, the values of the worst-case CoVaR and CoES are also equal to Eq. (14) if the partial information is derived from the first two marginal moments and the correlation coefficient of the given distribution.

Figure

1.

CoVaR and CoES with bivariate Gaussian distributions.

In Figs. 1 and 2, the values of CoVaR and CoES increase when the correlation coefficient \rho increases, and the worst-case CoVaR (CoES) is always larger than the CoVaR (CoES) generated by the true underlying distribution. Moreover, we find that the value of CoVaR (CoES) with a t-distribution is larger than that with Gaussian distribution when \beta is close to 1. This is because the t-distribution has a heavier tail than the Gaussian distribution does.

4.2

CoVaR and CoES with different copulas

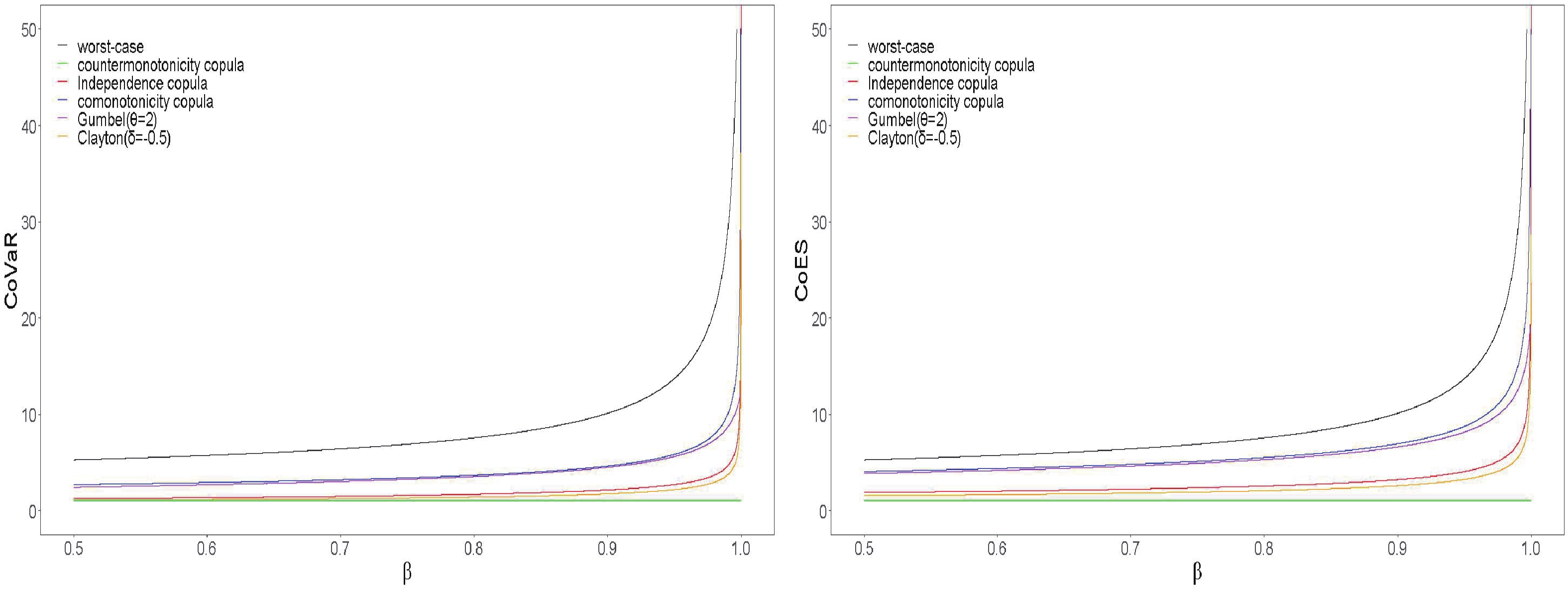

In this subsection, we consider the values of CoVaR and CoES when the marginal distribution of the true underlying distribution is fixed as a Pareto distribution with an essential infimum x_{\min} = 1 and tail parameter k = 3 , that is, F(x) = (1-x^{-3}) {1{}}_{\{x \geqslant1\}}, and copula changes. In all cases, the parameter \alpha = 0.9 , and \beta ranges from 0.5 to 1. In the following, we collect a few common copulas other than the comonotonicity copula, which is introduced in Section 2.2.

For Clayton and Gumbel copula, we let the parameter \delta = -0.5 and \theta = 2 , respectively. The worst-case {\rm{ CoVaR}}_{\alpha,\;\beta} and {\rm{ CoES}}_{\alpha,\;\beta} are derived from the moment information of the Pareto marginal distribution, that is

where \mu = 3/2 and \sigma^2 = 3/4 denote the mean and variance of the marginal Pareto distribution, respectively. Fig. 3 shows the values of the worst-case CoVaR and CoES, and the CoVaR and CoES with Pareto marginal and different copulas introduced above.

Figure

3.

CoVaR and CoES with Pareto marginal and different copulas.

As shown by Fig. 3, sorted the value of CoVaR of these copulas from small to large, we have countermonotonicity copula, Clayton copula ( \delta = -0.5 ), independence copula, Gumbel copula ( \theta = 2 ) and comonotonicity copula, while the worst-case CoVaR is the largest. The case of CoES has a same performance. This is because C^C \leqslant C_{-0.5} \leqslant C^I \leqslant G_{2} \leqslant C^M on [0,1]\times[0,1] . Hence, Proposition 2.1 can be applied. Note that the correlated coefficients of Gumbel and comonotonicity copula are positive. By Theorem 3.2, in the cases of these two copulas, the value of the worst-case CoVaR and CoES are also equal to (15) if the partial information is derived from the first two moments of the marginal distribution and the correlation coefficient of the given copula.

5.

Conclusions

In this paper, we study the worst-case {\rm{ CoVaR}}_{\alpha,\;\beta} and {\rm{ CoES}}_{\alpha,\;\beta} in case of model uncertainty with a known mean and covariance of the portfolio (X,Y) , that is, the uncertainty set is \mathcal F(\mu_1,\mu_2,\sigma_1,\sigma_2,\rho) defined by (11). When the correlation coefficient \rho > 0 , the values of the worst-case {\rm{ CoVaR}}_{\alpha,\;\beta} and {\rm{ CoES}}_{\alpha,\;\beta} are equal to a constant \mu_2+\sigma_2\sqrt{{\nu}/({1-\nu})}. To calculate the value of the worst-case CoVaR and CoES with uncertainty set \mathcal F(\mu_1,\mu_2,\sigma_1,\sigma_2,\rho) when \rho \leqslant 0 is beyond current technology, and it could be an open question.

Acknowledgements

This work was supported by the National Natural Science Foundation of China (71671176 , 71871208).

Conflict of interest

The authors declare that they have no conflict of interest.

Conflict of Interest

The authors declare that they have no conflict of interest.

The relationship between CoVaR, CoES and dependence structure are investigated.

In case where the first two marginal moments are known, the closed-form solution and the valueof the worst-case CoVaR and CoES are derived.

The worst-case CoVaR and CoES under mean and covariance information are investigated.

Basel Committee on Banking Supervision. Minimum capital requirements for market risk. Basel, Switzerland: Bank for International Settlements, 2019.

[2]

Adrian T, Brunnermeier M K. CoVaR. American Economic Review,2016, 106 (7): 1705–1741. DOI: 10.1257/aer.20120555

[3]

Brownlees C, Engle R F. SRISK: A conditional capital shortfall measure of systemic risk. The Review of Financial Studies,2017, 30 (1): 48–79. DOI: 10.1093/rfs/hhw060

[4]

Acharya V V, Pedersen L H, Philippon T, et al. Measuring systemic risk. The Review of Financial Studies,2017, 30 (1): 2–47. DOI: 10.1093/rfs/hhw088

[5]

Girardi G, Ergün A T. Systemic risk measurement: Multivariate GARCH estimation of CoVaR. Journal of Banking & Finance,2013, 37 (8): 3169–3180. DOI: 10.1016/j.jbankfin.2013.02.027

[6]

Huang W Q, Uryasev S. The CoCVaR approach: Systemic risk contribution measurement. Journal of Risk,2018, 20 (4): 75–93. DOI: 10.21314/JOR.2018.383

[7]

López-Espinosa G, Moreno A, Rubia A, et al. Short-term wholesale funding and systemic risk: A global CoVaR approach. Journal of Banking & Finance,2012, 36 (12): 3150–3162. DOI: 10.1016/j.jbankfin.2012.04.020

[8]

Karimalis E N, Nomikos N K. Measuring systemic risk in the European banking sector: A Copula CoVaR approach. The European Journal of Finance,2018, 24 (11): 944–975. DOI: 10.1080/1351847X.2017.1366350

[9]

Popescu I. Robust mean-covariance solutions for stochastic optimization. Operations Research,2007, 51 (1): 98–112. DOI: 10.1287/opre.1060.0353

[10]

Bertsimas D, Doan X V, Natarajan K, et al. Models for minimax stochastic linear optimization problems with risk aversion. Mathematics of Operations Research,2010, 35 (3): 580–602. DOI: 10.1287/moor.1100.0445

[11]

Delage E, Ye Y. Distributionally robust optimization under moment uncertainty with application to data-driven problems. Operations Research,2010, 58 (3): 595–612. DOI: 10.1287/opre.1090.0741

[12]

Natarajan K, Sim M, Uichanco J. Tractable robust expected utility and risk models for portfolio optimization. Mathematical Finance,2010, 20 (4): 695–731. DOI: 10.1111/j.1467-9965.2010.00417.x

Chen L, He S, Zhang S. Tight bounds for some risk measures, with applications to robust portfolio selection. Operations Research,2011, 59 (4): 847–865. DOI: 10.1287/opre.1110.0950

[15]

Nelsen R B. An Introduction to Copulas. 2nd edition. New York: Springer, 2006.

[16]

Mainik G, Schaanning E. On dependence consistency of CoVaR and some other systemic risk measures. Statistics & Risk Modeling,2014, 31 (1): 49–77. DOI: 10.1515/strm-2013-1164

[17]

Ghaoui L E, Oks M, Oustry F. Worst-case value-at-risk and robust portfolio optimization: A conic programming approach. Operations Research,2003, 51 (4): 543–556. DOI: 10.1287/opre.51.4.543.16101

Figure

1.

CoVaR and CoES with bivariate Gaussian distributions.

Figure

2.

CoVaR and CoES with bivariate t-distributions.

Figure

3.

CoVaR and CoES with Pareto marginal and different copulas.

References

[1]

Basel Committee on Banking Supervision. Minimum capital requirements for market risk. Basel, Switzerland: Bank for International Settlements, 2019.

[2]

Adrian T, Brunnermeier M K. CoVaR. American Economic Review,2016, 106 (7): 1705–1741. DOI: 10.1257/aer.20120555

[3]

Brownlees C, Engle R F. SRISK: A conditional capital shortfall measure of systemic risk. The Review of Financial Studies,2017, 30 (1): 48–79. DOI: 10.1093/rfs/hhw060

[4]

Acharya V V, Pedersen L H, Philippon T, et al. Measuring systemic risk. The Review of Financial Studies,2017, 30 (1): 2–47. DOI: 10.1093/rfs/hhw088

[5]

Girardi G, Ergün A T. Systemic risk measurement: Multivariate GARCH estimation of CoVaR. Journal of Banking & Finance,2013, 37 (8): 3169–3180. DOI: 10.1016/j.jbankfin.2013.02.027

[6]

Huang W Q, Uryasev S. The CoCVaR approach: Systemic risk contribution measurement. Journal of Risk,2018, 20 (4): 75–93. DOI: 10.21314/JOR.2018.383

[7]

López-Espinosa G, Moreno A, Rubia A, et al. Short-term wholesale funding and systemic risk: A global CoVaR approach. Journal of Banking & Finance,2012, 36 (12): 3150–3162. DOI: 10.1016/j.jbankfin.2012.04.020

[8]

Karimalis E N, Nomikos N K. Measuring systemic risk in the European banking sector: A Copula CoVaR approach. The European Journal of Finance,2018, 24 (11): 944–975. DOI: 10.1080/1351847X.2017.1366350

[9]

Popescu I. Robust mean-covariance solutions for stochastic optimization. Operations Research,2007, 51 (1): 98–112. DOI: 10.1287/opre.1060.0353

[10]

Bertsimas D, Doan X V, Natarajan K, et al. Models for minimax stochastic linear optimization problems with risk aversion. Mathematics of Operations Research,2010, 35 (3): 580–602. DOI: 10.1287/moor.1100.0445

[11]

Delage E, Ye Y. Distributionally robust optimization under moment uncertainty with application to data-driven problems. Operations Research,2010, 58 (3): 595–612. DOI: 10.1287/opre.1090.0741

[12]

Natarajan K, Sim M, Uichanco J. Tractable robust expected utility and risk models for portfolio optimization. Mathematical Finance,2010, 20 (4): 695–731. DOI: 10.1111/j.1467-9965.2010.00417.x

Chen L, He S, Zhang S. Tight bounds for some risk measures, with applications to robust portfolio selection. Operations Research,2011, 59 (4): 847–865. DOI: 10.1287/opre.1110.0950

[15]

Nelsen R B. An Introduction to Copulas. 2nd edition. New York: Springer, 2006.

[16]

Mainik G, Schaanning E. On dependence consistency of CoVaR and some other systemic risk measures. Statistics & Risk Modeling,2014, 31 (1): 49–77. DOI: 10.1515/strm-2013-1164

[17]

Ghaoui L E, Oks M, Oustry F. Worst-case value-at-risk and robust portfolio optimization: A conic programming approach. Operations Research,2003, 51 (4): 543–556. DOI: 10.1287/opre.51.4.543.16101

DownLoad:

DownLoad: