| [1] |

Borch K. An attempt to determine the optimum amount of stop loss reinsurance. In: Transactions of the 16th International Congress of Actuaries. Brussels, Belgium: International Congress of Actuaries, 1960: 597–610.

|

| [2] |

Arrow K J. Uncertainty and the welfare economics of medical care. The American Economic Review, 1963, 53 (5): 941–973.

|

| [3] |

Kaluszka M. Optimal reinsurance under mean-variance premium principles. Insurance: Mathematics and Economics, 2001, 28 (1): 61–67. doi: 10.1016/S0167-6687(00)00066-4

|

| [4] |

Kaluszka M, Krzeszowiec M. Pricing insurance contracts under cumulative prospect theory. Insurance: Mathematics and Economics, 2012, 50 (1): 159–166. doi: 10.1016/j.insmatheco.2011.11.001

|

| [5] |

Cai J, Tan K S, Weng C, et al. Optimal reinsurance under VaR and CTE risk measures. Insurance: Mathematics and Economics, 2008, 43 (1): 185–196. doi: 10.1016/j.insmatheco.2008.05.011

|

| [6] |

Cheung K C. Optimal reinsurance revisited: A geometric approach. ASTIN Bulletin, 2010, 40 (1): 221–239. doi: 10.2143/AST.40.1.2049226

|

| [7] |

Cui W, Yang J, Wu L. Optimal reinsurance minimizing the distortion risk measure under general reinsurance premium principles. Insurance: Mathematics and Economics, 2013, 53 (1): 74–85. doi: 10.1016/j.insmatheco.2013.03.007

|

| [8] |

Cheung K C, Sung K, Yam S, et al. Optimal reinsurance under general law-invariant risk measures. Scandinavian Actuarial Journal, 2014, 2014 (1): 72–91. doi: 10.1080/03461238.2011.636880

|

| [9] |

Cai J, Liu H, Wang R. Pareto-optimal reinsurance arrangements under general model settings. Insurance: Mathematics and Economics, 2017, 77: 24–37. doi: 10.1016/j.insmatheco.2017.08.004

|

| [10] |

Asimit A V, Cheung K C, Chong W F, et al. Pareto-optimal insurance contracts with premium budget and minimum charge constraints. Insurance: Mathematics and Economics, 2020, 95: 17–27. doi: 10.1016/j.insmatheco.2020.08.001

|

| [11] |

Jiang W, Hong H, Ren J. Pareto-optimal reinsurance policies with maximal synergy. Insurance: Mathematics and Economics, 2021, 96: 185–198. doi: 10.1016/j.insmatheco.2020.11.009

|

| [12] |

Borch K. The optimal reinsurance treaty. ASTIN Bulletin, 1969, 5 (2): 293–297. doi: 10.1017/S051503610000814X

|

| [13] |

Aase K. The Nash bargaining solution vs. equilibrium in a reinsurance syndicate. Scandinavian Actuarial Journal, 2009, 2009 (3): 219–238. doi: 10.1080/03461230802425834

|

| [14] |

Boonen T, Tan K S, Zhuang S C. Pricing in reinsurance bargaining with comonotonic additive utility functions. ASTIN Bulletin, 2016, 46 (2): 507–530. doi: 10.1017/asb.2016.8

|

| [15] |

Chen L, Shen Y. On a new paradigm of optimal reinsurance: A stochastic Stackelberg differential game between an insurer and a reinsurer. ASTIN Bulletin, 2018, 48 (2): 905–960. doi: 10.1017/asb.2018.3

|

| [16] |

Cheung K C, Yam S C P, Zhang Y. Risk-adjusted Bowley reinsurance under distorted probabilities. Insurance: Mathematics and Economics, 2019, 86: 64–72. doi: 10.1016/j.insmatheco.2019.02.006

|

| [17] |

Gavagan J, Hu L, Lee G, et al. Optimal reinsurance with model uncertainty and Stackelberg game. Scandinavian Actuarial Journal, 2022, 2022 (1): 29–48. doi: 10.1080/03461238.2021.1925735

|

| [18] |

Horst U, Moreno-Bromberg S. Risk minimization and optimal derivative design in a principal agent game. Mathematics and Financial Economics, 2008, 2 (1): 1–27. doi: 10.1007/s11579-008-0012-8

|

| [19] |

Cheung K C, Yam S C P, Yuen F. Reinsurance contract design with adverse selection. Scandinavian Actuarial Journal, 2019, 2019 (9): 784–798. doi: 10.1080/03461238.2019.1616323

|

| [20] |

Chan F, Gerber H. The reinsurer’s monopoly and the Bowley solution. ASTIN Bulletin, 1985, 15 (2): 141–148. doi: 10.2143/AST.15.2.2015025

|

| [21] |

Boonen T J, Cheung K C, Zhang Y. Bowley reinsurance with asymmetric information on the insurer’s risk preferences. Scandinavian Actuarial Journal, 2021, 2021 (7): 623–644. doi: 10.1080/03461238.2020.1867631

|

| [22] |

Boonen T J, Zhang Y. Bowley reinsurance with asymmetric information: a first-best solution. Scandinavian Actuarial Journal, 2022, 2022 (6): 532–551. doi: 10.1080/03461238.2021.1998922

|

| [23] |

Liang X, Wang R, Young V. Optimal insurance to maximize RDEU under a distortion-deviation premium principle. Insurance: Mathematics and Economics, 2022, 104: 35–59. doi: 10.1016/j.insmatheco.2022.01.007

|

| [24] |

Asimit A V, Badescu A M, Cheung K C. Optimal reinsurance in the presence of counterparty default risk. Insurance: Mathematics and Economics, 2013, 53 (3): 690–697. doi: 10.1016/j.insmatheco.2013.09.012

|

| [25] |

Asimit A V, Badescu A M, Verdonck T. Optimal risk transfer under quantile-based risk measurers. Insurance: Mathematics and Economics, 2013, 53 (1): 252–265. doi: 10.1016/j.insmatheco.2013.05.005

|

| [26] |

Cai J, Lemieux C, Liu F. Optimal reinsurance with regulatory initial capital and default risk. Insurance: Mathematics and Economics, 2014, 57: 13–24. doi: 10.1016/j.insmatheco.2014.04.006

|

| [27] |

Lo A. How does reinsurance create value to an insurer? A cost-benefit analysis incorporating default risk. Risks, 2016, 4 (4): 48. doi: /10.3390/risks4040048

|

| [28] |

Huberman G, Mayers D, Smith Jr C W. Optimal insurance policy indemnity schedules. Bell Journal of Economics, 1983, 14 (2): 415–426. doi: 10.2307/3003643

|

| [29] |

Zhuang S C, Weng C, Tan K S. et al. Marginal indemnification function formulation for optimal reinsurance. Insurance: Mathematics and Economics, 2016, 67: 65–76. doi: 10.1016/j.insmatheco.2015.12.003

|

| [30] |

Wang S S. Premium calculation by transforming the layer premium density. ASTIN Bulletin, 1996, 26: 71–92. doi: 10.2143/AST.26.1.563234

|

| [31] |

Denneberg D. Premium calculation: Why standard deviation should be replaced by absolute deviation. ASTIN Bulletin, 1990, 20 (2): 181–190. doi: 10.2143/AST.20.2.2005441

|

| [32] |

Laffont J J, Martimort D. The Theory of Incentives: The Principal-Agent Model. Princeton, USA: Princeton University Press, 2009.

|

| [33] |

Boonen T J, Jiang W. Mean-variance insurance design with counterparty risk and incentive compatibility. ASTIN Bulletin, 2022, 52 (2): 645–667. doi: 10.1017/asb.2021.36

|

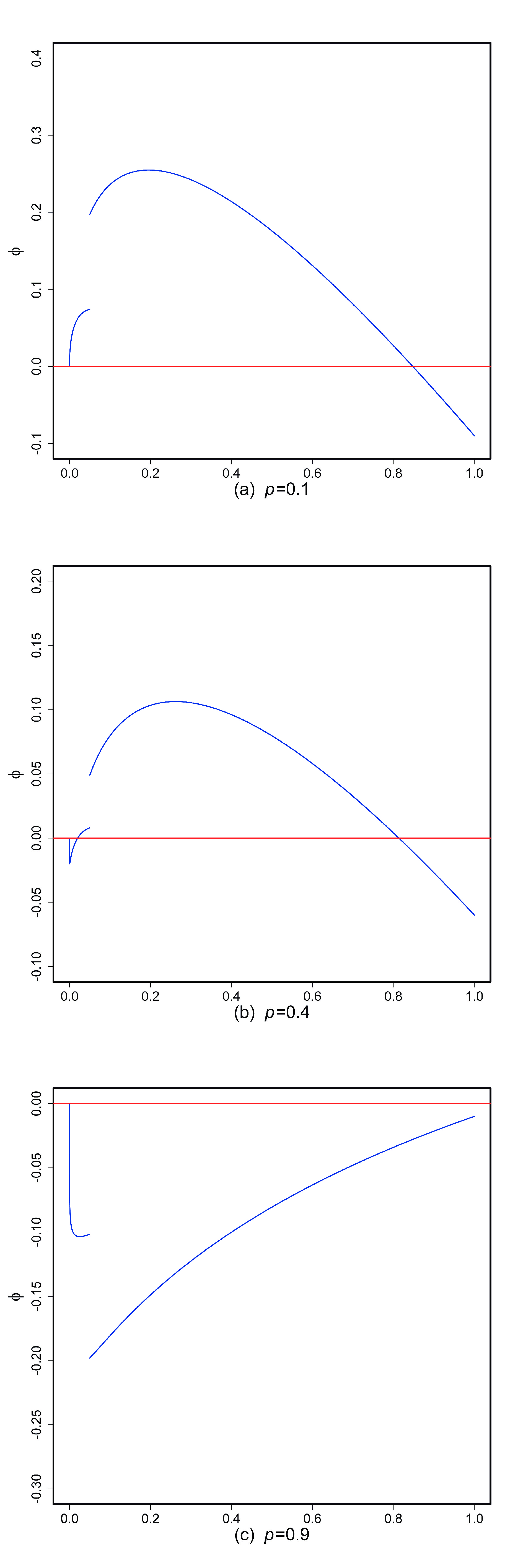

Figure

1.

Plots of the function

| [1] |

Borch K. An attempt to determine the optimum amount of stop loss reinsurance. In: Transactions of the 16th International Congress of Actuaries. Brussels, Belgium: International Congress of Actuaries, 1960: 597–610.

|

| [2] |

Arrow K J. Uncertainty and the welfare economics of medical care. The American Economic Review, 1963, 53 (5): 941–973.

|

| [3] |

Kaluszka M. Optimal reinsurance under mean-variance premium principles. Insurance: Mathematics and Economics, 2001, 28 (1): 61–67. doi: 10.1016/S0167-6687(00)00066-4

|

| [4] |

Kaluszka M, Krzeszowiec M. Pricing insurance contracts under cumulative prospect theory. Insurance: Mathematics and Economics, 2012, 50 (1): 159–166. doi: 10.1016/j.insmatheco.2011.11.001

|

| [5] |

Cai J, Tan K S, Weng C, et al. Optimal reinsurance under VaR and CTE risk measures. Insurance: Mathematics and Economics, 2008, 43 (1): 185–196. doi: 10.1016/j.insmatheco.2008.05.011

|

| [6] |

Cheung K C. Optimal reinsurance revisited: A geometric approach. ASTIN Bulletin, 2010, 40 (1): 221–239. doi: 10.2143/AST.40.1.2049226

|

| [7] |

Cui W, Yang J, Wu L. Optimal reinsurance minimizing the distortion risk measure under general reinsurance premium principles. Insurance: Mathematics and Economics, 2013, 53 (1): 74–85. doi: 10.1016/j.insmatheco.2013.03.007

|

| [8] |

Cheung K C, Sung K, Yam S, et al. Optimal reinsurance under general law-invariant risk measures. Scandinavian Actuarial Journal, 2014, 2014 (1): 72–91. doi: 10.1080/03461238.2011.636880

|

| [9] |

Cai J, Liu H, Wang R. Pareto-optimal reinsurance arrangements under general model settings. Insurance: Mathematics and Economics, 2017, 77: 24–37. doi: 10.1016/j.insmatheco.2017.08.004

|

| [10] |

Asimit A V, Cheung K C, Chong W F, et al. Pareto-optimal insurance contracts with premium budget and minimum charge constraints. Insurance: Mathematics and Economics, 2020, 95: 17–27. doi: 10.1016/j.insmatheco.2020.08.001

|

| [11] |

Jiang W, Hong H, Ren J. Pareto-optimal reinsurance policies with maximal synergy. Insurance: Mathematics and Economics, 2021, 96: 185–198. doi: 10.1016/j.insmatheco.2020.11.009

|

| [12] |

Borch K. The optimal reinsurance treaty. ASTIN Bulletin, 1969, 5 (2): 293–297. doi: 10.1017/S051503610000814X

|

| [13] |

Aase K. The Nash bargaining solution vs. equilibrium in a reinsurance syndicate. Scandinavian Actuarial Journal, 2009, 2009 (3): 219–238. doi: 10.1080/03461230802425834

|

| [14] |

Boonen T, Tan K S, Zhuang S C. Pricing in reinsurance bargaining with comonotonic additive utility functions. ASTIN Bulletin, 2016, 46 (2): 507–530. doi: 10.1017/asb.2016.8

|

| [15] |

Chen L, Shen Y. On a new paradigm of optimal reinsurance: A stochastic Stackelberg differential game between an insurer and a reinsurer. ASTIN Bulletin, 2018, 48 (2): 905–960. doi: 10.1017/asb.2018.3

|

| [16] |

Cheung K C, Yam S C P, Zhang Y. Risk-adjusted Bowley reinsurance under distorted probabilities. Insurance: Mathematics and Economics, 2019, 86: 64–72. doi: 10.1016/j.insmatheco.2019.02.006

|

| [17] |

Gavagan J, Hu L, Lee G, et al. Optimal reinsurance with model uncertainty and Stackelberg game. Scandinavian Actuarial Journal, 2022, 2022 (1): 29–48. doi: 10.1080/03461238.2021.1925735

|

| [18] |

Horst U, Moreno-Bromberg S. Risk minimization and optimal derivative design in a principal agent game. Mathematics and Financial Economics, 2008, 2 (1): 1–27. doi: 10.1007/s11579-008-0012-8

|

| [19] |

Cheung K C, Yam S C P, Yuen F. Reinsurance contract design with adverse selection. Scandinavian Actuarial Journal, 2019, 2019 (9): 784–798. doi: 10.1080/03461238.2019.1616323

|

| [20] |

Chan F, Gerber H. The reinsurer’s monopoly and the Bowley solution. ASTIN Bulletin, 1985, 15 (2): 141–148. doi: 10.2143/AST.15.2.2015025

|

| [21] |

Boonen T J, Cheung K C, Zhang Y. Bowley reinsurance with asymmetric information on the insurer’s risk preferences. Scandinavian Actuarial Journal, 2021, 2021 (7): 623–644. doi: 10.1080/03461238.2020.1867631

|

| [22] |

Boonen T J, Zhang Y. Bowley reinsurance with asymmetric information: a first-best solution. Scandinavian Actuarial Journal, 2022, 2022 (6): 532–551. doi: 10.1080/03461238.2021.1998922

|

| [23] |

Liang X, Wang R, Young V. Optimal insurance to maximize RDEU under a distortion-deviation premium principle. Insurance: Mathematics and Economics, 2022, 104: 35–59. doi: 10.1016/j.insmatheco.2022.01.007

|

| [24] |

Asimit A V, Badescu A M, Cheung K C. Optimal reinsurance in the presence of counterparty default risk. Insurance: Mathematics and Economics, 2013, 53 (3): 690–697. doi: 10.1016/j.insmatheco.2013.09.012

|

| [25] |

Asimit A V, Badescu A M, Verdonck T. Optimal risk transfer under quantile-based risk measurers. Insurance: Mathematics and Economics, 2013, 53 (1): 252–265. doi: 10.1016/j.insmatheco.2013.05.005

|

| [26] |

Cai J, Lemieux C, Liu F. Optimal reinsurance with regulatory initial capital and default risk. Insurance: Mathematics and Economics, 2014, 57: 13–24. doi: 10.1016/j.insmatheco.2014.04.006

|

| [27] |

Lo A. How does reinsurance create value to an insurer? A cost-benefit analysis incorporating default risk. Risks, 2016, 4 (4): 48. doi: /10.3390/risks4040048

|

| [28] |

Huberman G, Mayers D, Smith Jr C W. Optimal insurance policy indemnity schedules. Bell Journal of Economics, 1983, 14 (2): 415–426. doi: 10.2307/3003643

|

| [29] |

Zhuang S C, Weng C, Tan K S. et al. Marginal indemnification function formulation for optimal reinsurance. Insurance: Mathematics and Economics, 2016, 67: 65–76. doi: 10.1016/j.insmatheco.2015.12.003

|

| [30] |

Wang S S. Premium calculation by transforming the layer premium density. ASTIN Bulletin, 1996, 26: 71–92. doi: 10.2143/AST.26.1.563234

|

| [31] |

Denneberg D. Premium calculation: Why standard deviation should be replaced by absolute deviation. ASTIN Bulletin, 1990, 20 (2): 181–190. doi: 10.2143/AST.20.2.2005441

|

| [32] |

Laffont J J, Martimort D. The Theory of Incentives: The Principal-Agent Model. Princeton, USA: Princeton University Press, 2009.

|

| [33] |

Boonen T J, Jiang W. Mean-variance insurance design with counterparty risk and incentive compatibility. ASTIN Bulletin, 2022, 52 (2): 645–667. doi: 10.1017/asb.2021.36

|

ISSN 0253-2778

CN 34-1054/N

Copyright © Editorial Office of JUSTC, All Rights Reserved. 皖ICP备05002528号

Supported by:

Beijing Renhe Information Technology Co. Ltd

DownLoad:

DownLoad: