ISSN 0253-2778

CN 34-1054/N

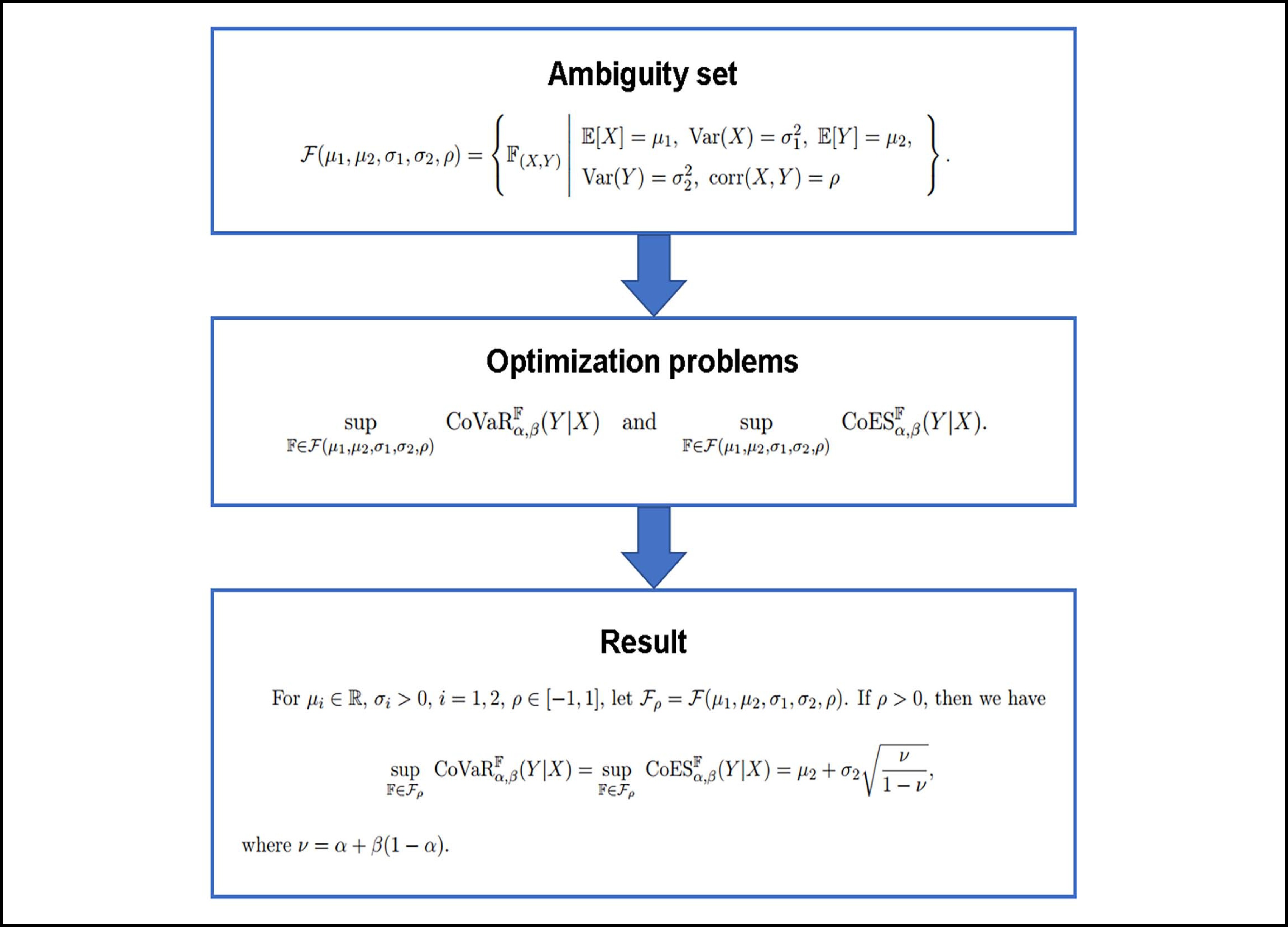

In this paper, we study the worst-case conditional value-at-risk (CoVaR) and conditional expected shortfall (CoES) in a situation where only partial information on the underlying probability distribution is available. In the case of the first two marginal moments are known, the closed-form solution and the value of the worst-case CoVaR and CoES are derived. The worst-case CoVaR and CoES under mean and covariance information are also investigated.

We construct the above new ambiguity set, then propose the optimization problem of CoVaRand CoES based on this ambiguity set, and give the theoretical results.

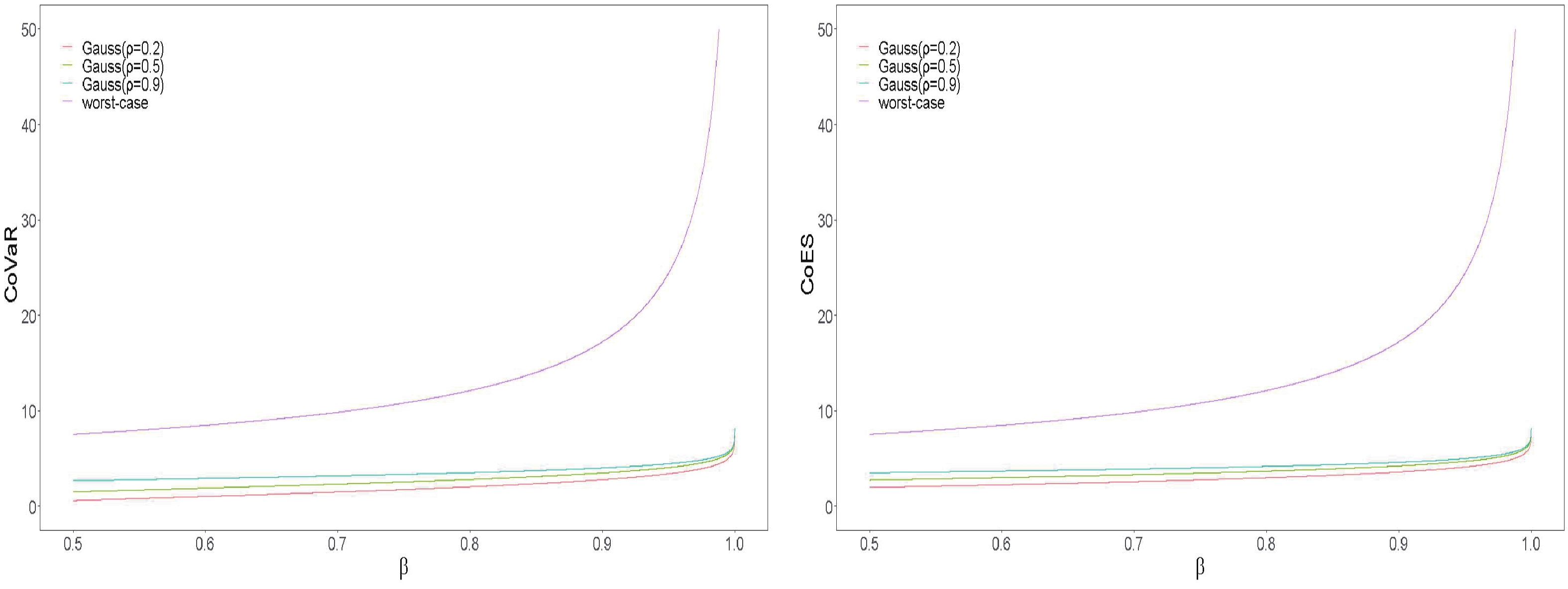

Figure 1. CoVaR and CoES with bivariate Gaussian distributions.

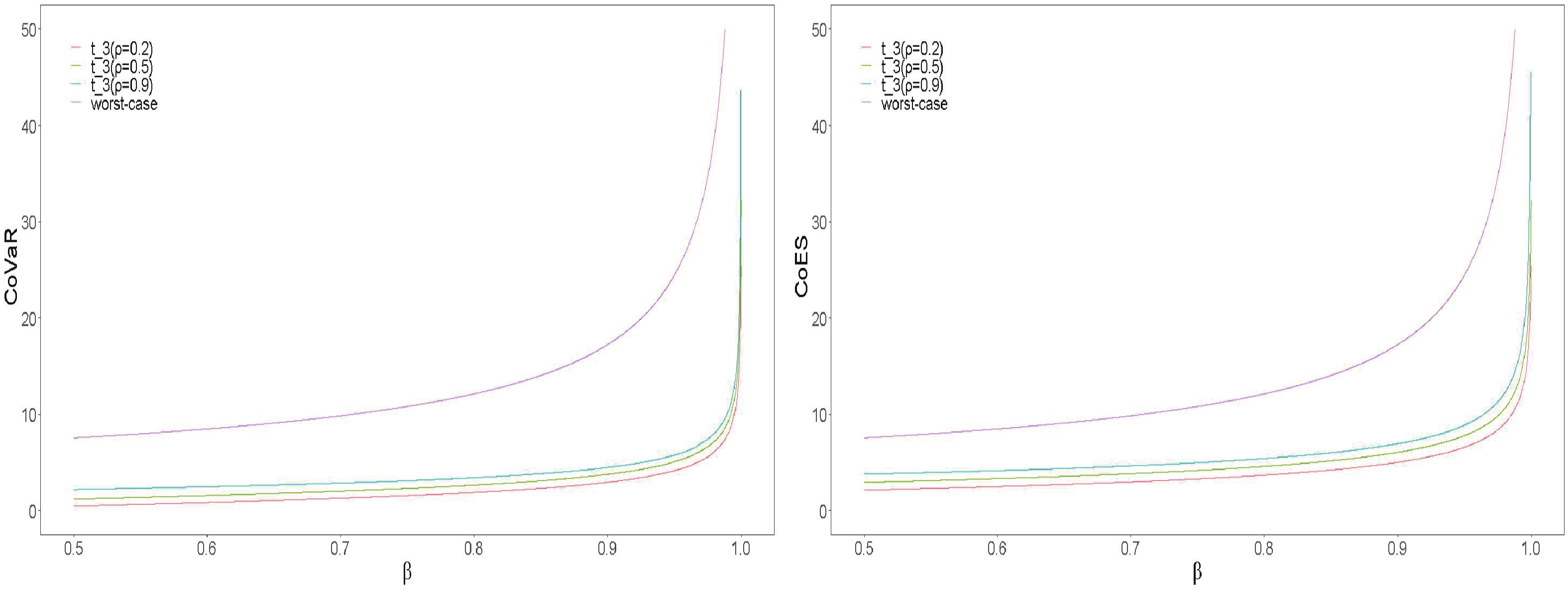

Figure 2. CoVaR and CoES with bivariate t-distributions.

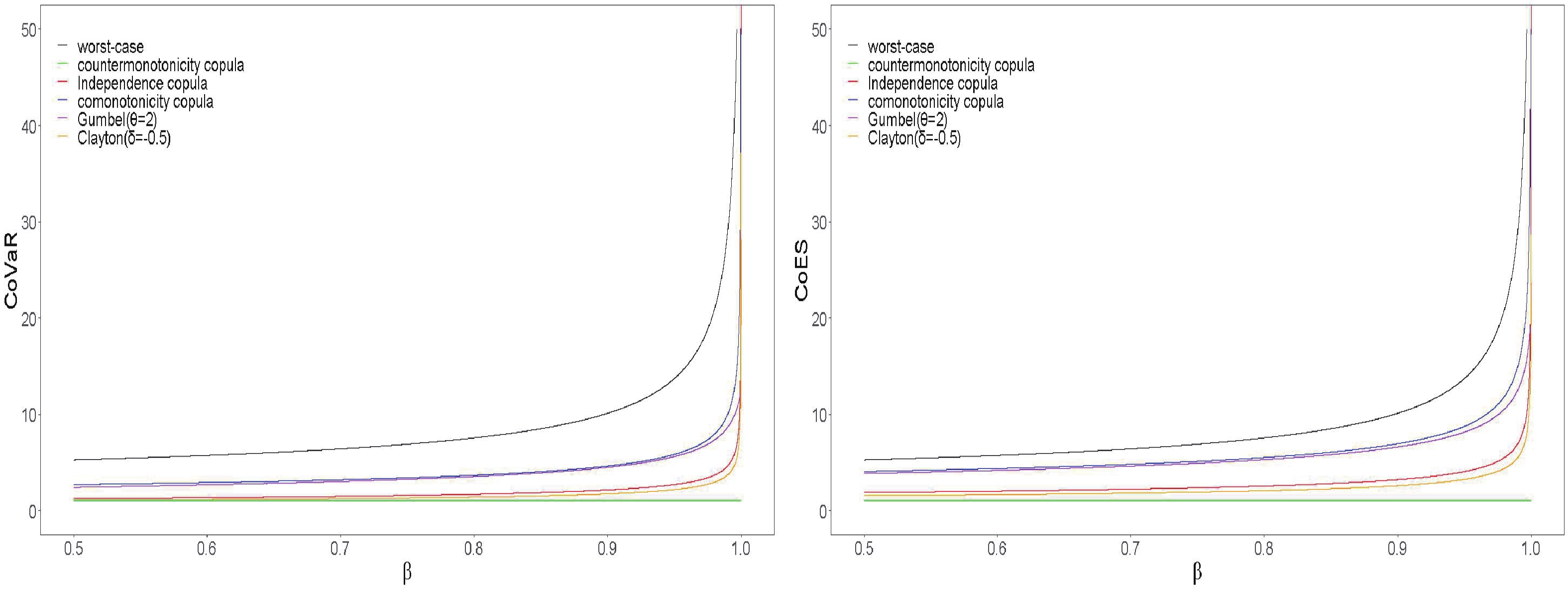

Figure 3. CoVaR and CoES with Pareto marginal and different copulas.

| [1] |

Basel Committee on Banking Supervision. Minimum capital requirements for market risk. Basel, Switzerland: Bank for International Settlements, 2019.

|

| [2] |

Adrian T, Brunnermeier M K. CoVaR. American Economic Review, 2016, 106 (7): 1705–1741. DOI: 10.1257/aer.20120555

|

| [3] |

Brownlees C, Engle R F. SRISK: A conditional capital shortfall measure of systemic risk. The Review of Financial Studies, 2017, 30 (1): 48–79. DOI: 10.1093/rfs/hhw060

|

| [4] |

Acharya V V, Pedersen L H, Philippon T, et al. Measuring systemic risk. The Review of Financial Studies, 2017, 30 (1): 2–47. DOI: 10.1093/rfs/hhw088

|

| [5] |

Girardi G, Ergün A T. Systemic risk measurement: Multivariate GARCH estimation of CoVaR. Journal of Banking & Finance, 2013, 37 (8): 3169–3180. DOI: 10.1016/j.jbankfin.2013.02.027

|

| [6] |

Huang W Q, Uryasev S. The CoCVaR approach: Systemic risk contribution measurement. Journal of Risk, 2018, 20 (4): 75–93. DOI: 10.21314/JOR.2018.383

|

| [7] |

López-Espinosa G, Moreno A, Rubia A, et al. Short-term wholesale funding and systemic risk: A global CoVaR approach. Journal of Banking & Finance, 2012, 36 (12): 3150–3162. DOI: 10.1016/j.jbankfin.2012.04.020

|

| [8] |

Karimalis E N, Nomikos N K. Measuring systemic risk in the European banking sector: A Copula CoVaR approach. The European Journal of Finance, 2018, 24 (11): 944–975. DOI: 10.1080/1351847X.2017.1366350

|

| [9] |

Popescu I. Robust mean-covariance solutions for stochastic optimization. Operations Research, 2007, 51 (1): 98–112. DOI: 10.1287/opre.1060.0353

|

| [10] |

Bertsimas D, Doan X V, Natarajan K, et al. Models for minimax stochastic linear optimization problems with risk aversion. Mathematics of Operations Research, 2010, 35 (3): 580–602. DOI: 10.1287/moor.1100.0445

|

| [11] |

Delage E, Ye Y. Distributionally robust optimization under moment uncertainty with application to data-driven problems. Operations Research, 2010, 58 (3): 595–612. DOI: 10.1287/opre.1090.0741

|

| [12] |

Natarajan K, Sim M, Uichanco J. Tractable robust expected utility and risk models for portfolio optimization. Mathematical Finance, 2010, 20 (4): 695–731. DOI: 10.1111/j.1467-9965.2010.00417.x

|

| [13] |

Wiesemann W, Kuhn D, Sim M. Distributionally robust convex optimization. Operations Research, 2014, 62 (6): 1358–1376. DOI: 10.1287/opre.2014.1314

|

| [14] |

Chen L, He S, Zhang S. Tight bounds for some risk measures, with applications to robust portfolio selection. Operations Research, 2011, 59 (4): 847–865. DOI: 10.1287/opre.1110.0950

|

| [15] |

Nelsen R B. An Introduction to Copulas. 2nd edition. New York: Springer, 2006.

|

| [16] |

Mainik G, Schaanning E. On dependence consistency of CoVaR and some other systemic risk measures. Statistics & Risk Modeling, 2014, 31 (1): 49–77. DOI: 10.1515/strm-2013-1164

|

| [17] |

Ghaoui L E, Oks M, Oustry F. Worst-case value-at-risk and robust portfolio optimization: A conic programming approach. Operations Research, 2003, 51 (4): 543–556. DOI: 10.1287/opre.51.4.543.16101

|

| [18] |

Bernard C, Pesenti S M, Vanduffel S. Robust distortion risk measures. https://ssrn.com/abstract=3677078 .

|

ISSN 0253-2778

CN 34-1054/N

Copyright © Editorial Office of JUSTC, All Rights Reserved. 皖ICP备05002528号

Supported by: Beijing Renhe Information Technology Co., Ltd.

DownLoad:

DownLoad: